TikTok Shop Watch #1: Southeast Asia

How well can Bytedance replicate its e-commerce success in Southeast Asia?

Image source: TikTok

Content

Introduction

About a year ago, and a few months after TikTok Shop officially launched in the US, we published an extensive report on TikTok Shop: The long and winding road of TikTok Shop. We explored how TikTok Shop had fared in Indonesia and the UK. TikTok Shop largely failed in the latter market because of its excessive focus on live commerce and poor management of cultural differences. TikTok refocused on Southeast Asia but also faced various challenges in that part of the world.

Now that TikTok Shop is launching in Europe, has been active in the US for about 16 months and all eyes are on whether the app will be banned or sold in that market, we thought it was time for an update. Has it shown more success in the US than in the UK? And how is it doing in Southeast Asia?

There is much information to share on TikTok Shop’s developments in 2024 and its prospects now that it recently launched in several European countries. Therefore, we have decided to split this report into multiple parts. In this first part, we will examine the developments and status of TikTok Shop in Southeast Asia. In the second part, we will discuss the US and European markets. In the third and final part, we explore the various sales models TikTok uses around the world and look at the level of success of live commerce in its markets. We will publish these reports over the next three weeks.

While your business interests might not be focused on the Southeast Asian market, this first part should still interest you since TikTok uses the region as a test area. In this region, Bytedance will try out strategies implemented in Douyin years ago. As such, it will show where TikTok Shop might go in other parts of the world.

The first chapter with statistics for Southeast Asia is free to read for all subscribers, the rest of the report is available to paid subscribers only.

Please note that some of the data in this report can be conflicting since they come from different sources that can use different definitions for metrics.

We hope you enjoy this report.

Cheers,

Ed Sander – Research Editor

TikTok Shop in Southeast Asia

By 2024, TikTok's e-commerce business had been launched in 9 markets worldwide, including six Southeast Asian countries (Indonesia, Vietnam, Thailand, Malaysia, The Philippines and Singapore), the United States, the United Kingdom and Saudi Arabia. Among these markets for TikTok e-commerce, the Southeast Asian countries performed exceptionally well, with their total merchandise volume exceeding that of other regions. The best countries in Southeast Asia have an average daily sales of about $40 million. Meanwhile, in other countries, TikTok has performed poorly or failed to enter successfully for various reasons (we will get back to that in part 2 of this series).

TikTok also withdrew from Brazil and Mexico (where it recently relaunched). While it wanted to focus resources on existing markets, it faced risks with tariff policies (Brazil), political instability (Mexico), and government investigations (Europe). Therefore, TikTok decided not to enter these high-risk emerging markets but to focus resources on relatively stable regions with high growth potential, such as Southeast Asia, the United Kingdom, and parts of the United States.

Understandably, Bytedance chose Southeast Asia as its first region for expanding TikTok Shop. The number of consumers is enormous, the e-commerce market is growing fast and comparable to China 10-15 years ago, and the geographical distance is relatively small. Moreover, TikTok's main user groups are concentrated in Southeast Asia, with Indonesian users accounting for nearly 70% of the region's users.

The total e-commerce market in Southeast Asia is worth $114.6 billion, with Indonesia making up 46.9% of that. Vietnam and Thailand are the fastest-growing markets, with growth rates of 52.9% and 34.1%, respectively, while Indonesia is more mature, with a growth rate of 3.7. [1] According to research firm Cube Asia, the net merchandise value will double to over $300 billion in 2029. Influencer-led marketing is contributing about one-fifth of online sales in the region. [2]

