Need for Speed 2: Can the front-end warehouse model ever be profitable?

MissFresh versus Dingdong Maicai and the market of fresh produce delivery

Still from Dingdong promo clip.

Things that caught our attention

The front-end warehouse model on paper

Two IPOs and the fall of MissFresh

Others using the front-end warehouses

Can the front-end warehouse model be profitable?

Front-end warehouses versus alternatives

Things that caught our attention

James Hu recently interviewed Rui. They talk about AI, starting the Tech Buzz China podcast, distortion of truth, her current work as COO for a start-up and more. You can watch the interview on YouTube.

Earlier this year, Ed delivered a two-part session on how Chinese e-commerce changed in the past decade and how some of these innovations are coming our way. The session was filmed, and the first half on the evolution of e-commerce in China is now available on YouTube.

EV maker BYD sold 2.07 million vehicles in the first nine months of 2023, up 76% from a year earlier. We wrote about BYD earlier this month in Manpower over Machines: The Calculated Gamble of BYD.

Temu, Pinduoduo’s cross-border platform, is now available in 47 countries. Temu is rumoured to be planning to charge merchants a 0.5% commission for outsourced customer service. (source) Temu has denied the rumours.

Temu has also been shown to impact the bargain retail business. We wrote extensively about Temu in Temu: from $0 to $3 billion in 10 months.

Cotti Coffee has been recruiting franchisers outside China. We wrote about Cotti last months in Coffee Wars: How the arrival of Cotti has sparked a price war.

Introduction

A few months ago, we explored two different forms of instant retail: delivering goods within one hour from local businesses.

In Redefining Fresh: Alibaba's Freshippo and the New Frontier in Grocery Business, our article on Alibaba’s Hema supermarkets (Freshippo), we saw an example of the store + warehouse model. In this model, orders are picked in a supermarket and attached warehouse and are home-delivered within a 3-5 km radius. Some other supermarket chains like JD.com’s 7Fresh (七鲜 Qixian) and Yonghui have also followed this model, while Meituan pulled the plug on its Ella (小象 Xiaoxiang) Hema-clone a few years ago.

In Need for Speed: Instant Retail, we discussed a different form of instant retail in which marketplace platforms like Meituan’s Shangou, Dada Nexus’ JD Daojia and Alibaba’s Ele.me enable offline retailers to open online shops and provide them with couriers for home-delivery. Many Chinese retailers, from the smallest pop-and-mom shops to big chains like Walmart, have used these third-party services, and some have seen the share of online orders in their total sales grow to as much as 50% through this model.

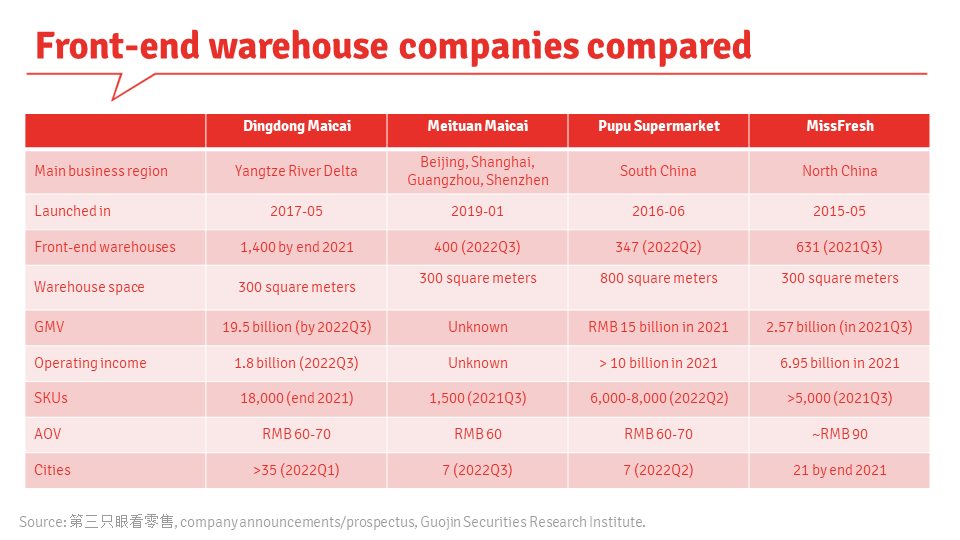

In this new article (and an upcoming one on Meituan), we will explore the remaining business model of front-end warehouses (前置仓 qian zhi cang). This is the domain of businesses like Meituan Maicai, Dingdong Maicai and the now-defunct MissFresh. How do these platforms work, and are they profitable? Why did Missfresh perish while Dingdong survived? And who is Pupu, another important player in the market?

We hope you’ll enjoy this deep dive into the sector.

Freya Zhang, Ed Sander & Rui Ma

(Click on the images above for information on the Tech Buzz China team.)

The front-end warehouse model on paper

As with other forms of grocery delivery, the interest of China's internet companies in front-end warehouses lies in the frequency of traffic they can generate for their apps. Having the consumer return several times a week offers recurring opportunities to pull them further into the ecosystems and sell more goods and services than just groceries. Among the leading players, this is especially true for Meituan.

Unlike Hema and JD.com's 7Fresh, companies that operate through front-end warehouses typically have no stores but only small- to medium-sized warehouses close to residential areas or office buildings. These front-end warehouses, sometimes called DMWs (Distributed Mini Warehouse), normally deliver within an hour in a radius of 3 kilometres. Front-end warehouses have multiple temperature facilities such as refrigerators, freezers, and sometimes reheating for fresh product processing.

Still from Dingdong promo clip.

Rental costs for front-end warehouses are said to be lower than for a store (according to MissFresh, just one-third), and they also allow for storage of more products on the same surface. Shops often cover 800 to 1000 square metres, and a front-end warehouse is 200 to 400 square metres. As a result, the sales per square metre is about three to four times higher than at a supermarket, or so MissFresh claimed. That might be true, but the warehouses also have limited SKUs, putting a ceiling on the average order value.

Front-end warehouse companies usually have a high proportion of fresh produce, around 55%. The most prominent feature is the aquatic and seafood categories. This category doesn’t just attract many customers; it also provides high margins.

In traditional retail companies in China, spoilage rates for fresh produce are often high because retailers, for cost reasons, usually do not use refrigerated transport between regional warehouses and shops. Front-end warehouses tend to purchase many of their products directly from the source and operate their own logistics chain with only a regional (city) warehouse and a front-end warehouse between the farmer and consumer. As such, the supply chain is much shorter than for supermarkets, which in China usually have to deal with various layers of producers and wholesalers. Products, therefore, have a shorter total transport time, and less fresh produce is lost. MissFresh, for instance, claimed to be able to limit spoilage loss to 2.5%.

In China, regular supermarkets have a catchment area of 500 metres to 1 kilometre. Front-end warehouses extend this to 3 kilometres through home delivery. A company can ensure good coverage with multiple front-end warehouses in a city. If the population density is high, the warehouses need to be closer together to guarantee fast delivery and to keep delivery profitable. Due to the high population density in Chinese cities, MissFresh delivery drivers could deliver around 60 to 70 orders daily, and a courier could take 6 or 7 orders per trip.

Population density is often lower outside city centres, so the delivery time is longer. The front-end warehouse model no longer works if the population density is too low. Hence, companies using this model tend to focus on China's 30 to 40 largest cities. In addition to the higher population density, consumers in these cities have a busier life, more disposable income and are more interested in the convenience of grocery delivery. But as we will see, even those cities can prove to be a challenge for the model.

Indeed, let's not get too enthusiastic about the supposed advantages of front-end warehouses. The model has proven difficult to operate unless there is enough scale (per warehouse). Spreading resources too thinly can lead to disaster, as we will see.

In addition to the cold chain, inventory management is challenging for these platforms, just like for supermarkets. Which products should you put in those front-end warehouses? On the one hand, you must avoid stocking too many products and throw away as few unsold perishable products as possible. On the other hand, you could have too few products in stock and lose customers because of frequent out-of-stocks.

The players in this sector use artificial intelligence and big data to try and solve these problems. For example, based on available data about consumers in the catchment area, Meituan Maicai's product range is adapted to consumers' needs and preferences. Dingdong also uses big data to predict future orders and minimise waste. In their apps, they give individual customers recommendations based on data to increase the order value and offload leftover stock.

Front-end warehouses compared to other grocery delivery models. For more on community group buying, read our earlier report.

Because of the investment costs, front-end warehouse players usually started in a few cities and, if possible, in places where the competition was not yet present. A few years ago, you could see different players popping up in various parts of China.

