The Staggering Hippo - Part 2: The Transformation of Alibaba’s Hema (Freshippo)

Introduction

Last month, in Staggering Hippo - Part 1: Ultimate Guide to Alibaba’s Hema (Freshippo) Store Formats, we introduced 12 formats that Alibaba’s Hema launched between 2016 and 2021. We explained which formats failed and which survived and how the Hema strategy was divided between the well-known Hema Xiansheng, ‘going up-market’ with Hema X, and ‘going down-market’ with Hema Outlet and Hema Neighbourhood.

In October 2023, when I led a retail study tour to China, I presented a group of Dutch retailers with these 12 formats during one of the tour’s masterclasses. The retail specialists were baffled by how Hema had stuck that many different formats for different target groups under the same brand umbrella. I argued that while you won’t often come across the same strategy in the West, it might make sense in China. After all, Hema quickly built up a reputation for being a trustworthy brand offering good quality. It seemed to be building on this reputation while targeting new markets, which seemed a better option than launching completely new brands.

While the retail specialists could understand this strategy, they failed to understand what Hema announced to do that same month they visited China: turn the successful Hema Xiansheng stores into discount stores. This resulted in heated discussions in which Hema was often ridiculed for its swaying positioning. “In all my professional career, I have advised brands to always stick to their positioning,” one of the highly experienced retail professionals said.

So, how did Hema transform itself? What’s behind this thinking? And is it working out, some nine months later? In this article, we pick up where the first part of this series left off, in 2023. We’ll discuss how Hema got fixated on competitor Sam’s Club, how it started the discount strategy, and many other recent developments, like the opening of Hema Premier, which seems to be the exact opposite of what Hema was trying to achieve.

The report below is the biggest we have ever produced and about twice the length of a regular newsletter. But instead of creating a third part in this series we decided to share the whole remaining text, allowing us to tell you about other exciting topics in the coming months.

The start of this report is free for all subscribers. The full report is available for our very supportive paying subscribers.

Note: Alibaba calls Hema Freshippo (yes, with one ‘h’) in English, but in this series, we’ll continue to use Hema because it is easier to differentiate the different concepts using this name.

Ed Sander, Research Editor

Hema into 2023

2023 opened well for Hema. In an internal memo, CEO Hou Yi shared that the Hema Xiansheng supermarket chain, Hema’s primary format, had broken even. But ambitious as ever, Hou Yi also wrote that Hema wanted to service 1 billion customers, reach RMB 1 trillion in sales in 10 years and establish 1,000 Hema villages.

By 2023, Hema had very strong product and innovation capabilities. But it was also facing high operating and delivery costs. Competition had grown fiercer and Hema had to battle with both internet companies like Meituan Maicai (now Meituan Xiao Xiang) and traditional giants like Walmart/Sam’s Club. Traditional retail also increased its e-commerce capabilities.

Hema’s online and offline integration model (store + warehouse) and self-delivery were its main competitive strengths. It also had the advantage of tapping into the user data of 800 million monthly active Taobao users, a resource no traditional retail company has available. The mandatory use of the Hema app to pay for offline purchases ensured a full profile of the consumption of its users. All this data also enabled Hema to do faster C2M product development with its supply chain. [1]

Hema certainly has shown some impressive accomplishments. In 8 years, it opened more than 300 Hema Xiansheng stores and became China’s 8th largest supermarket chain. However, for a long time, revenue and fast store expansion were more important than profitability. This typical ‘internet thinking’ had to change. [2]

When Hema started opening stores nationwide, it was convinced the stores should operate locally because different places have different habits and eating patterns. But it soon found it could not compete with local supermarkets that had been operating for decades. After 2021, Hema focussed on innovative products determined by headquarters, supplemented with local speciality products. It also started Hema Neighbourhood and Hema Outlet to accelerate expansion. [3]

According to Alibaba’s financial report for the quarter ending September 2022, the cash flow of most Hema Xiansheng stores had turned positive. Still, with an average margin of 3%, net profit remained meagre. It was mostly the Hema Xiansheng stores in first-tier cities that were profitable; other cities and store formats still had to reach that point.

"Hema still has an unresolved problem: the price is too high. At least in terms of price, we have no obvious competitive advantage. In today's economic environment, we need to solve this problem." CEO Hou Yi said. Hema saw two paths to solve the problem: target the ‘sinking market’ with Hema Outlet and lower the prices of goods for the middle class (at Hema Xiansheng, Hema Premier), as described in part 1 of this series. [4]

A Hema Outlet store in Beijing.