Gross Merchandise Value

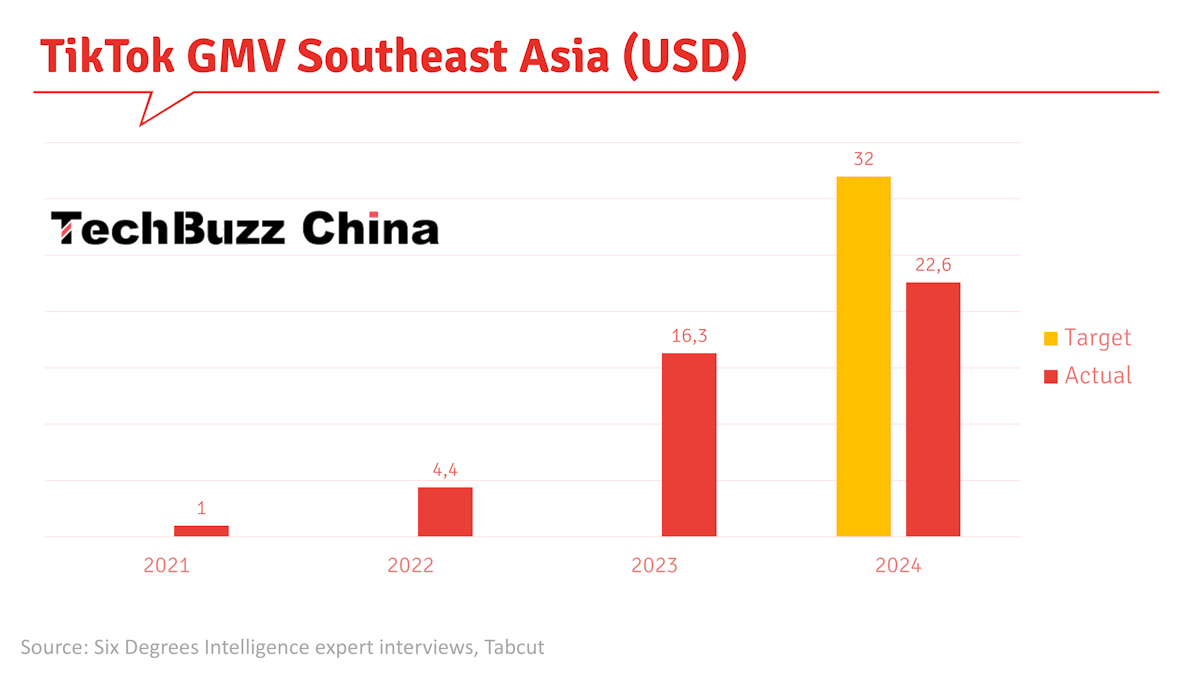

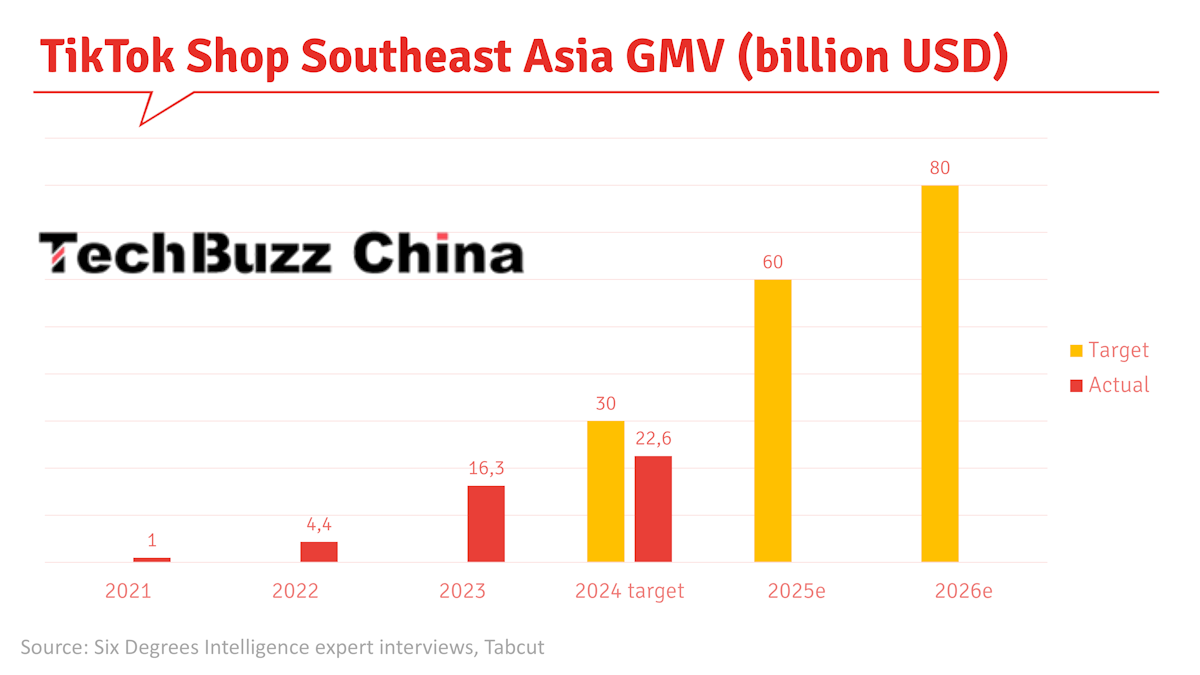

TikTok launched in Southeast Asia in February 2021, with Indonesia being its first market. Our December 2023 report described its early success in the region. In 2022, TikTok Shop was launched in Thailand, Vietnam, Malaysia, Singapore, and the Philippines, and the Southeast Asia GMV reached $4.4, which was 90% of global GMV. [3]

In 2023. TikTok's global e-commerce GMV TikTok Shop almost quadrupled its GMV to $16.3 billion. [5] Southeast Asia again contributed more than 90%. That same year, TikTok launched TikTok Mall (search-based ‘shelf e-commerce’), which reached 37% of GMV, a higher share than Douyin Mall has in China. [3]

The Southeast Asian e-commerce market performed strongly in the first half of 2024, especially in household goods, cosmetics and women's clothing categories. Specifically, sales of household goods reached $2.3 billion, cosmetics sales were $1.7 billion, and electronic products sales were $830 million. Overall, the total merchandise transaction volume of Southeast Asian e-commerce in the first half of 2024 was approximately $12.7 billion.

By mid-2024, daily orders reached the number in the table below.

Source: Former ByteDance TikTok e-commerce strategy manager, June 2024

In the first nine months of 2024, TikTok Shop’s revenue grew by 111% YoY. [7]

According to Tabcut, the 2024 GMV in SEA ended up being $22,6 billion. [9]

These are all impressive figures, but they didn’t meet TikTok’s own expectations. Initially, TikTok’s Southeast Asian e-commerce market was expected to expand to $32 billion by 2024. The main reasons for the possible failure to achieve the annual target include poor sales performance after the end of Ramadan and poor results of spring marketing activities. Also, Indonesia’s GMV needed to recover from a 2-month ban on TikTok Shop in Indonesia in Q4 2023 (see ‘Indonesia’).

Source: Tabcut [9]

Other KPIs

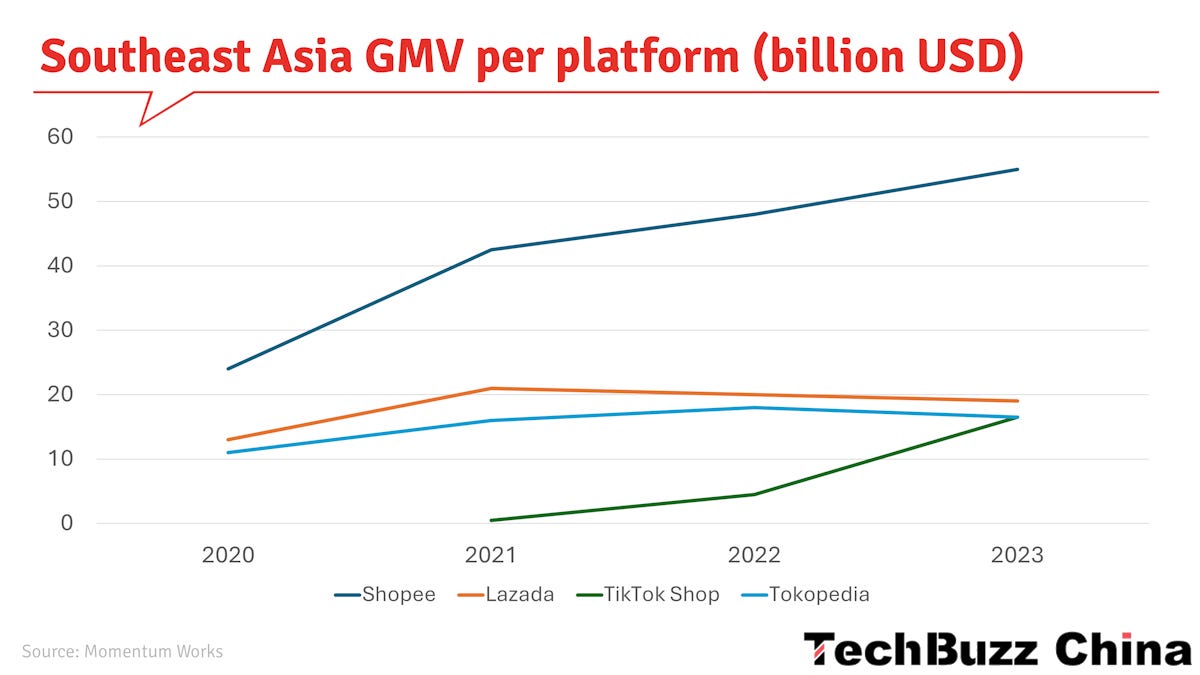

Currently, Southeast Asia has become TikTok Shop's main source of income. In the Southeast Asian e-commerce market, TikTok has advanced from a market share of about 13.2% in 2023, a significant increase from 4.4% in 2022. [6] Together with Tokopedia, TikTok now has a 30% market share in SEA, second only to Shopee (48%). [3]

Note: 2024 includes Tokopedia.

On a country level, Shopee has a market share of 35-45% in various markets, while TikTok's market share is only 5-15%. To increase its market share and catch up with its competitors, TikTok plans to increase its market share to about 25% by enhancing user interaction and optimising its operations.

TikTok's strategy in the Southeast Asian e-commerce market has several notable features. First, with more than 90%, local merchants occupy most of the platform's GMV. Due to the impact of tax policies, cross-border e-commerce lacks competitiveness - especially in Indonesia - TikTok mainly relies on local businesses. However, in the other five Southeast Asian countries, both cross-border and local merchants can be found on the platform.

TikTok's strategy focuses on attracting large sellers to cover 90% of competitor merchants. The platform considered multiple factors in its development, including content sustainability, merchants' production capabilities, and influencers' cultivation.

In terms of orders, the average order amount in the region is between $4.5 and $6. Singapore has the highest average order value, more than $20, while the average order value in other markets is about $4 to $5.

TikTok's current e-commerce user conversion rate is 20%, which is still far from the 40-50% in the Chinese market.

Regarding consumer behavior, it found that consumers in Southeast Asia generally have low brand loyalty and awareness. However, the Singapore market is again an exception: Singaporean consumers show high brand loyalty and willingness to buy.