The model snowballed since it was introduced in 2015, and according to iResearch, its market was RMB 33.7 billion five years later. At that time, it was expected to grow to RMB 306.8 billion by 2025, and Missfresh and Dingdong held 23% and 39% market share respectively. [1]

Direct sourcing

It is well-known that only selling fresh produce is not profitable because of low prices and fierce (price) competition. Like other fresh-food e-commerce companies, front-end warehouse companies try to shorten the supply chain to minimise procurement costs and spoilage. They cut out wholesale suppliers and middlemen through direct sourcing by buying goods directly from farmers. They sometimes even set up self-operated farms and processing factories.

For more popular product categories, they adopt a series of supply chain strategies from procurement to fulfilment, working backwards in the supply chain when the customer and order scale are large enough. With the accumulated data, they can predict order volume per day and season, allowing them to cooperate with suppliers to obtain more stable supply and lower costs.

Some large platforms choose direct sourcing from the origin for high-volume products like seafood, potatoes and vegetables. These commodities usually are not processed and shipped straight to the transit or regional warehouses. The elimination of middlemen reduced costs, and shortening the delivery time improves product quality. No direct source will be interested if the sales quantity is too small. Unlike secondary suppliers, source suppliers usually only deliver full trucks. Therefore, no fresh-food e-commerce company can directly source all of its assortment.

Still from MissFresh promo clip.

Products purchased from the place of origin need to be cleaned, selected and sometimes processed. Therefore, it is sometimes necessary to establish origin warehouses close to the source to improve the efficiency of packaging, sorting and delivery. While direct sourcing means lower procurement costs, it often increases investments in the required origin and processing warehouses.

Direct sourcing is a trend you don’t just see with front-end warehouses but has also played an essential role in Hema’s recent profitability. In the future, whichever fresh food e-commerce company can promote direct sourcing faster will get better development opportunities.

Marketplace platforms like JD Daojia and Meituan Shangou, discussed in Need for Speed: Instant Retail, don’t engage in direct sourcing. Their speciality lies in quickly getting goods from A to B, not in controlling the supply chain. They aren’t retailers; they are service providers.

Let’s look at the leading players that have dominated the front-end warehouse sector in recent years.

MissFresh

MissFresh's story is one of initial success, followed by a crash and burn. It tells us a lot about Chinese internet business and is therefore worth re-evaluating.

Still from MissFresh promo clip.

Founded in 2014 by ‘boy wonder’ Xu Zheng, MissFresh (每日优鲜, Meiri Youxian) was the first player to pioneer the front-end warehouse model. [2] Each warehouse had refrigerated storage capacity, one manager, 5-10 sorting staff and 10-20 delivery staff, bringing goods to the consumer in 30-60 minutes in a 3 km radius. Through customer subsidies, it hoped to develop habits of frequent online shopping with its customers. [3] MissFresh claimed that delivery from a front-end warehouse was about ten times more efficient than from a store and used this cost advantage to compete with supermarkets on price.

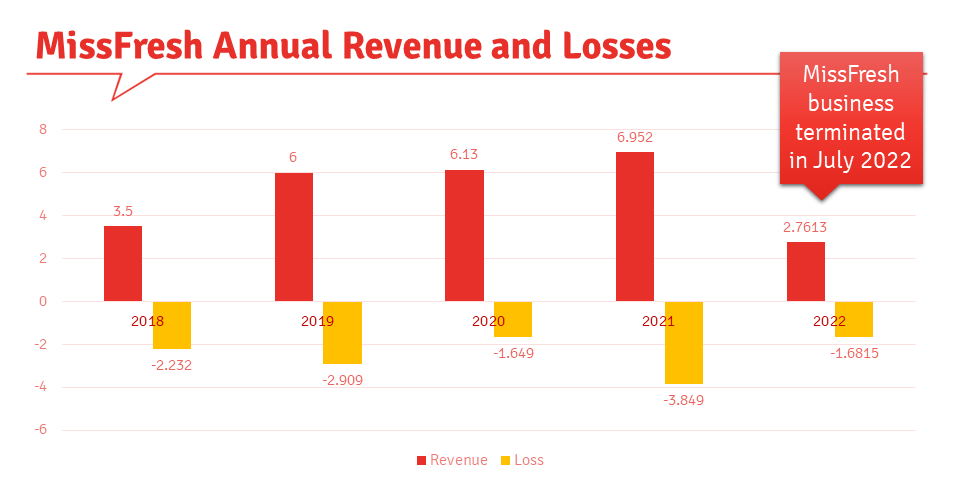

MissFresh was backed by Tencent with a $450 million funding in 2018. In that year, MissFresh sold RMB 10 billion worth of products. According to Trustdata, the company had a 50% share of the online market for fresh products in 2019, followed by Hema with approximately 26%. [4]

At the start of 2019, MissFresh had set a GMV target of 20 billion and full profitability in the same year. However, its IPO prospectus showed that 2019 only saw RMB 7.59 billion GMV and a 2.9 billion loss. [3] As we will see, it would never reach profitability…

MissFresh claims to source 93% of fresh products and 80% of all products directly from their source and have a loss rate of only 2.5%. [1] It had a minimum spend of RMB 39 for free delivery. In 2020, its customers ordered 8.2 items per order and in Q2 2021, it saw an average order value (AOV) of RMB 96.1 and an average number of daily orders per warehouse of 417. [5]

On average, MissFresh customers would use the app four times a month. Older customers bought slightly more frequently than young people: fifty and sixty-year-olds bought every one or two days, while thirty-year-olds sometimes bought only once every two weeks. The latter group does less home cooking, buys more goods at once, and stocks up.

Still from MissFresh promo clip.

The number of SKUs MissFresh offered grew as it added new product categories; when it launched, it had only 800. The limited number of SKUs gave the company a good negotiating position with its suppliers, being able to buy in large volumes. Of the SKUs that MissFresh supplied, about 70% were the same throughout China, and 30% were regionally selected and purchased. Eventually, MissFresh settled on 4,000 SKUs, about a tenth of what many supermarkets offer on their shelves. [6] It could, however, also deliver another 20,000 SKUs the next day. [1]

Fewer variants and, as a result, larger volumes provided benefits in the cold chain. Different products have to be transported at different temperatures. For example, apples are sensitive to cold, while durians should be transported frozen. In other words, they cannot go to a warehouse in the same truck. Larger volumes, however, ensure well-filled trucks and, therefore, lower logistics costs.

Jack Yang, at the time, Chief Growth Officer at MissFresh, shared some of the company’s strategies in a Tech Buzz China Live Cast. “MissFresh was also driven by penetration of mini-programs among 500 million users. We were creating a lot of gamification mechanisms, such as giving cash rewards to users who shared a red envelope with their groups. WeChat allowed that and in some ways encouraged us to give money away to groups to grow the penetration of mini programs.”

“Because labour was still relatively cheap in China, we relied on many foot soldiers, in-person salespeople, to drive our growth. For example, we hired tens of thousands of foot soldiers to go from apartment to apartment to do in-person sales. We asked people to join a WeChat group, and if you joined, we gave you a 5 yuan coupon. We created a new group each time a group reached about 200 to 300 people. We used bots to moderate these groups. We did a lot of these relatively manual things. And because the labour is cheap, were still able to scale these operations to 12 cities and have coverage of millions of users.”

By mid-2020, MissFresh operated over 1,500 front-end warehouses, serving 25 million monthly active customers. When it opened a new warehouse in a city it was already active in, it claimed to break even in three months. In new cities, it would take six to nine months.

MissFresh app.

Funding dries up

Until 2018, MissFresh's financing went smoothly, with investors, among which Tencent, as mentioned, hoping the front-end warehouse model would bring new vitality to the challenging fresh food industry. As early as 2018, Alibaba, Meituan, and JD.com all intended to acquire MissFresh but stopped pursuing this as they considered the firm’s valuation too high. [7]

MissFresh tried various diversification strategies to grow its business, including a Pinduoduo-like social commerce platform. Seeing Luckin's initial success, MissFresh bought hundreds of commercial coffee machines worth tens of millions of yuan when it planned to sell coffee and meals. Most of these machines were left to gather dust in warehouses. Indeed, these experiments were failures, and MissFresh lost RMB 3 billion in 2019, almost all the funding it had raised in the previous year. [3]

After receiving RMB 10 billion in funding since its 2014 founding, investors started losing interest in MissFresh. After 2018, even Tencent scaled down its investments in the company, never leading another funding round again. The only reason Tencent continued to make smaller investments probably was that MissFresh would lose other investors' trust without Tencent’s endorsement. MissFresh had approached JD.com for funding, but the company kindly declined because it didn’t see improving unit economics. [3]

By 2019, US venture capitalists had stopped investing in MissFresh. The company was running out of cash, but the sudden explosion of business during the pandemic temporarily saved it. When many Chinese had to stay in their apartments during strict lockdowns, grocery delivery was one of the few ways to get your hands on food, and it renewed interest among investors in the sector. During Spring Festival 2020, daily orders tripled compared to the previous month, and the AOV rose from RMB 80 to RMB 120. Gross profit increased to 25%, three times the previous year's. [3]

MissFresh got two more investments totalling RMB 5 billion and continued to use most of this funding for customer subsidies. When these stopped, the daily volume of orders dropped again. MissFresh received another funding from Qingdao’s local government on the condition it would move its HQ to that coastal town in Shandong. [3] The same happened when the city of Changshu offered an investment, giving MissFresh two main offices.