Hema Mall had basically withdrawn from the market, and Hema Outlet had a limited role in making profits. Membership store Hema X’s expansion was slow and stagnated at nine stores. Its service radius was small, so it had limited impact in the market. Hema X also couldn’t price its products too high because of its competition. Overall, these formats made double-digit losses.

Initially, the Hema Outlet stores mainly sell expired and discounted goods. While making less gross margin (or even losses) on products, they also need to deal with reversed logistics from Hema Xiansheng stores (at the end of the day, goods are transported from Hema Xiansheng stores to Hema Outlet stores). In theory, the Outlet stores could reach 30% gross profit, but in reality, profits are meagre. This has led to speculation that Hema Outlet is being used to transfer costs from one format to another.

Hema’s GMV in the first half of 2023 was the same as during the first half of the pandemic year of 2022, not showing significant growth.

To IPO or not to IPO …

On the 28th of March 2023, Alibaba announced its 1+6+N restructuring and announced that several business units and Alibaba-run companies would go public. On April 19th 2023, it was reported that Hema was working on a Hong Kong IPO that could happen within 6 to 12 months. While Hema initially denied the news, the focus on cost reductions in 2022 and more recent leaked news about profitability all pointed in that direction. [5]

On May 18th 2023, Alibaba confirmed that Hema would be one of the first businesses to be spun off in an IPO. At the time, it was said that the IPO could take place as early as late 2023.

In June 2022, Hema had begun seeking additional private funding, but the valuation had shrunk from $10 billion to $6 billion. [6]

All of this begs the question …

How profitable was Hema really?

When cooking up plans for Hema, founder Hou Yi had initially set the following requirements for Hema to succeed: [3]

online transactions should be larger than offline

the average daily order volume of a single online store should exceed 5,000 orders

the app should not require other traffic support and should be able to survive independently

achieve 30-minute delivery within a controllable range under the background of controllable cold chain logistics costs

Hema accomplished all those goals, but has it ever reached profitability?

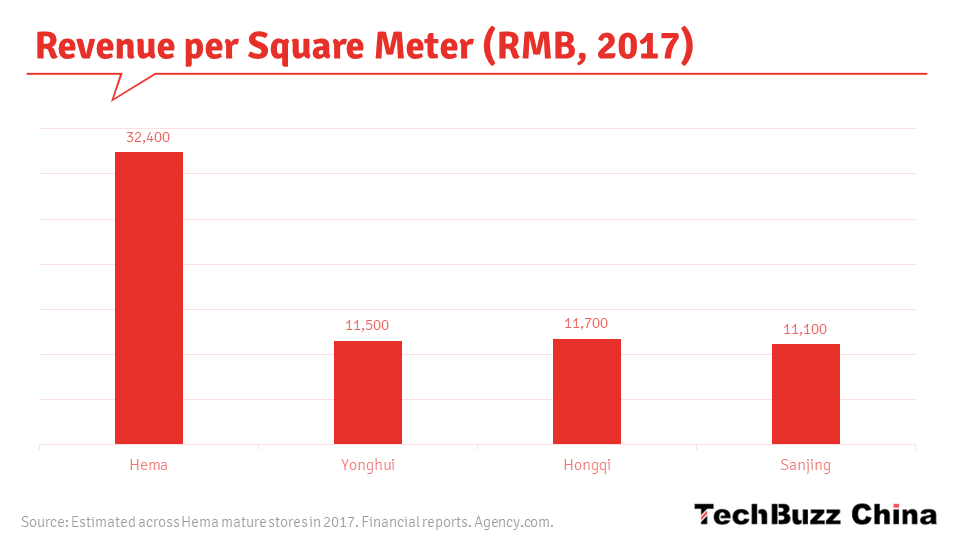

In the early days of Hema, it was eager to share that the sales per square meter of Hema Xiansheng were 3-5 times those of comparable supermarkets. That’s impressive, but it said little about the innovative chain's profitability and the costs of running Hema, which would undoubtedly also be multiples of those ‘comparable supermarkets’.