The return rate in Southeast Asia is higher than that in China, mainly because cash on delivery is widely used in the region. In China, the return rate is about 20%, while in Southeast Asia, this rate is usually higher. This model has led to an increase in the proportion of unpaid orders, which has brought challenges to TikTok's business development in the region. Despite this, TikTok's performance in Southeast Asia is still quite good, especially in the two important markets of Indonesia and Thailand.

In 2024, TikTok has shifted its strategic focus from growth to improving financial outcomes. The platform is now prioritizing the development of a more profitable business model to recover its investment. The primary objective has become enhancing profitability.

Please note: the rest of this article, containing information on competition, the Indonesian market, logistics, products, local services, merchant costs and margins, challenges and outlook, is only available to paid subscribers.

Competitors

In previous years, the Southeast Asian e-commerce market was dominated by Lazada and Shopee. However, the situation has changed significantly. TikTok Shop has risen rapidly. Compared with the US market, competitors in the Southeast Asian market, such as Shopee and Lazada, are relatively weak, which allowed TikTok to enter and increase its market share quickly.

There are significant differences between Southeast Asian e-commerce platforms. TikTok Shop tends to sell creative and interactive goods, emphasising the characteristics and practicality of products. In contrast, Shopee and Lazada offer a wider range of goods, including large household items and hardware. Regarding marketing strategy, TikTok Shop focuses on displaying practical goods and promoting sales through content marketing. In terms of logistics services, TikTok plans to launch preferential warehousing and logistics services to attract merchants to use its official services.

TikTok Shop versus Shopee

The two platforms have launched fierce competition in the Southeast market, especially in Indonesia and Vietnam. Both platforms are rapidly growing in the region, primarily by capturing market share from other competitors rather than from each other. While TikTok Shop has grown, its scale and market influence still lag behind Shopee's. Shopee is outperforming TikTok Shop in several areas, boasting a higher average spend per customer and a more extensive user base. Interestingly, while TikTok Shop's growth has hit a standstill in some markets, Shopee's performance shows considerable regional differences.

Shopee uses specific tools to identify best-selling items on TikTok Shop and competes on price by subsidising similar products or introducing new sellers. However, Shopee has a more established presence in the market and continues to hold its ground in sectors like consumer electronics, where TikTok Shop's impact is minimal. TikTok Shop primarily focuses on the beauty and fashion sectors. Indeed, the relationship between Shopee and TikTok Shop isn't necessarily one of direct competition. Shopee's platform offers various products and services across multiple categories. Currently, the market environment supports both TikTok Shop and Shopee effectively. However, the market might not have the capacity to accommodate many more competitors beyond these two platforms.

Meanwhile, TikTok Shop still shows significant potential for growth. Q2 2024 quarterly data indicated that, in multiple markets, both average customer expenditures and the customer base for TikTok Shop are lower than Shopee's, suggesting room for expansion.

In 2024, Southeast Asian e-commerce platforms have experienced a notable increase in commission rates. Shopee led this trend, with other platforms following suit. Interestingly, following Shopee's fee changes in 2024, TikTok Shop mirrored these adjustments within a month. TikTok Shop observed that Shopee has not reverted to its former strategy of offering high subsidies. Consequently, it doesn't feel compelled to pursue an aggressive market either.

While TikTok Shop's fees remain lower, the gap between their rates and Shopee's has narrowed. Interestingly, the difference in commission rates between Shopee and TikTok Shop isn't substantial enough to trigger a mass exodus of sellers from one platform to another. The user base of major e-commerce platforms has largely adapted to this general fee rise.

This shift has played a significant role in Shopee achieving profitability. Similarly, Lazada has reportedly reached financial stability, while Tokopedia is either already profitable or on the brink of becoming so. The financial performance of TikTok Shop, however, remains unclear. The absence of significant delayed reactions to the fee increases suggests a transition period where Southeast Asian e-commerce platforms can potentially achieve profitability and attract investors.

In early 2024, Shopee's logistics advantage in the Vietnamese market was mainly reflected in its freight costs. Specifically, Shopee's freight costs were about half of TikTok Shop's. This significant cost advantage stems primarily from the fact that Shopee has its own logistics network, Shopee Express, while TikTok relies on third-party logistics services.

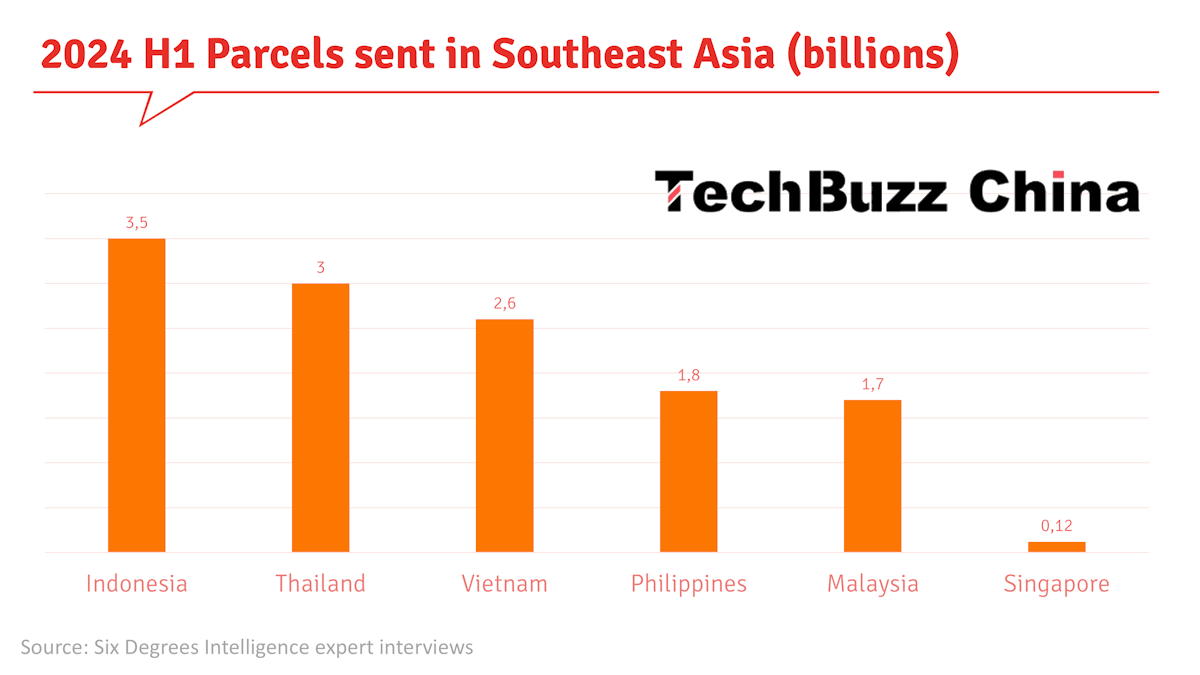

Shopee's logistics network is crucial to its e-commerce strategy, ensuring efficient delivery systems that contribute significantly to its competitive advantage. Shopee Express has almost 25% market share in parcel delivery in Southeast Asia, accounting for 1,8 billion parcels in the first half of 2024. [26] It delivers 50% of all Shopee orders in the region (as well as more than 70% in Brazil). This gives them better negotiation power with third parties and helps consistency in service levels. Of the other platforms, only Lazada has its own in-house logistics. [23] This strong delivery infrastructure is key to Shopee's ability to maintain its edge over rivals like Lazada and TikTok Shop in the e-commerce landscape.