With no more private and government investments left to draw from, MissFresh could only go public. While it planned an IPO, MissFresh’s front-end warehouses dropped from around 1,500 to 631 in number. The company claimed that small warehouses of 100 square metres had been merged into bigger 300 square metres ones and that there was no effect on scale. [8] Meanwhile, MissFresh’s main competitor, Dingdong, had expanded to 1,136 warehouses.

After the 2020 funding, MissFresh claimed to have reached nationwide positive cash flow for six months. However, the prospectus and financial reports that were issued later showed a negative cash flow in the first half of that year at RMB -745 million. It wasn’t the first time MissFresh had shown questionable financial reporting. In 2016, MissFresh had claimed to have broken even in Beijing. A journalist later found out that it was due to adjustments in financial calculations; user subsidies and marketing expenses for Beijing had been moved to the cost centre of headquarters. [3]

MissFresh kept intentionally downplaying market risks, omitting RMB 830 million in short-term loans and RMB 248 million in convertible bonds, together 30% of their liabilities, from the first version of their prospectus. The U.S. Securities and Exchange Commission (SEC) forced MissFresh to make these risks more visible in later versions. [3]

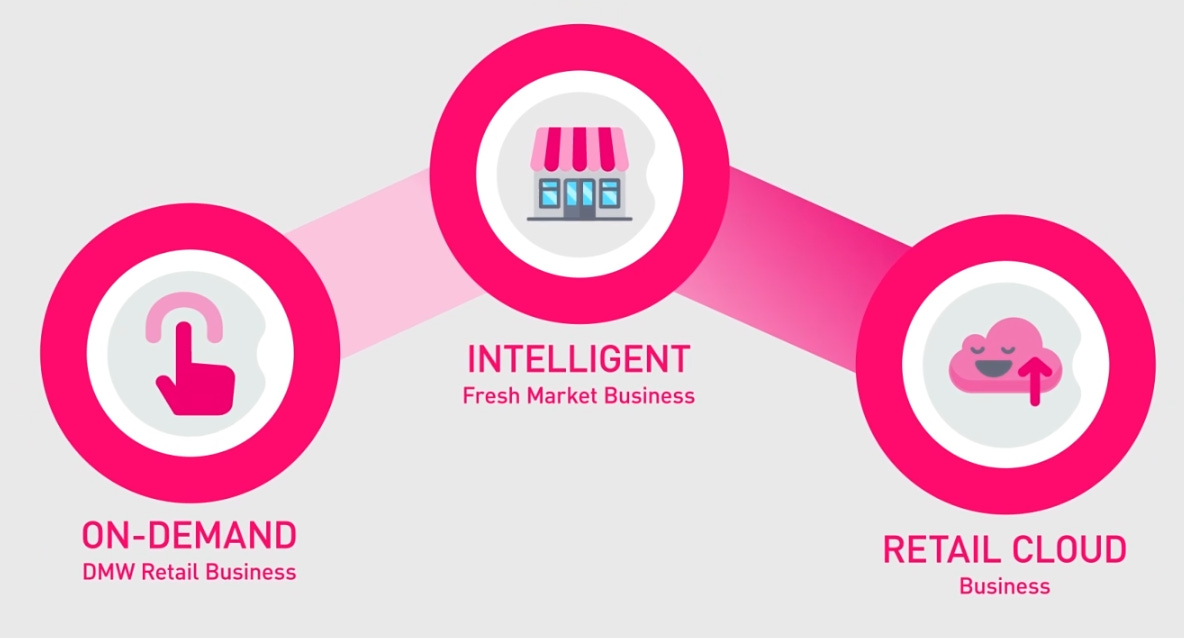

Going ‘Smart’

While it was preparing for its IPO, MissFresh tried new initiatives like ‘intelligent fresh markets’ and ‘retail cloud’, the investments of which put even more pressure on its operating results.

Still from MissFresh promo clip.

The concept of Intelligent Fresh Market was based on renting vegetable markets from governments and subcontracting spaces to vendors with a profit margin. It also provided the vendors with paid SaaS tools for bookkeeping, online marketing, CRM and business planning (far too fancy a service for the average vegetable seller if you ask us). At the markets, it would also set up online shops with pick-up of goods featuring FMCG that were usually only available in supermarkets. Vendors would get a share of the revenue of such products. MissFresh claimed to operate 34 fresh markets in 15 cities in June 2021, at a net margin of 10-15%. [5]

Retail Cloud, launched in cooperation with Tencent Smart Retail, involved packaging MissFresh’s technical capabilities as SaaS for supermarket chains in lower-tier cities. It was meant to help SME supermarkets create and operate online stores and campaigns in mini-programs and optimise their logistics. MissFresh would get a share of the incremental profit. At the time of the IPO, MissFresh was testing the service with just one client. [5] One year later, by mid-2022, MissFresh claimed the intelligent fresh market business had expanded to 20 cities and that 50 retail companies were using its retail cloud. [36]

MissFresh also set up a next-day delivery service with JD.com and made half its products available on JD.com and JD Daojia. But all these new initiatives only made up 5% of revenue by Q3 2021. [3] They did look fancy in the IPO PR though … and the company said it would invest 40% of the funds raised in intelligent fresh markets and retail cloud to help it penetrate lower-tier cities.

Let’s leave MissFresh for a moment and look at its biggest competitor. Until 2018, MissFresh had acquired most of its customers through social channels, and because of the lack of direct competitors, the acquisition costs weren't high. But that all changed with the arrival of Dingdong Maicai that same year.

Dingdong Maicai

Another party in the front-end warehouse market is Dingdong Maicai (叮咚买菜), founded in 2017 by wholesale veteran Liang Changlin. Dingdong burned RMB 300 million in savings from Liang's previous entrepreneurial ventures in its first year. One hundred fifty investment institutions rejected funding requests, and if it weren't for RMB 45 million in funding in May 2018, Dingdong would not have seen the end of that year. Further funding rounds proved much easier, and Liang even got offered more capital than he needed. [8]

Still from Dingdong promo clip.

While MissFresh expanded around the country, Dingdong initially stuck to Shanghai and the surrounding area. It also stuck to its product category of fresh fruit and vegetables while competitors expanded their categories to increase average order value. [8] Instead, Dingdong emphasised economies of scale and only offered around 2,000 SKUs, half of what MissFresh offered for instant delivery. It focused more on fresh products and kitchen consumables, serving as a substitute for fresh markets. It gave Dingdong a higher single-product concentration and better bargaining power with suppliers than most other retailers. [5]

Like MissFresh, Dingdong delivered within a radius of 3 kilometres within 30 minutes. But unlike MissFresh, it provided free delivery without a minimum spend requirement. In 2021, customers typically purchased fewer items per order than with MissFresh but bought more frequently. Dingdong's AOV was RMB 56.8 (MissFresh had RMB 96.1), and the average daily order per warehouse reached 913, more than twice that of MissFresh. [5]

Still from Dingdong promo clip.

While MissFresh focused on fruit until early 2019, Dingdong focused on fresh vegetables. Dingdong also established self-operated farms and pork processing factories to reduce supply chain costs. It launched 600 private labels in 2021, 60% of which are self-processed or produced, which could increase profit margins by 10-30% compared to brand suppliers. Meanwhile, MissFresh's attempts at private labels were mostly still produced by suppliers and had much lower cost reductions. [3]

Dingdong customers were, on average, slightly older (40-60 years) than those of MissFresh (30-50 years). The core of its users consisted of urban households aged 26-45. Customers are broken down into the following segments: [9]

high-quality consumption focussed, aged 30-50, accounting for 60%;

health focussed silver-haired group over 50 years old, accounting for 20%;

young people under 30 years old with emerging demand, accounting for 20%.