The costs of opening a Hema store were initially RMB 50 million but later dropped to RMB 30 and 17 million. A 5,000 m2 store would have 300 FTEs, and a 2,000 m2 store would have 100 FTEs (excluding couriers). Meanwhile, a Carrefour store of 30,000 m2 would have a maximum of 200 FTEs, and an 800 m2 ALDI would have 12. Hema’s original management staff came from hypermarkets and added many organisational layers. [2]

The first Hema store in Shanghai became profitable in 1.5 years. However, when it started to expand nationwide, the consumption power of most other cities did not match that of Shanghai. While the chain kept opening new stores, the average sales per m2 dropped from RMB 56,000 in 2016 to 30,000 in 2018. In 2018, some Hema stores suffered losses of tens of millions of yuan for several months, and in 2019, Hema was forced to close a store for the first time. [6]

Then, it launched all the concepts we discussed in part 1 of this series, trying to find a winning model. It invested a billion yuan in community group buying alone. About the opening and closing of store formats, Hou Yi said they were done "to study customer value and focus on the value of a certain type of customer through new stores." He said about opening and closing so many formats: “These decisions were made by me alone, and they were closed by me alone.” [3]

After trying many different formats, Hema’s profitability and GMV growth fell short of expectations within Alibaba. Hema was degraded from an independent business group to a sub-business segment of the B2B business group. [3] At an Alibaba internal conference, Hou Yi even received the ‘Bad Strawberry Award’ given to the worst business. E-commerce professionals estimated that in the first quarter of 2021 alone, Hema's losses had reached about RMB 3 billion. [7]

In 2020, Hema proudly claimed that online sales in Shanghai and Beijing accounted for more than 75% of total sales, and it wanted to increase this to 90% by 2021. However, not long after, Hema CEO Hou Yi changed the positioning and said that more attention should be paid to the logic of physical stores and that online should only take half of total sales. [2] Hema likely realised that being overdependent on online orders with high delivery costs while also running expensive offline retail locations made it difficult to become profitable.

In 2021, Alibaba made Hema responsible for its own profitability. It would get no more blood transfusions from the group. Hema became an independent company and started acting more sensible. But not by finding a stable and reliable business model … [6]

In January 2022, former Hema CEO Hou Yi made it clear in an internal letter that in 2022 the goal was to go from single-store profitability to overall profitability. After GMV targets of RMB 34 and 45 billion in 2021 and 2022, respectively, Hema set itself an ambitious target of RMB 100 billion in 2023. [8] It would reach a little over half of that target.

Revenue and operating profit Hema. [15]

Source: [8]

Hou Yi also applied the brakes and began to reduce costs. The IT engineers were moved from Nanjing to Wuhan, R&D costs were halved, store security and cleaning staff were reduced, and store management had to participate in hands-on work. Operational functions were centralised. [3]

Hema cut down the redundancy of departments and reduced labour costs through layoffs in 2022. It started to optimise procurement costs and reduce related personnel. Staff was centralised, and headquarters and procurement of standardised goods were consolidated. Hema also laid off its private label staff and merged this function with non-private label procurement, reducing internal competition.

In 2022, Hema reduced its operating costs by 5%. Store staff was reduced by 30% between 2021 and April 2023. In Q4 2022 and Q1 2023, Hema Xiansheng achieved profitability for two consecutive quarters. [3]

Hema said about the reorganisation: "We rearranged the most capable and experienced procurement. In just two months, the efficiency of the entire standard product area increased by 7%, and more than 70 million redundant non-performing inventory assets were processed. At the same time, the share of goods from the national supply chain has reached 83%. We will allow more and more suppliers to achieve better scale through similar integration.” [9]

Meanwhile, Hema closed some stores (including some Hema Minis) and improved its private-label offerings. It has also gradually reduced the large seafood and catering it offers. This was once one of its unique selling points, but it came with really high costs. Having visited many Hema stores since 2018, I was often shocked when I arrived around 8 PM and saw the number of dead fish and shrimps the staff would be fishing out of the basins.

Dead fish and prawns at Hema.

For retailers like Sam's Club and Hema, the live products they provide, such as Australian lobster and abalone, although popular with some consumers, are not actually profitable and sometimes even cause serious losses. The profitability of seafood in the aquaculture industry is also a headache for store managers. In general, physical supermarkets face considerable challenges in selling fresh products.