The competitive landscape of Shopee and TikTok Shop in the Southeast Asian market is mainly reflected in how they obtain traffic. TikTok provides free traffic as an entertainment platform, and users conduct e-commerce activities only after browsing the content. TikTok limits e-commerce traffic to about 16% to prevent the platform from being over-commercialised. In contrast, Shopee, a market platform focusing on product variety and price, obtains traffic through multiple channels.

By October 2024, TikTok Shop's merchandise transaction volume in Vietnam had reached about 70% of Shopee’s. TikTok Shop has performed well in social e-commerce, and many Vietnamese users have moved from Facebook or Instagram to TikTok Shop for sales. Although TikTok Shop has been operating in Indonesia for quite some time, its market penetration is not as high as in Vietnam.

Both platforms have invested heavily in live broadcast functions and brand awareness to enhance their competitiveness. Well-known Internet celebrities are often invited to promote products and increase brand awareness through live broadcasts. In addition, the two companies hold concerts and other promotional activities to further enhance brand influence.

There are significant differences in sales patterns between the two e-commerce platforms. The sales trends of goods on the Shopee platform generally show a stable and predictable pattern. Once a product starts to sell well, it tends to remain popular for a long time. In contrast, the sales pattern of TikTok Shop shows an evident peak phenomenon, with a surge in product sales in a short period of time, followed by a rapid decline in demand.

On the one hand, this difference has an important impact on merchants' product strategies and inventory management. It makes it difficult for merchants to stock up stably locally. They often run out of stock as soon as orders are sold out. After the stock is out, new goods can only be transported by sea from China, which takes a month. To solve the shortage problem, TikTok Shop has worked hard in the past years to find local retail companies in Southeast Asia, and even rented stalls in wholesale markets and asked the owner to livestream the sales to find a more stable local supply. [24] The TikTok team was responsible for uploading products, ordering and shipping - all of which would reduce efficiency. [25]

On the other hand, TikTok Shop allows merchants to quickly understand the market response to new products and get feedback almost immediately after the products are put on the shelves. This leads to a higher frequency of new product launches on TikTok Shop. On the Shopee platform, since it takes longer to accumulate sales momentum, merchants may need to adopt different strategies to manage product life cycles and inventory.

Image source: TikTok

Zooming in on Indonesia

According to Statista, by July 2024, Indonesia had the most TikTok users worldwide, with almost 157 million users and 100 Daily Active Users. Forty percent of the population uses TikTok, and 65 percent of users are between 18 and 34 years old.

Indonesia’s e-commerce industry is set to expand to about $160 billion by 2030 from $62 billion in 2023, according to a report by Google, Singapore state investor Temasek Holdings and consultancy Bain & Co. [10] But Indonesia also has challenges in competition (Shopee and Lazada have 60% market share), poor logistics and payment infrastructure and a weak manufacturing industry resulting in out-of-stocks. [3]

The situation in Indonesia is different from those in other Southeast Asia countries. Creators and users are highly receptive to live streaming. Meanwhile, abundant business flow from Lazada and Shopee has driven the growth of logistics companies such as J&T Express (Jitu). However, due to the Indonesian government's local trade protection, only local merchants can open stores on TikTok. TikTok had to give up cross-border e-commerce and attract local merchants with zero commission. [25]

TikTok Shop has experienced relatively limited growth in Indonesia compared to other parts of Southeast Asia. This can be attributed to two main factors. First, Indonesia's e-commerce industry is more developed and thus experiencing a slower overall expansion pace. Second, TikTok Shop was introduced in Indonesia 6-9 months before it expanded to other Southeast Asian countries, affecting comparative growth rates.

TikTok Shop + Tokopedia

Since its launch in 2022, TikTok Shop has made significant strides in the Indonesian market. The platform's key growth strategy was expanding its merchant base. To achieve this, TikTok Shop actively reached out to top merchants from Tokopedia, encouraging them to fully transition their operations and increase their investment in TikTok Shop. It ensured it offered more competitive pricing and improved product placement. To achieve this, TikTok Shop offered financial incentives on its platform, aiming to surpass Tokopedia in terms of vendor attraction and retention.

TikTok Shop's strategy to outperform Tokopedia centred on offering merchants a more attractive fee structure, only asking them to pay an admin fee. In contrast, Tokopedia merchants faced additional charges on top of the standard admin fee when utilising services like Shopee Pay Later or Shopee Coins.

In Q4 2023, Indonesia implemented regulations stating that e-commerce and content platforms must be separated (TikTok was the only app in Indonesia doing this). These policy adjustments significantly impacted TikTok's gross merchandise volume (GMV) as it temporarily had to shut down its in-app e-commerce. In two months, TikTok lost $1 billion in GMV. [11]

In essence, the legislation was meant to protect local businesses. A local seller shared: “Although TikTok in Indonesia only allows local small stores to register, many local merchants’ sources of goods are actually made in China. Chinese products are abundant on the platform and are sold at low prices. Although they sell as Indonesian small and medium-sized enterprises, they may still threaten Indonesia’s manufacturing industry.” [12]

TikTok took action in response to these regulatory requirements. To obtain e-commerce qualifications, it acquired a 75% stake in Tokopedia for $840 million. The merger created a new entity with 40% market share in Indonesia, the second biggest after Shopee. [13]

During the negotiations, TikTok had demanded that the deal be closed before December 12th so that it could restart e-commerce before that day, an important shopping festival in Indonesia. When TikTok Shop relaunched on December 11th, it showed Tokopedia’s logo and green branding. [14] As part of the deal, the seller, Tokopedia’s parent company GoTo, got 0.4% fee on both TikTok and Tokopedia’s combined transaction amounts as a revenue stream with no associated cost. [10]

TikTok promised to, over time, invest over $1.5 billion in the merged entity and specific measures to support Indonesian small and medium-sized enterprises: [12]

The promotion of Indonesian products on Tokopedia and TikTok’s platforms

Building the capacity of Indonesia's SMEs through a program focusing on skills development and providing resources relating to upstream production and selling

Supporting merchants to sell products online by providing support in areas such as marketing, branding, and sustainable business practices

Helping local brands to promote their products in international markets

The establishment of technology centers across Indonesia to develop local tech talent

Ensuring a marketplace that fosters fair competition.

This also means that Chinese businesses might have to move manufacturing to Indonesia.

The joint venture allowed purchases to be completed on Tokopedia even as the advertising or promotion of products continued on TikTok, especially its live channel. TikTok would also set up an ‘Indonesia pavilion’ on Douyin to help Chinese merchants sell in China. [10]

The merger did not hurt user stickiness and repeat purchases but instead achieved traffic sharing between platforms. TikTok and Tokopedia can now direct traffic to each other, which helps maintain user stickiness. In addition, they have integrated the merchant management system to achieve the simultaneous upload of goods, improving efficiency and driving business growth.

After its revival, TikTok Shop in Indonesia generated sales of approximately RMB 2.88 billion in January 2024, an increase of approximately 72.4% year over year. [15] However, it took nine months, spanning Q4 2023, Q1 2024, and Q2 2024, for the Indonesian TikTok Shop to return to its pre-restriction revenue levels.

When it acquired Tokopedia, TikTok became the leading force in Indonesia's e-commerce sector. As a result of this merger, the e-commerce scene in Southeast Asia is undergoing notable changes. The cooperation with Tokopedia is a successful example of the company collaborating with other e-commerce platforms to achieve traffic sharing and maximise revenue. This cooperation model is similar to the relationship between Douyin and Taobao. Taobao puts external link advertisements on Douyin, but this does not affect Douyin's overall commercial scale.