Dingdong invested in infrastructure: 1,000 front-end warehouses, 60 city sorting centres, ten food R&D facilities and processing plants, focussing on quality control and R&D. [8] In Q1 2021, Dingdong processed 900,000 orders per day and generated RMB 1.5 billion in monthly sales in 27 cities. [10]

Unlike MissFresh, which used some franchised warehouses that paid a RMB 60,000 deposit, Dingdong was fully self-operated. Thus, Dingdong had higher costs, and MissFresh could initially expand faster, but MissFresh had less control over quality. It tried to fight Dingdong in Dingdong's home base of Shanghai, but in Q1 2020, Dingdong overtook its competitor in daily orders, with better performance efficiency, repurchase rate and other KPIs to boot. [3]

Like MissFresh, Dingdong benefited from the 2020 pandemic and demand for online grocery delivery, surpassing MissFresh and even Alibaba’s Hema (Freshippo). [8] In the first half of 2020, Dingdong's orders in Shanghai increased by 300% and its number of users by 200%. In Q3 2020, Dingdong expanded to Beijing, Tianjin and other cities. Xiamen and Chongqing followed, and more than 20 second and third-tier cities. However, most warehouses outside first-tier cities could not meet their KPIs. The average daily orders lay between 300 and 600, and warehouses required substantial subsidising to maintain volume. [8]

According to their IPO prospectuses, in 2020, MissFresh and Dingdong had average order values of RMB 95 and 57, respectively. MissFresh was operating in 16 cities and Dingdong in 36. MissFresh held 23% market share and Dingdong 39%. [5]

Dingdong app.

Two IPOs and the fall of MissFresh

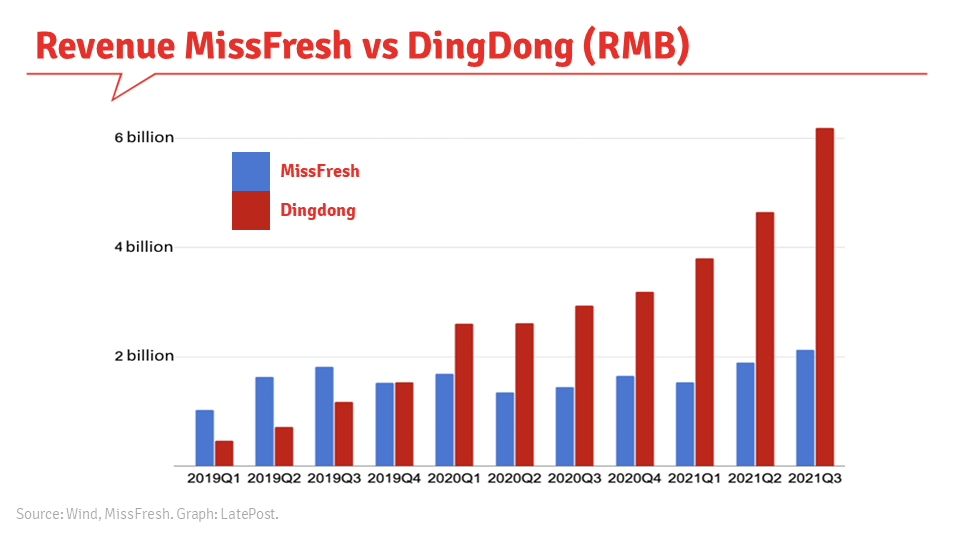

At the end of 2020, MissFresh released its listing plan, closely followed by Dingdong. Both companies remained unprofitable and needed new funding to support their development ... or even survival. Both planned to go public on June 29 2021, and both hoped to raise $300 million.

On June 24th, MissFresh suddenly broke off its IPO roadshow and announced it would go public the next day at a valuation of $3.2 billion, a move intended to snipe Dingdong. MissFresh raised $273 million on Nasdaq with a share price of $13. But on the day of the listing, shares plummeted 26% to $9.60, making some funds that had planned to invest in Dingdong pull out. Dingdong reacted by lowering its funding target to $80 million. [3] Its shares sold at $23.50, valuing it at around $5 billion.

After their IPOs, MissFresh and Dingdong had cash to survive for 1.5 and 1 year, respectively. The two needed to quickly become profitable or find extra funding before money would run out again. With their poorly performing IPOs, finding new investors would prove difficult. [11]

Please note: the rest of this article is only available to paid subscribers.

Dingdong shifts to efficiency

Around the time of the IPO, Dingdong opened three convenience stores in office buildings in Shanghai’s Pudong district: Good Morning Ding Dong (叮咚早上好, Dingdong Zao Shang Hao). It planned to open ten more in the city. Like Luckin Coffee stores, the convenience stores only accepted orders through the mobile app. The store provided breakfast for white-collar workers through a ‘central kitchen + reheating’ model. [12] None of these convenience stores still seem operational at the time of writing.

In 2020 and 2021, Dingdong expanded from 17 to 37 cities and from 700 to 1,400 warehouses to maintain the leading position it had gained in the market. But it found these created severe losses. Dingdong had placed hundreds of millions of adverts on Douyin and other channels. User acquisition costs were RMB 130, and retention was only 28%. It had increased its local recruitment team to 1,600 people. But most of the new users recruited with coupons never returned. To reach their targets, the local recruiters had often signed up multiple members of one household with the promise of free goods. Dingdong lost RMB 6.4 billion in 2021. Many wondered if it would be sustainable, lacking extreme circumstances like the pandemic. [8]

In mid-August 2021, Dingdong changed its strategy from ‘scale has priority, while taking into account efficiency’ to ‘efficiency has priority, taking into account scale'. It realised that if the company was to survive in the challenging funding climate of tech rectification that was in full swing, it had to become self-sufficient instead of depending on capital. Focus shifted to penetration rate, purchase frequency, average order value, etc. [8]

Dingdong scrapped its 1,600 local recruiters, online advertising, and subsidies and got rid of users who only came for free stuff. Plans for new warehouses in Henan and Shandong were abandoned. Local management had to strictly control the number of employees and negotiate cost reductions with landlords. Meanwhile, pre-made dishes, private label products, and self-developed and self-produced products had to differentiate Dingdong from the competition and help improve gross margins and purchase frequency. It aimed to increase its ratio of private label products from 7.2% to 20% in 2022. [8]

Dingdong started a strict regime for its local operations, assessing multiple indicators such as labour efficiency, order volume, on-time rate, cargo damage, etc. Employees who failed to meet standards saw their wages reduced. It increased the target for processed daily warehouse and delivery staff orders from 90 and 60, respectively, to 130 and 80. [8]

In a front-end warehouse that had 900 orders per day, there would previously be ten employees:

4 for order picking during the night

4 for sorting and packaging during the day

1 for quality control

1 for processing and packing seafood products

After the new targets were set, this was reduced to 6.9 employees, requiring the remaining staff to work longer. [8]

Still from Dingdong promo clip.

In the last quarter of 2021, Dingdong became profitable in the Shanghai area, with an average order value of RMB 66, daily orders per warehouse of more than 1,200 and a gross profit margin of more than 28%. Some analysts questioned the figures since profits were achieved while raising the threshold for delivery and lowering subsidies, which usually hurt the number of orders. Indeed, Dingdong's sales had fallen 15%. While Shanghai performed well, in Beijing, the average daily orders per warehouse dropped by 20-30% from 1,000-1,200 to 800-1,000. [8]

Dingdong had more than 20 private labels, including for bakery, pastry, milk, seasoning and prepared dishes. Private-label products are exempt from channel and marketing costs, and product costs can generally be reduced by 20-30%. About 80% of Dingdong’s sales initially consisted of fresh fruit and vegetables. [8] It shrunk the share of fresh products to 60% and added nearly 600 private label and prepared dishes SKUs. The latter contributed RMB 900 million to Dingdong’s sales in Q4 2021. [8]

By December 2021, monthly full-company losses had narrowed to RMB 200 million, and Dingdong hoped to be profitable within ten months. [8]

When Shanghai went into lockdown in 2022, it was again Dingdong and its seven sorting & processing warehouses and 170 front-end warehouses that kept Shanghai fed. More than a hundred other Shanghai warehouses had temporarily been closed because of the pandemic, while demand had more than doubled. Dingdong provided about 10% of Shanghai’s food needs at the time. [8]

During the lockdown, an order picker in a 300 square metre front-end warehouse processed about 500 orders a day, while couriers delivered 200 a day, two or three times as much as before the lockdown, working 18 hours from 6 AM to 0 PM. Dingdong’s reliability increased its stock price by 50% during this period. [8]

Dingdong still saw its fair amount of challenges in 2022. In March, it received bad press about hygiene and product quality at one of its warehouses in Beijing’s Haidian district. Dead fish were reportedly sold as fresh fish. Dingdong implemented a strict supervision and punishment system for violations: RMB 800 fine per violation and dismissal after three strikes.