The average sales per store are about RMB 600,000, and the average order value is RMB 60 (the total number of orders per store is 8,000 - 10,000, of which online orders account for 60%). In Shanghai, the daily average sales of a Hema store are usually RMB 700,000 - 800,000. During holidays, it can even reach RMB 2 million. The average gross margin remains between 25% and 30%.

The one-time investment in setting up the store is RMB 20 - 30 million. For stores with an area of 3,000 - 4,000 m2, the rental costs is RMB 3 - 4 per square meter per day. The costs of daily operations include employee salaries (2-3% of gross margin), water, electricity, gas and marketing account for 4-5% of gross margin. Loss of goods is 2-3% of gross margin. Delivery of online orders costs typically 10% of the profit of a single order. Group-level warehouse investment and delivery costs from warehouses to stores should also be considered fixed costs.

In January 2023, Hou Yi stated in an internal memo that Hema Xiansheng (but not the rest of the brand formats) had reached profitability in 2022. "Hema has completed the first phase of the goal as a new retail format." [10] Alibaba’s financial report over the quarter ending December 2022 said that Hema had achieved double-digit growth and YoY losses had been significantly reduced due to improved distribution, operational efficiency and gross margin. It was the first time Alibaba’s quarterly direct sales, of which Hema is part, exceeded RMB 10 billion. [9]

It was later confirmed that Hema Xiansheng had been profitable in the December quarter of 2022 and March quarter of 2023. The financial report for 2023 (ending on 31st of March 2023) stated that Hema had “significantly narrowed losses year-on-year”. [8] But it had yet to achieve full-year profitability.

Rumours have it that despite Hou Yi’s announcements that Hema Xiansheng was profitable at the end of 2022 and the whole umbrella brand was profitable in early 2023, Hema’s costs are too high. Its annual losses would exceed billions of yuan. Without blood transfusions from Alibaba, it would likely not survive in its current form. [11]

While people in the industry have said that Hema would not have been possible without Hou Yi [12], Hou Yi himself has also stated on several occasions that without Alibaba’s financial and technical support, Hema would not have been possible. [13] Since its start, Alibaba has invested at least RMB 10 billion in Hema. It was willing to pay for innovation because "innovation is Alibaba's culture." [3] But as we described in The Collapse of Alibaba’s New Retail? - Part 2: Hypermarkets, Supermarkets and Convenience Stores, a culture that rewards innovation and ‘storytelling’ comes with its own problems.

The plans for an IPO were put on hold in September 2023. Alibaba could only achieve a valuation of $4 billion, much lower than the $10 billion it targeted when it tried to raise private funding in 2022. Blaming this on weak sentiment for consumer stocks, Alibaba decided to wait for more favourable market conditions. [14]

China’s physical retail has struggled with homogeneity. Traditional hypermarkets like Carrefour and Alibaba’s RT-Mart are facing pressure from changing industry trends, leading to continuous store closures.

A report by the China Chain Store and Franchise Association shows that in 2021, 67.1% of supermarket companies saw a year-on-year decrease in sales, 72.2% of companies saw a year-on-year net profit decrease, and 68.4% of companies saw a year-on-year decline in customer traffic. In 2022, nearly 7,000 physical retail stores closed down, of which at least 1,138 are from the supermarket industry. [16]

Sales in the supermarket segment declined 0.4% YoY in 2023. Some players in this market have even seen their revenue drop by more than 10%. [17]

Meanwhile, foreign discount stores (targeting price-sensitive mass consumers) and warehouse-style membership stores like Costco and Sam’s Club (targeting high-income families) have performed well in China, posing challenges to the supply chain-building capabilities of others. They have efficient supply chain management, can achieve global procurement, and provide distinctive product supplies to meet the diverse needs of consumers. They usually adopt a low gross margin strategy, and their primary source of profit comes from the membership fees. Membership renewal rates and annual consumption transaction volume are the main KPIs.

The membership store market in China has been booming in recent years. Market size reached RMB 33.50 billion in 2022, growing 10.1% YoY and is expected to grow to RMB 38.78 billion in 2024. [18] Euromonitor even estimates the growth rate to be nearly 20% and has doubled between 2018 and 2022. According to a report by Bain & Company and Kantar Worldpanel in the first quarter of 2023, the number of Chinese consumers in warehouse-style member stores will increase by 30.3% year-on-year, and the purchase frequency will increase by 12.8%. [19]

And for a change, Hema was not to lead market development but to follow them …

Characteristics discount stores and membership stores. [17]