The TikTok Shop + Tokopedia collaboration has prompted Shopee to adjust its strategy to maintain its leading position in the Indonesian market. TikTok Shop aims to expand its e-commerce strategy beyond its current focus on livestreams and short videos (‘content-based commerce’) to capture more intentional consumer purchases. The platform intends to broaden its product range to include more conventional e-commerce offerings (search-based ‘shelf commerce’), moving beyond spontaneous purchases. In Indonesia, collaborating with Tokopedia could drive significant growth for TikTok Shop.

However, integrating TikTok Shop with Tokopedia has also encountered significant challenges in its early stages. 2024 data show a decline in user activity on TikTok Shop following its merger with Tokopedia. This trend has sparked discussions about whether Shopee's aggressive market strategies are the primary cause or if customers simply prefer the products and user interfaces offered by Shopee and Lazada. Users appear to have a greater preference and recognition for the features and design of platforms like Shopee and Lazada.

Despite the partnership, Tokopedia has also struggled to reclaim a substantial portion of its market share, raising questions about the effectiveness of this alliance in competing with Shopee. Market analysis suggests that Tokopedia has yet to mount a significant challenge against Shopee. Tokopedia has adopted a cautious approach to offering discounts and running promotional campaigns, and as a result, its gross merchandise value is trending downward.

Meanwhile, TikTok Shop's Indonesian branch is growing, surpassing its performance in the same period in 2023 before the ban was implemented. At present, the combination of TikTok Shop and Tokopedia has not yielded significant outcomes. However, it's crucial to continue monitoring this consolidated entity, as it may leverage its assets within the Indonesian market in the future.

While the integration of TikTok Shop and Tokopedia faced initial hurdles, its impact on the e-commerce landscape in Indonesia remains to be seen. There's significant interest in whether Tokopedia will improve its market performance. Any signs of potential collaboration or partnership between Tokopedia and TikTok Shop are closely watched in the market.

After the merger, the combined entity had about 5,000 employees. [16] On June 14th 2024, a round of layoffs was announced. TikTok's systems would replace nearly 80% of Tokopedia’s. Redundancy estimates ranged from 450 to 70% of Tokopedia’s almost 3000 employees. Layoffs would occur throughout the second half of 2024 and first impact Governance, Trust & Safety, Creator Operations and Account Management. [17]

Merchant Costs and Margins

In the early days, TikTok Shop would invite merchants on Lazada and Shopee to join its platform, which led to Shopee implementing ‘cut-off contracts’ with merchants, giving merchants a small RMB 377 subsidy if they didn’t sell on TikTok. But TikTok offered $100 in subsidies for livestream investments for every $100 sold and also paid the postage fees. Competitors could not match these benefits. [3]

TikTok Shop was also later (at the end of 2022) in implementing store deposits than Shopee and Lazada (at the beginning of 2022), and its deposits were less than 1/3rd of the other two. While Shopee raised commissions and handling fees to 10% in 2022, TikTok’s was still 3%, and merchants still had a three-month commission-free period and free shipping for 30 days. TikTok Shop also subsidised service providers with up to 10% cash rebates if transaction volume met specific requirements. [3] [24]

However, TikTok Shop has significantly changed its approach to merchant incentives and fees over the past year. Notably, they've reduced the financial perks offered to merchants. Despite this reduction, TikTok Shop's merchant incentives remain comparable to Shopee's. Still, TikTok Shop has surprised many by accelerating its commission hikes, increasing its revenue share. Overall, TikTok Shop has quickly adopted traditional market strategies, demonstrating a rapid evolution in its approach to e-commerce.

TikTok Shop achieved a single-month overall profit in early 2024 and planned to have full-year profitability in Southeast Asia by the end of 2024. [3]

On the TikTok platform, the profit margins of merchants of various types and sizes differ. For merchants who distribute goods, TikTok's commission rate in Southeast Asia is only 5%, much lower than Shopee's more than 20% commission rate in some categories, so it has more profit potential. On Shopee and Lazada, merchants' total expenses (including commissions, logistics and advertising fees) usually exceed 30%. However, content-based merchants on TikTok Shop have higher overall costs due to the need to invest in live broadcasts and influencers. It may be difficult to achieve profitability if they mainly rely on content promotion.

The cost of livestreaming marketing involves many aspects, including hiring anchors, paying platform fees, and paying commissions. In Southeast Asia, the monthly cost of hiring 3 to 5 influencers is about $6,000 to $8,000, and the labour cost is relatively low. Together with the investment in livestreaming equipment, the total monthly expenditure is about $50,000 to $60,000. Large livestreaming rooms can achieve monthly sales of millions of dollars, while their fixed costs account for a relatively low proportion. In daily livestreaming activities, large merchants usually hire medium-sized influencers with stable influence. Although these influencers are not top-tier celebrities, they can provide continuous and stable promotion effects.

Most merchants can achieve profitability on the TikTok platform, but this depends on their investment strategy and goals. Some brands may be more concerned with brand image building than direct profitability, so they may accept a lower return on investment. Most big brands that hire influencers for livestreaming do not focus on direct sales as their primary goal but on long-term brand value.

In the Indonesian market, TikTok observed that leading merchants usually cooperate with well-known Internet celebrities or KOLs for a short period during major events or new product launches. The platform mainly attracts some local white-label products and a small number of local brands. Finding a balance between content marketing, KOL cooperation, and brand building is the key.

Competition in the Southeast Asian e-commerce market is extremely fierce, especially in terms of price wars. In this context, TikTok has adopted a strategy of providing subsidies to lower prices in order to attract users. Taking Indonesia as an example, TikTok provides about 20% of commodity and transportation subsidies, making its commodity prices about 10% lower than Shopee (when comparing the same SKU). The cost of this subsidy program is borne not only by the platform but also by merchants.

Delivery fees can seriously impact a merchant's profitability. In an early 2024 interview, a Vietnamese shoe seller shared, "Most small and medium-sized sellers in the Vietnamese market are losing money. I think the shipping fee charged by TikTok is the last straw for merchants. Because of each product's small profit margin, shipping fees’ impact is even more magnified." If shipped to the same address in Hanoi, the shipping cost of Shopee orders is RMB 3-6 less than for TikTok Shop orders. This price difference is related to the cooperation models signed by each merchant with different platforms. Still, it is undeniable that TikTok Shop’s shipping commission has affected many small and medium-sized businesses in Vietnam.” [15]

Logistics

Logistics are a serious challenge in Indonesia, a nation of 270 million inhabitants and 17,000 islands. Tokopedia spent over a decade and millions of dollars on developing an infrastructure. The conglomerate behind Tokopedia, GoTo, has a logistics arm that operates five warehouses on Java, home to about half the country’s population. This business went to TikTok as part of its deal with Tokopedia. [19]

Still, TikTok selects logistics partners based on service quality and cost-effectiveness, and its logistics and distribution strategy in Southeast Asia mainly relies on J&T Express (Jitu). The number of orders for J&T Express in Southeast Asia has remained relatively stable. Compared with the high growth in the 2022-2023 period, the current growth rate has slowed down, and the penetration rate of logistics has not changed significantly.

In August, the company accounted for 80% of TikTok's logistics volume in Southeast Asia, especially in Indonesia. J&T Express was chosen for its comprehensive service capabilities, including price stability, delivery efficiency, and package integrity. J&T Express's logistics tracking transparency and network coverage meet TikTok's needs. In the Indonesian market, in addition to J&T Express, TikTok also uses Ninja Van (17 million pieces) and GoTo Logistics (1 million pieces) for logistics distribution. In the Thai market, in addition to J&T Express handling 141 million parcels, Flash Express is handling 58 million parcels, and Kerry Express is handling more than 5 million parcels.