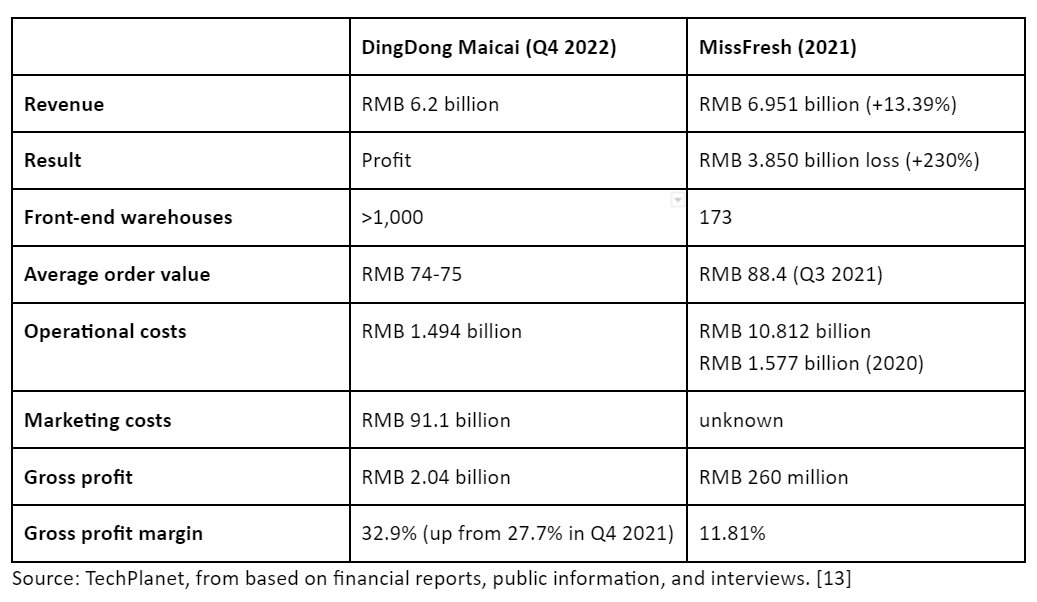

Dingdong’s marketing spend ratio had dropped from 6.5% in Q4 2021 to 1.47% in Q4 2022 and was 2.19% for the whole of 2022, the lowest in its five years of existence. Its gross profit margin increased from 27.7% to 33.2% in the same period. [13] Dingdong’s share of goods directly purchased from the source had reached 79%, and its private labels accounted for 11.4% of its total revenue. [32]

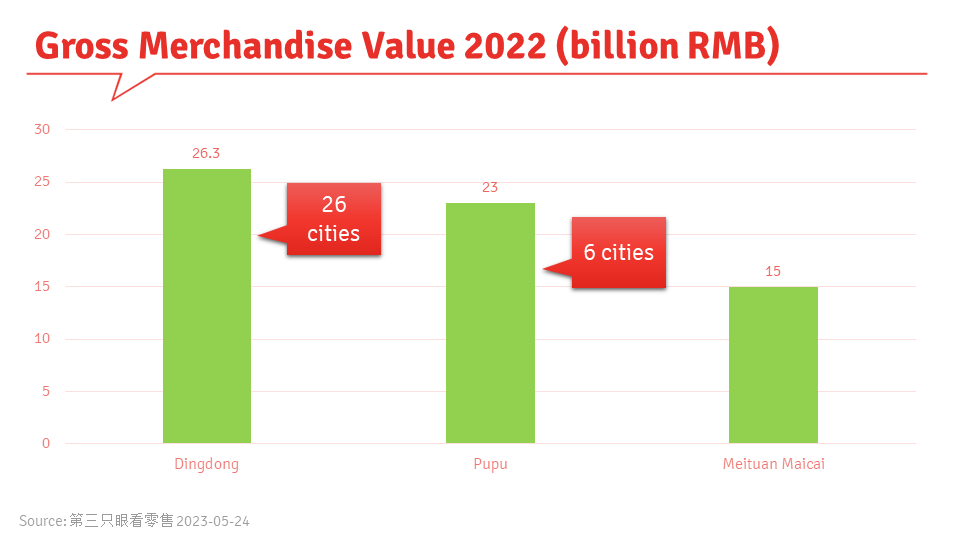

When Dingdong released its Q4 2022 financial report, it showed it had achieved its first net profit under non-GAAP standards of RMB 49.88 million. It had moved from profitability in the Shanghai region in Q4 2021 to national profitability in two years, six years since its establishment. [13] In 2022, Hema had a GMV of RMB 34 billion, while Dingdong had RMB 26.25 billion. [14]

Meanwhile, its main competitor hadn’t fared so well…

MissFresh in trouble

At the time of its IPO, MissFresh had planned to become profitable by 2024-2025 by increasing the average order value from RMB 96 to RMB 105-110, decreasing subsidies, increasing fulfilment efficiency (more orders per courier) and improving gross margin to 25% by adding high-margin FMCG and private labels to the product mix, optimising the supply chain and charging delivery fees. [5]

During the lockdown in Shanghai, Dingdong's operations remained stable, and it seized the opportunity to deliver groceries to citizens who could not leave their houses, turning losses into profits. Meanwhile, MissFresh had to close businesses. In the first half of 2021, MissFresh spent RMB 20 million each month on Douyin and other channels to buy traffic and issued large coupons (‘199 minus 100 RMB').

In Q3 2021, MissFresh’s gross profit was 12%, with a little less than RMB 2 billion in unrestricted cash left, while suppliers and loans that needed to be paid within one year were RMB 2.4 billion. Competitor Dingdong’s gross profit margin was 17% at the time but continued to increase to 30+%.

After the listing, MissFresh lost RMB 46 on every RMB 100 of goods it sold and closed 2021 with a loss of RMB 3.7 billion (almost double the money it had raised with the IPO), bringing its total loss to RMB 10.5 billion since its founding. [3]

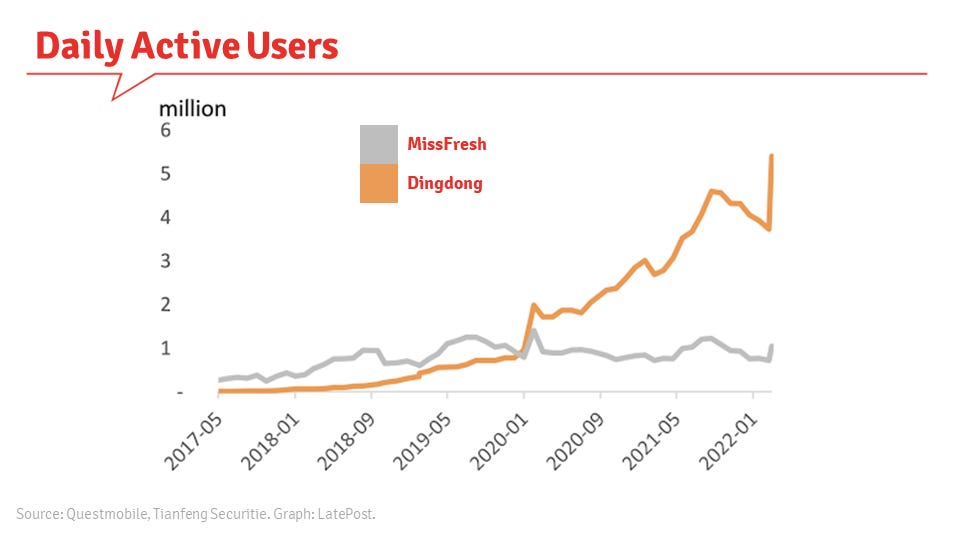

After the IPO, MissFresh’s management thought the $300 million it raised would help it become profitable in 2022. However, the company’s problems only grew, and by mid-2022, the company expected its highest annual loss ever at RMB 3.7 billion, while it did not see substantial growth in users or sales. After the temporary Q1 2020 peak that the pandemic brought, MAU and DAU did not increase, while Dingdong kept showing significant growth. [3]

One of MissFresh's other problems was internal corruption, with warehouse staff reselling discounted products for their own profits and making kick-back deals with warehouse owners, who would rent them out at higher prices to MissFresh. Of the 1,200 electric vehicles MissFresh deployed in Beijing, only 800 were used. The rest had been sold or used for private purposes. [3]

MissFresh laid off 200 staff members in September 2021 and continued trying other cost savings, like halving the staff’s bonuses. In August 2021, some suppliers started noticing delays in payments. For renewed contracts, payment terms were extended from 60 to 90 days. By Q1 2022, some suppliers stopped their deliveries. In new negotiations, MissFresh was able to retain some suppliers but had to lower the payment terms to one month or even one week and pay higher prices. It convinced some reluctant suppliers by telling them they were a US-listed company backed by the Qingdao government. [3]

MissFresh's financial report for 2021, released in November 2022, showed close to RMB 7 billion in revenue but a net loss of more than RMB 3.8 billion.