Currently, J&T Express has a market share of more than 90% in Indonesia and about 80% in Thailand, showing its dominant position in these markets. Compared with the domestic Chinese market, J&T faces less competitive pressure in Southeast Asia, providing more development opportunities.

J&T has performed outstandingly in the Indonesian market, handling 140 million parcels in the second quarter of 2024 alone, becoming a major force in the market. However, with the increase in the number of orders, J&T may face the challenge of capacity pressure. Looking ahead, 2025 will be a critical period. As the number of orders increases, whether J&T Express can efficiently process large orders and maintain system stability will become an important issue.

To meet this challenge, it plans to improve the efficiency of parcel distribution by enhancing technology and optimising the network, as well as seeking external assistance to improve efficiency further. Although the market penetration rate may decline, the total number of parcels in the Southeast Asian e-commerce logistics market is expected to continue to grow.

Image source: still from a J&T Indonesia promo video

Will TikTok set up self-operated logistics?

Speculation is rife about potential significant investments in TikTok’s supply chain infrastructure. While TikTok Shop almost exclusively partners with J&T and Ninja Van for deliveries, there's talk of them possibly developing their proprietary delivery system. However, building such a system from scratch would require substantial financial resources. Interestingly, the investment remains considerable even in Indonesia, where TikTok Shop acquired Tokopedia, which had its own delivery service due to a previous merger with a local courier company.

Compared with using third-party logistics, the cost of self-operated logistics may be about 20% lower than using third-party logistics because the overall cost can be better controlled. However, While TikTok Shop is exploring creating its own logistics network, it's not currently a top priority because this requires high costs and complicated processes. TikTok would need to invest a lot of infrastructure in self-built logistics, which puts its initial preparation costs under great pressure.

They may consider the option after 2025 or 2026. From the perspective of long-term sustainable development, evaluating whether these infrastructure investments can be recovered through long-term operations is necessary. Using third-party logistics can avoid significant initial investments, but the cost per delivery may be slightly higher. This trade-off needs to be carefully considered to ensure that TikTok's subsidy strategy is sustainable in the long run.

Instead of setting up in-house logistics, TikTok focuses on establishing multiple storage centres to reduce delivery times and improve distribution efficiency, especially in smaller urban areas outside major cities. This strategy mirrors successful approaches taken by other e-commerce giants. However, the financial implications of such moves are significant. TikTok Shop carefully weighs its options as it plans its next steps in the competitive e-commerce landscape.

At the same time, the express delivery industry in Southeast Asia is also facing a fierce price war that keeps costs down for TikTok Shop. Major express delivery companies have attracted customers by lowering prices to increase market share. Among them, J&T Express has built a vast logistics network in Southeast Asia, and few other large logistics service providers can compete with it. J&T Express offers TikTok a price discount of about 15%, which gives it an advantage in the competition. Although FlashExpress has a certain scale, its operating network has not yet covered all markets.

Products

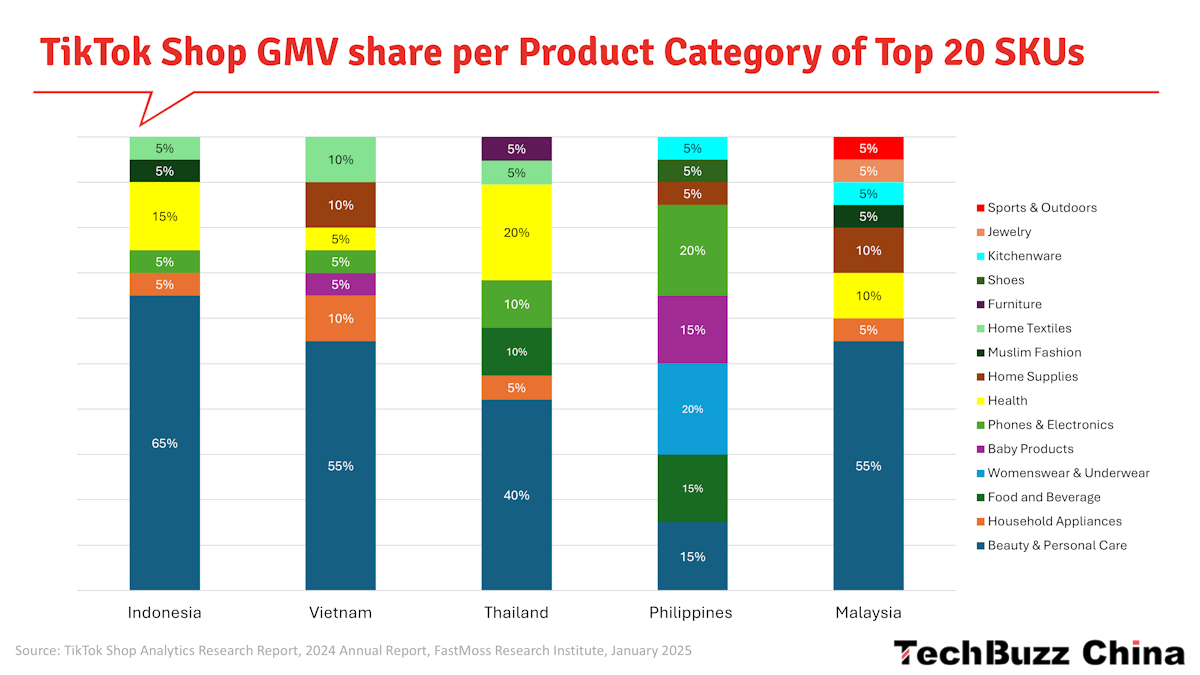

According to TikTok data analytics company FastMoss, Beauty & Personal Care was the most popular product category in every market. Women’s apparel was another popular category, and Muslim Fashion stood out in Malaysia and Indonesia.

Image: TikTok Shop Analytics Research Report, 2024 Annual Report, FastMoss Research Institute, January 2025

Tabcut data confirms that the Muslim Fashion category has become a major hit on TikTok Shop Indonesia, maintaining a consistent third-place ranking among all product categories for the past six months. Tabcut's data indicates that in September 2024, TikTok Shop Indonesia achieved a GMV of $552 million, with the Muslim fashion category contributing roughly $45.4 million, 8.22% of the total GMV. [8]

In Indonesia, 9 of the 10 top shops and 8 out of 10 top-grossing products are from the beauty and personal care category. The AOV in the country is $4.98. [9]

Fastmoss tracked the categories for the top 20 SKUs sold on TikTok Shop. The data shows apparent differences per market.

Local Services

TikTok Shop is already starting to offer more than just physical products…

Over the past two years, we have published two reports on how Douyin has entered the local services business in China (Food Fight! Douyin’s local services business and What’s up with…? - Part 4: Douyin Local Services). In 2023, Douyin made RMB 310 billion GMV in local services.