In January 2022, MissFresh tried unsuccessfully to wow investors with plans to add more 3R (ready-to-cook, ready-to-heat, and ready-to-eat) products to its assortment, promising improving margins. [15] It also started a livestream channel on Douyin and a Douyin Shop where viewers could buy products for delivery within an hour in Beijing and Shanghai. [16]

In May 2022, more employees were laid off without compensation. In June, the company’s limited funds were used to pay staff, while suppliers had to wait. Another 20% of staff had been laid off, and the remaining middle and senior managers saw their salaries cut by 50%. [3]

After the listing, nobody was willing to invest in MissFresh anymore. A supposed $200 million funding by Shanxi Donghui, a Chinese multi-conglomerate in the metal and energy sector, never came through. JD.com considered buying MissFresh because of the value of its front-end warehouses for instant retail business but decided against it because of MissFresh’s enormous debts. [17]

After MissFresh burned RMB 14 billion in funding, including money from state-owned enterprises and local governments, and never becoming profitable, it fell into a crisis in the summer of 2022…

It had already shrunk the number of cities it was active in from 17 to just Beijing, Shanghai, Tianjin and Langfang (a city between Tianjin and Beijing). Its stock price had fallen to just 14 dollar cents. [18]

On June 30 2022, MissFresh had RMB 2.24 billion outstanding in accounts payable (which MissFresh denied), while it had RMB 108 million in its 323 bank accounts (we assume groups of warehouses had their own bank account). [3]

In early July 2022, Missfresh admitted it had overstated its revenue in its next-day delivery business unit for the first nine months of 2021 by 14% (RMB 677 million). This led to the dismissal of employees involved in the fraud, voluntary departure of executives and lawsuits. [19]

On July 28th 2022, just one year after its IPO and after all its fundraising stories about "hundred cities, ten thousand warehouses and one hundred million households", MissFresh terminated instant deliveries from its front-end warehouses and its retail cloud business. [3] Suppliers that demanded to be paid were told they would only receive half of their invoices, spread out over ten months. Staff on a business trip had to buy return tickets with their own money. [17]

Scrambling for cash, in August 2022, MissFresh sold its vending machine business Bianligou, consisting of 14,000 machines, for RMB 30 million, or just RMB 2,142 per machine. [20]

In November, news broke that MissFresh was facing nearly 1,400 lawsuits from former employees and suppliers demanding a total of RMB 813 million. The company had 1,925 employees at the end of 2021, 100 in July 2022 and 55 by the end of 2022. [21]

Why did Dingdong survive and MissFresh perish?

We can see several reasons:

According to industry insiders, the secret of Dingdong's performance was its constant focus on finding inefficiencies and process improvement. [3] Dingdong reduced staff, investments and subsidies and vigorously worked on improving its gross profit margin, which reached 28.7% in Q1 2022, 10% higher than half a year earlier, and improved it to 32.9% at the end of 2022. While Missfresh depended on subsidising consumers for growth, Dingdong was setting up more direct sourcing, self-farming, self-processing and developing semi-processed products and private labels. In 2021, Dingdong’s pre-discount gross margin on private labels was 33.8%, much higher than the 26% on non-private label products. [13]

In 2022, Dingdong closed down loss-making warehouses in 10 cities to reach a positive result. It also reduced the number of warehouses in cities where it remained active. While Shanghai warehouses saw 1,000 orders daily, those in Guangzhou and South China only had 600-800. From its peak in 2021, Dingdong has scaled down from 1,400 warehouses in 37 cities to about 1,000 in early 2023. [13]

Dingdong’s focus on efficiency was probably why Dingdong received new funding in March 2022. While MissFresh desperately searched for new cash, Dingdong received RMB 500 million in immediate funding from the Bank of Shanghai as part of a larger loan package worth up to RMB 8 billion in support. [22]

The Shanghai government picking Dingdong as a preferred grocery supplier during the Shanghai lockdown threw the company another unexpected lifeline. Shanghai contributed 45.8% to Dingdong’s GMV in 2022, exceeding RMB 12 billion. [33]

MissFresh kept pumping resources into new businesses like coffee, vending machines, intelligent fresh markets and retail cloud. MissFresh never optimised its core business … until it was too late.

In Q4 2022, Dingdong’s marketing expenses had dropped 75% YoY. Helped by the disappearance of its primary competitor and COVID lockdowns that persisted in October and November, Dingdong turned profitable in Q4 2022 (non-GAAP). In other words, Dingdong might have survived because MissFresh didn’t.

We’ll return to Dingdong and MissFresh in a moment, but first, let us turn our eyes to the south of China. While these two were battling over cities in the east and north, something had been brewing there...

Pupu Supermarkets

While MissFresh and Dingdong are the most well-known examples of the small front-end warehouse model, Pupu Supermarket (朴朴超市, Pupu Chaoshi) has shown the feasibility of the large warehouse model in second-tier cities. Pupu was founded in 2016 in Fuzhou, Fujian province. It has more than 400 large front-end warehouses in 6 cities. [23] Most have 6,000 orders per day, comparable to a local medium-sized supermarket. [24]

In 2020, Pupu also created Pupu Special Selection (朴朴特选, Pupu Texuan), a selection of low-priced products available in its app, to compete with community group buying platforms. The selection, which was more comprehensive than CGB platforms, included flash sales deals and was available through the same 20-minute delivery as other Pupu products. [25]

Still from Pupu promo clip.

Unlike Dingdong and MissFresh, Pupu Supermarket does not consider itself a pure internet company. It considers itself a retail enterprise. Its staff profile is much more ‘retail’ than ‘internet’. MissFresh and Dingdong first created a large-scale and high GMV before they started optimising to become profitable. That’s a standard internet approach in China. But Pupu did not focus on quickly scaling up and expanding. Instead, it focused on building its supply chain, creating user stickiness and providing good service.

Pupu adopted a model of using large warehouses with more SKUs and low-priced fresh food products to attract traffic. Other products would drive profit. At first, its front-end warehouses were comparable to its competitors’, 300-500 square metres, but they were later enlarged to 800 or even 1,500 square metres. This allowed the number of SKUs to grow from 3,000 to more than 8,000. [23]

A warehouse typically starts with 3,500 SKUs and builds up to 6,000 over a year. Fresh produce accounts for about 40% of GMV, and other food products for about 35%. The rest is non-food, including a lot of mother and baby products. While Dingdong has many more warehouses, these (on average) didn’t have the GMV of a Pupu warehouse. In the areas where the two competed, Pupu was said to have better quality, be more reliable in delivery time and offer more SKUs. With Dingdong, consumers can not fulfil all their needs and have to buy some goods elsewhere.

While larger warehouses allow for more SKUs, the higher costs limit the speed of expansion to other cities. It took Pupu 3 years to get a foothold in Fuzhou before expanding to the Pearl River Delta (Shenzhen and Guangzhou). Further expansion to Wuhan, Chengdu and Foshan followed in 2021. Only Fuzhou, Xiamen and Chengdu have city-wide delivery. [23] Currently, Fujian and South China account for 40% of Pupu’s sales, with the remaining 20% of sales contributed by the Wuhan and Chengdu markets. [26] Pupu reached a high penetration of 70% in Fuzhou but had to do so by investing heavily in consumer subsidies. Its prices were often lower than those in offline supermarkets. [23]

Image taken from the Pupu website.

When Pupu expanded and grew, it could no longer rely on the staff it had cultivated in the organisation and needed to attract outsiders. According to a Pupu manager, its HR was inexperienced, unprofessional and arrogant and, as a result, had difficulties recruiting quality employees, mostly taking fresh graduates. A lot of workload remained with the older employees, who therefore did not have time to train the rookies, who consequently didn’t learn fast enough. Mid-level staff needed to be trained at headquarters for three months, seriously slowing down Pupu’s development.

In a city like Shenzhen, Pupu would need about 3,000 orders per warehouse per day to break even. But labour costs would be much higher than in Fuzhou and Xiamen because salaries are about 1.5 times higher in Shenzhen, resulting in a higher break-even point.

After launching in a new city, Pupu will gradually replace local products with centrally sourced products. Initially, local products will have a higher share because the supply chain has not developed fully. But after about 2.5 years, 60% can usually be sourced centrally.

Pupu cooperates with suppliers to provide better quality products, for instance, by working with meat suppliers to improve technology for controlled temperature meat packaging. This will improve shelf life, quality and customer satisfaction.