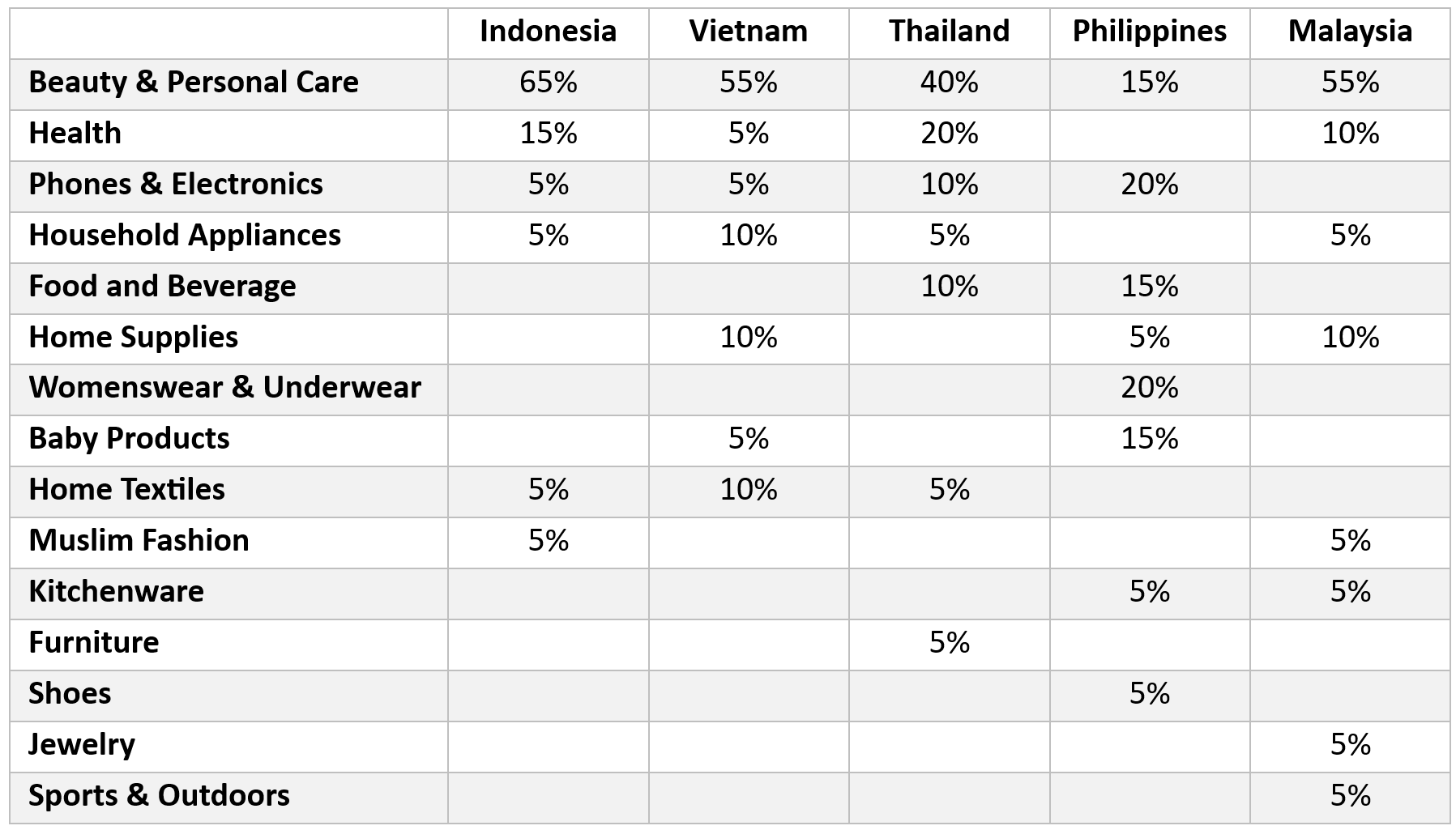

In July 2024, news broke that TikTok had started testing local services in Thailand and Indonesia. While still in beta phase, some users would see group buying deals in their feeds, primarily from restaurants. TikTok started posting content to recruit merchants for ‘TikTok Local Services’ and job postings for Singapore, Bangkok and Jakarta on its official website. [4]

Job description for "Business Development Manager" (Source: TikTok Career official website) [4]

This development shows that Bytedance follows the exact roadmap with TikTok as Douyin in China: short video + advertising -> in-app e-commerce -> local services. [4]

There is a large potential market for local services in Southeast Asia, which has a total population of nearly 700 million, of which more than 50% are under 30 years old. Furthermore, there is a high penetration rate of online payments, a unique food culture fostered by the tropical climate, a prosperous service industry created by cheap labor, and rich natural and cultural tourism resources. These are all potentials for the local life industry in Southeast Asia. [4]

However, as with e-commerce, a sound infrastructure is the main challenge for local services. The transportation and logistics systems in Southeast Asia are not yet fully developed, and the expansion of chain enterprises is restricted by the supply chain, which also leads to the immaturity of the local supply side. In 2023, the chain rate of the catering sector was only one-third of that in the United States. Many catering stores' hygiene and safety standards are also far behind those of mature countries, and there is a lack of standardised and innovative new products. [4]

The regulatory risks involved with using real location data necessary for the local services business could also be a hidden concern for TikTok in developing local life business overseas. A person close to TikTok revealed that the platform had planned to do local life overseas "very early, but the local supply chain is difficult to do, so we have been building infrastructure." [4]

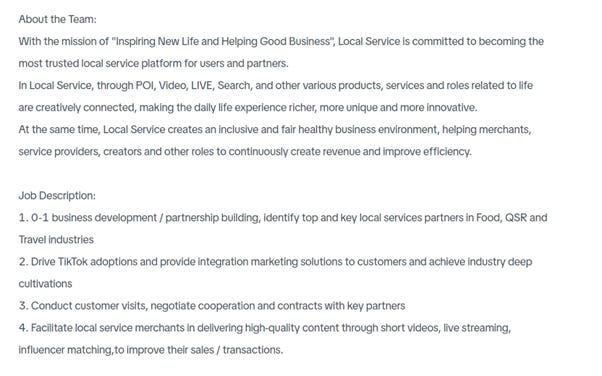

The first signs of local services can also be seen outside Asia. In August 2022, TikTok and Ticketmaster partnered to enable TikTok users to discover events and directly buy tickets through the app in the US. Selected content creators can add links to the event in their videos. [20] At the end of 2023, the functionality was expanded to 20 countries. Any ‘Certified Artist’ on TikTok in participating countries can use the Ticketmaster ticketing feature to promote their live dates and connect with fans around the globe. [21]

Image credit: TikTok

Challenges

TikTok Shop is facing various challenges in the Southeast Asian market.

The significant e-commerce expansion in Indonesia primarily occurred from 2018 to 2020. However, the growth drivers evident in the Indonesian market during this period are no longer present. Currently, the growth of Indonesia's e-commerce industry is experiencing a period of slow progress, similar to the aftermath of excessive consumption. This gradual advancement has led to a reduction in competitive intensity within the market. In today's environment, increasing market share requires taking it from competitors, which is expensive. Unlike previous years, the current scenario does not allow businesses to take advantage of organic market growth.

After the regulatory challenges in Indonesia, other Southeast Asian countries such as Thailand, Vietnam and Malaysia could also come with similar uncertainty risks. The governments of these countries have communicated with TikTok and raised some challenges and pressures, but these have not yet been translated into specific laws or policies.

After Indonesia’s ban, Malaysia said it was studying its own regulations closely, and Vietnam hit out at TikTok for content that Hanoi says spread distorted information, including inciting violence, while its shop also failed to provide requisite information about sellers’ goods, according to the government. [10]

In Malaysia, where TikTok Shop held nearly 20% of the e-commerce market in 2023, officials were also considering new rules for the platform. And the Indonesian government isn’t done regulating the e-commerce industry, Rifan Ardianto, a director at the Ministry of Trade, said in an interview last year. In October, Indonesian officials said they had asked Apple and Google to block Temu and Shein from app stores in the country. [14]

Many Southeast Asian countries are now mainly paying attention to the positions of the United States and other major economies. If the United States continues to put pressure on TikTok, Southeast Asian countries, the United Kingdom, and other European countries may follow in its footsteps, triggering more uncertainty risks. This chain reaction may have a broader impact on TikTok's global business.