In July 2023, Pupu had 1.1 million daily orders, while Dingdong had about 1 million. Pupu might well be the reason it was so difficult for Dingdong to get a foothold in South China. [13] According to insiders, people's spending power in Shanghai, Dingdong's most successful market, is higher than in South China. The main competition in that region will be between Pupu and Meituan Maicai, Meituan's front-end warehouse operation. In its home province, Fujian, Pupu faces competition from Yonghui, which also operates front-end warehouses there (see below). Fuzhou is also the headquarters of Yonghui. [26]

While the company as a whole is not yet profitable, Pupu claims 70% of its warehouses already show positive results, and it will reach full profitability in 2023. It will be opening new warehouses more conservatively, with 50-80 new ones planned in Chengdu and Wuhan. Pupu avoids competition and opens warehouses where others don’t yet operate. [27]

In July, Pupu was said to be planning to open 70 more locations on top of the 30 it had opened in the first half of 2023. [23] Like Dingdong, Pupu has been reducing costs and improving efficiency in 2022, raising its gross profit margin from 16% to 22%, and costs have dropped by 4-5% since last year. GMV at the end of 2022 was RMB 22 billion. These improvements were mainly the result of direct sourcing and other optimizations in the supply chain. Pupu expects to optimise further and reach a gross profit margin of 25%. Considering that Dingdong's gross profit margin reached 32.9% in Q4 2022 and was barely profitable (non-GAAP), Pupu still seems to have a long way to go. [23] But then again, Pupu has more SKUs, a higher AOV and potentially a better net profit per order.

Further expansion would require a lot of extra capital. Pupu has seen five funding rounds until November 2021 but has not received further private funding since. Allegedly, Pupu has been preparing for an IPO for a while. There might be few takers considering MissFresh's fate and how Pupu has never been profitable in the seven years since its founding. [23]

Others using front-end warehouses

MissFresh, Dingdong and Pupu are not the only ones using front-end warehouses. Let’s briefly look at some other well-known names that use, or have used, the approach for part of their business.

Sam’s Club

In 2016, Walmart invested in JD and both invested in JD Daojia, part of Dada Nexus, which we have described in the previous Need for Speed article. Walmart’s Sam’s Club opened a flagship store on JD.com and put some of its products in JD’s self-operated warehouses.

In 2017, while MissFresh and Dingdong began opening front-end warehouses around the country, Sam’s Club faced challenges because of slow expansion, and it wanted to increase the frequency of user purchases. It began testing the front-end warehouse model in Shenzhen. [28] By now, the retailer has nearly 500 front-end warehouses across China. Each measures 500-800 square metres and requires RMB 300,000 - 500,000 investments. They see average consumer orders of RMB 200. [28]

Dada’s courier services, also part of Dada Nexus, provides delivery from these warehouses. In the urban areas of many cities, Sam’s Club has been able to achieve 1-hour delivery. [29] Dada delivers 2 million orders daily, nearly 400,000 of which come from Sam’s Club. In 2022, the growth rate of Sam’s e-commerce deliveries was 300%, with half of the daily orders being delivered from front-end warehouses. Competitor Costco only offers next-day delivery. [29]

According to recent figures, 55% of Sam’s Club’s sales now come from online channels, part of which are delivered from its front-end warehouses. [28]

JD.COM

JD.com recently established an Innovative Retail Department. One of the department's projects concerns an attempt at front-end warehouses. Some think that trying out this model is JD's defence strategy against the expansion of Meituan in this field, as well as the potential erosion of its market share by front-end warehouse operators. [30]

By July, JD had already started two self-operated front-end warehouses in Beijing, and six more were under construction. JD places high-volume, fast-turnover products in these warehouses so it can deliver them in 2 hours instead of the usual next or same-day service levels. But if it wants to match Meituan’s and Dingdong’s delivery speed, it will need more warehouses with a smaller distance to customers. This would require serious investments. [31]

Meanwhile, JD has also set up the Jingdong Maicai platform. In essence, this is an aggregation marketplace where its own affiliated retailers like 7Fresh and Yonghui plus third parties like Pagoda (百果园), Wumart (物美), Dingdong Maicai, Carrefour and even Hema can offer products to consumers. [32]

Yonghui

According to April 2023 data, Yonghui has launched 966 e-commerce warehouses across the country, including 156 ‘online full warehouses’ (线上全仓, which cover 22 cities), 161 ‘high-standard half warehouses’ (高标半仓, covering 44 cities) and 22 ‘satellite warehouses’ (卫星仓) plus 627 store warehouses (店仓, covering 150 cities). Some of these warehouses are front-end warehouses, although the different naming makes it hard to determine how many.

In five cities, Yonghui has achieved prominent city centre coverage through 160 warehouses: Fuzhou, Beijing, Chengdu, Chongqing and Hefei. [26]

According to industry insiders, Yonghui has been plagued by staff shortages. As soon as it started getting many orders, its staff could not keep up, and complaints would skyrocket.

Hema Small Stations

In 2019, Alibaba’s Hema (Freshippo) also tried the front-end warehouse model. It had 80 so-called ‘small stations’ (盒马小站) in 5 cities. [3] Hema Small Stations were located in areas where Hema was unable or unwilling to establish a full-fledged store. They would mainly serve as a front-end warehouse and only offer delivery. As such, they were comparable to Ding Dong Maicai, Meituan Maicai and MissFresh.

The concept wasn’t a success, and Small Stations were abandoned in March 2020, with some locations being upgraded to Hema Mini stores. Regarding the front-end warehouse model, Hema founder Hou Yi later said: "I also use Dingdong to buy vegetables and I study them.” He found three problems with the model: [3]

The consumer price cannot be increased. People cook for themselves so the price cannot be too high. There is also no offline store like Hema to improve AOV with catering offerings.

The loss rate cannot be reduced. Most customers place an order just before dinner time. If there is too much stock in the warehouse, the loss rate after 18:00 hours will be enormous. If there is too little stock, there will be huge out-of-stocks before 18:00 hours, and customers won't be retained.

Gross profit margins are too low. The goods sold through e-commerce are the same as in vegetable markets, and persuading customers to pay significantly higher prices is impossible.

Still from Dingdong promo clip

Can the front-end warehouse model be profitable?

Let's see if Hou Yi was right …

Many investors consider the combination of high-cost door-to-door service and low-cost grocery shopping a value mismatch. [8] In 2022, LatePost made the following estimation for the situation in Beijing: [3]

Average order value: RMB 85

x Average daily order value per warehouse: 700 on weekdays and 1,000 in the weekend

= RMB 1.989 million monthly income

Monthly costs are:

Webmaster: RMB 12,000

Warehouse management: 6 x RMB 6,000

Couriers: 20 x RMB 9,000

Water, electricity, sanitation: RMB 18,000

Costs of goods: RMB 1.744 million (87.72% according to MissFresh's data for Q3 2021)

Result: RMB 25,700 loss per warehouse per month. This does not yet take into account loss of goods and consumer subsidies.

Despite the calculations above and the demise of MissFresh, the profitability of Dingdong seems to point towards possible sustainability of the model, as long as gross profit margins and orders per warehouse are high enough and costs can be kept under control.

A MissFresh executive told LatePost they needed a 30-35% gross margin to break even. Their margin was less than 12% in 2021. Meanwhile,

Haitong Securities calculated in 2019 that Dingdong would only reach the break-even point at 1,250 orders per warehouse per day (based on 3 RMB rent per square metre for a 300 square metre warehouse, an average order value of 50 RMB, 30% profit margin and 30 warehouse workers). [37] Dingdong itself said the model needs 1,000 orders per warehouse, an average order of at least RMB 65 and a gross profit margin of 30%. [13]

The biggest challenge to the front-end warehouse model are the operational costs of the city warehouses (that supply the front-end warehouses), the front-end warehouses and the delivery costs from the city to the front-end warehouses and from there to the customer. From 2020 to 2021, Dingdong’s ratio of operational expenses remained stable at 35% of revenue. From 2018 to 2020, MissFresh’s ratios dropped from 35% to 26%, and Dingdong could control it down to 25.25% by the end of 2022. [13]

But, as we’ve shown, there have been too many factors at play to conclude that Dingdong has proven the front-end warehouse model to be sustainable. Could it maintain its results with its remaining warehouses now that the pandemic has ended?

Some industry insiders claim that food e-commerce, especially front-end warehouses, has been enormously impacted by the end of the pandemic. Consumers no longer need immediate delivery and are no longer willing to pay delivery costs and premium prices. Many have returned to wet markets and supermarkets for their groceries.