There are growing concerns about the potential oversaturation of TikTok Shop's live-streaming e-commerce in Indonesia and the broader Southeast Asian market. While some are debating whether live streaming is suitable for these sectors or if there's a shortage of skilled influencers to drive engagement, it's important to note that the live streaming feature of TikTok Shop has not yet reached its peak or widespread adoption.

Another challenge is the partnership between Shopee and YouTube (332 million users in Southeast Asia), which launched YouTube Shopping in Indonesia, Thailand and Vietnam in September. Users can purchase products featured on YouTube through links to Shopee embedded in the videos. How successful this partnership will be remains to be seen because, for many influencers, it is harder to get engagement and, thus, sales on YouTube if they are new to the platform or have a small following. Brands also prefer TikTok because YouTube influencers with large followings tend to be more expensive. Finally, users also tend to use YouTube more for long-form content, news, entertainment, and motivational videos. [2]

Many Indonesians don’t have bank accounts, and e-commerce companies allow shoppers to pay for items in cash upon delivery. [19] This limitation results in high return rates and unpaid orders, so TikTok needs to adopt corresponding strategies to address it in this and other markets. These strategies may include optimising the logistics system, improving payment methods, and strengthening user education.

Compared with China, the Southeast Asian market is still in its infancy, and the competitive landscape has not yet been entirely determined. The region's main challenges include a complex financial environment and changing policies, which have brought significant difficulties to logistics management. Despite these uncertainties and challenges, the Southeast Asian e-commerce market still contains big opportunities. As the market continues to mature and infrastructure improves, TikTok expects to see more innovation and growth.

Outlook

Despite the abovementioned challenges, TikTok has a promising development prospect in the Southeast Asian market. First, TikTok has a large user base, with monthly active users reaching 1.2 billion worldwide. In every Southeast Asian country, TikTok has more than 50 million monthly active users; in Indonesia, the number exceeds 150 million (Statista, July 2024). This provides a vast potential market for TikTok.

In the next two years, e-commerce user penetration in Southeast Asia is expected to reach 20%. To promote this growth, e-commerce platforms can improve product supply by increasing content and attracting more large retailers and small sellers to promote user conversion. Once the e-commerce user penetration rate reaches 20%, the market may enter a stable stage and undergo a consolidation process. Against this backdrop, TikTok has set ambitious goals for its e-commerce business in Southeast Asia.

There's an ongoing discussion about TikTok Shop's strategic direction in Indonesia, particularly whether it will intensify competition with Shopee or prioritise improving its financial performance. Currently, TikTok Shop is concentrating on enhancing the user experience and streamlining the purchasing process for Indonesian consumers. They're also fine-tuning their algorithms to optimise subsidy distribution. A key focus for TikTok Shop is developing strategies to attract and retain high-value customers.

This strategy is being carefully formulated with the understanding that if TikTok Shop decides to adopt a more aggressive stance in the near future, significant financial incentives and resources will be exclusively directed towards these high-value users. These priorities would likely impact TikTok Shop's competitive position and financial performance.

The company is adjusting its strategy in Southeast Asia by reducing its competitive activities in the region. Despite this shift, TikTok Shop maintains a strong presence in the established Southeast Asian market. The company's executives view this market as a dependable source of revenue that needs to remain profitable. Interestingly, the funds generated from Southeast Asia are being strategically allocated to support robust growth initiatives in Europe and the United States. By focusing on Southeast Asian ventures, the company aims to build up its financial resources before expanding into other markets such as the UK, North America, or South America.

On January 8th, TikTok launched a ‘Refund without Return’ policy for cross-border orders in Southeast Asia. Refund requests that meet specific criteria, such as order amount within the platform's specified range, will be automatically approved. Merchants will still need to manually approve refunds through the Seller Centre if they choose to process them without requiring a return. [22]

It’s a controversial policy that Pinduoduo and Temu have applied. Many domestic e-commerce companies in China followed suit in 2024, only to mostly roll them back later in the year. The policy is prone to abuse by consumers. It can seriously harm merchants' profitability, especially if it is combined with fines for merchants, as Temu does.

Targets

TikTok has implemented a five-year development plan in the Southeast Asian market, which is now in its fifth year. According to this plan, TikTok aimed to have GMV reach $30 billion in 2024 (accounting for 60% of the global GMV of $50 billion [11]), $50-$60 billion in 2025, and between $70 - $80 billion in 2026. This means that the market size will almost double between 2024 and 2025.

To achieve this ambitious goal, TikTok is adopting several strategies. First, it is committed to improving user interaction and operational efficiency. Second, it plans to expand market share by efficiently utilising volume. In addition, it will focus on improving conversion rates and increasing repurchase rates while optimising customer lifetime value. Through these measures, TikTok is confident that it can further expand its influence and transaction scale in the Southeast Asian market.

However, the actual figures that have been reported have shown less than $23 billion in sales in Southeast Asia in 2024, bringing serious doubts about the feasibility of the targets for 2025 and 2026.

TikTok's e-commerce growth is mainly achieved by grabbing market share from competitors rather than transferring offline business to online. Market competition is expected to contribute 60% to 70% of GMV, while offline conversion will account for 30% to 40%. In the long run, TikTok's e-commerce business GMV in Southeast Asia could reach up to $120 billion.

In the next 1-2 years, when TikTok's GMV reaches a certain scale, it may consider building its own logistics system.

TikTok originally planned to launch in the Spanish market in the summer of 2024, adopting a localised and fully managed service model to provide merchants with a one-stop e-commerce solution. In addition, it also planned to launch business development plans in Germany, Italy, France, and Ireland. [6] However, these plans were temporarily put on hold to focus resources on developing TikTok Shop in the US and Southeast Asia. In December, TikTok finally launched in Spain and Ireland. It is said to be testing in Germany and Italy and preparing for the Netherlands.

We will continue our report on TikTok’s activities outside Asia in part 2 of this series.

Sources

This series of TikTok updates has been compiled from an analysis of more than 20 exclusive interviews with experts from the Six Degrees Intelligence network, augmented with the articles below.

Images by Tech Buzz China’s Ed Sander unless stated otherwise. These images may not be reproduced without Tech Buzz China's prior consent.

[1] Chinesellers 2024-09-30 [2] Rest of World 2025-01-06 [3] Latepost 2024-10-09 [4] 36氪未来消费 2024-07-12 [5] 36氪未来消费 2024-12-27 [6] 白鲸出海 2024-10-16 [7] Chinesellers 2024-11-19 [8] Chinesellers 2024-10-14 [9] Momentum Works 2025-01-06 [10] SMCP 2024-02-05 [11] 36氪未来消费 2023-12-19 [12] 白鲸小编 2023-12-12 [13] Tech in Asia 2023-12-11 [14] New York Times 2024-10-30 [15] 白鲸出海 2024-02-06 [16] Bloomberg 2024-06-12 [17] Momentum Works 2024-06-18 [18] TechPlanet 2024-12-17 [19] New York Times 2024-10-30 [20] Techcrunch 2022-08-03 [21] TikTok 2023-12-03 [22] Chineselllers 2024-12-31 [23] Momentum Works 2024-05-24 [24] Latepost 2024-01-09 [25] Latepost 2024-12-21 [26] Momentum Works 2024-11-15