Dingdong increased its prices in Q4 2021 and screened for high-quality users who don’t constantly use discounts. Many products are now more expensive than in alternative channels, and Dingdong has lost price-sensitive customers. While Dingdong can optimise its gross margin and AOV, can it maintain its number of orders? [13] At the end of 2022, the daily orders at Dingdong had already dropped from one million to 800-900K. Beijing dropped from 1,000-1,200 during the pandemic to 800-1,000 in Q4 2022, and some warehouses didn't even reach that level and were stuck at 800 daily orders. [13]

Finally, some industry insiders believe that Pupu's large warehouse model, with more SKUs is the way forward for the front-end warehouse business. [26] But even more so than Dingdong, Pupu still needs to prove its approach is profitable.

Not for lower-tier cities

The front-end warehouse model concentrates on first- and second-tier cities with high population density and high disposable income. [8]

MissFresh only built warehouses in first- and second-tier cities with enough potential among high-income customers. It had determined about 50 cities where its business could be sustainable, and by the end of 2021, it was active in 21. Meanwhile, Dingdong would expand its geographical coverage from metropolises to surrounding lower-tier cities. It was active in 37 cities in 2021, including 11 third- and fourth-cities. [5]

Despite its activity in lower-tier cities, Dingdong has calculated that a front-end warehouse in a third-tier city needs at least 700 orders per day and an average order value of RMB 60 to be profitable. It concluded that first-tier cities could do front-end warehouses, some in second-tier cities would be barely profitable, and those in lower-tier cities would fail. [8] Still, Dingdong gave third-tier cities another try by finding the 30-40% of the population in those cities it considered its target audience.

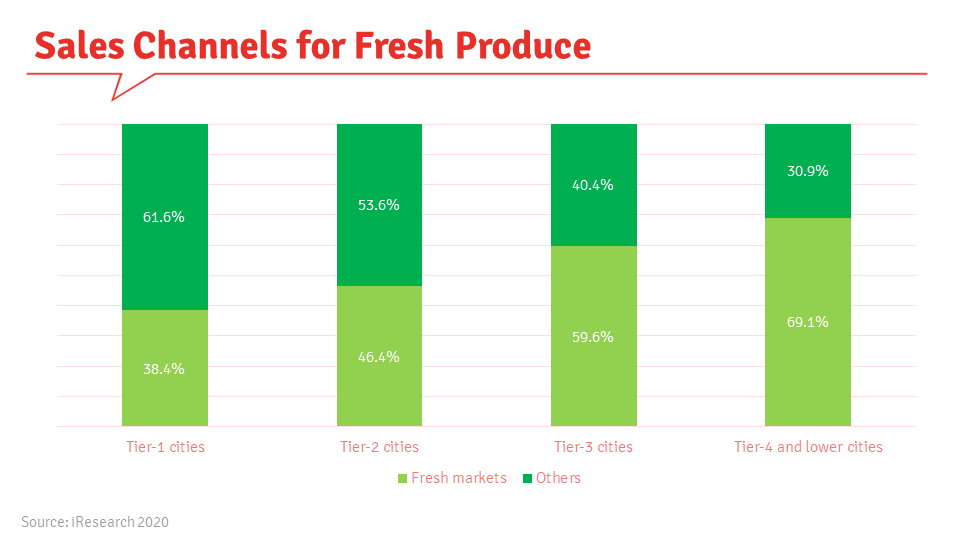

Fresh food e-commerce as a whole is expected to survive in first- and some second-tier cities with solid GDP per capita or consumption power. In third-tier cities and below, it is hard to maintain the model due to insufficient consumer demand and spending power. In such cities, where people also shop more in traditional channels like fresh markets (see graph below), revenue will not be able to support the high costs of front-end warehouses, distribution and spoilage. Therefore, there is a ceiling to the model's growth as it can only work in a few dozen cities.

Some experts think that, as with other retail formats like hypermarkets, the front-end warehouse will eventually make it to the third- and fourth-tier cities. [26] Considering the learnings of Dingdong and MissFresh, the time might not be right yet.

Dingdong in 2023

Now that Dingdong has become profitable in Q4 2022, all eyes are on this year’s results for the company. If it could maintain its profitability post-pandemic, it could prove the sustainability of the front-end warehouse model. These were the results in the first two quarters of 2023:

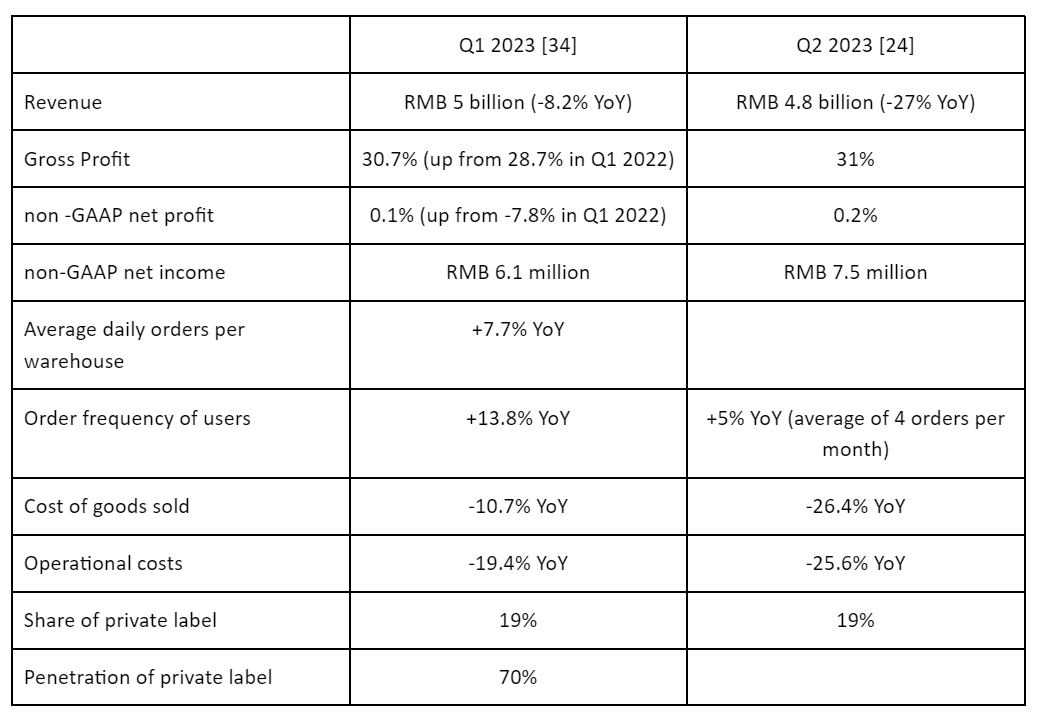

Dingdong kept growing its private label offerings. In Q1 2023, private labels of pre-made dishes made up 19% of Dingdong’s GMV and the user penetration had increased to 70%. [35]

In Q2 2023, Dingdong claimed to have reduced the loss rate to 0.5%. [24]

Dingdong has a membership program. For RMB 88 per year, members get benefits such as free dishes, exclusive products and discounts, and ‘super member days’. The program is designed to increase order value and frequency. In Q2 2023, its members accounted for 54% of GMV, up 10% from a year earlier, while member orders increased 9%. [19]

Q2 2023 was Dingdong’s third profitable quarter based on non-Gaap standards. Cost reductions seemed to be the primary reason: compared to Q2 2022, operational costs were almost 26% lower in the same quarter in 2023. Costs of goods decreased by 26.4%, and Dingdong’s direct sourcing ratio now stood at 80%. User retention increased: frequency of monthly orders grew by 5% YoY to 4 orders. ARPU increased by 8% YoY. According to Dingdong, sales and marketing expenses decreased by 39% because the strong brand image allowed lower customer acquisition costs. [24] But we’re pretty sure the absence of last year’s competitor also played a role …

Year-on-year, Dingdong saw 8% lower revenue in Q1 and 27% lower revenue in Q2. It attributed this to the exceptionally high volumes during the pandemic, especially during last year’s lockdown in Shanghai in Q2. It also pointed to more people travelling during Spring Festival and Dragon Boat Festival this year, resulting in fewer orders than in 2022. Finally, Dingdong pulled out of several cities in Q2 2022, resulting in lower revenue but better profitability. But compared to Q2 2021, Dingdong’s revenue only increased 4%. [19]

Dingdong’s retreat from loss-making regions continued. In May 2023, it pulled out of Chengdu and Chongqing. ‘Temporarily’ according to the company. In Chengdu, Dingdong faced competition from Pupu, which offered lower prices. After this retraction, it still operated in 25 cities. [39]

By early 2023, Dingdong’s delivery staff could handle 70 daily orders, higher than the 40 food delivery couriers. However, the user experience was in danger of being hurt because it could result in a higher overall delivery time since couriers take more orders per ride. While Dingdong used to advertise ‘delivery in 29 minutes’ (one minute faster than MissFresh), it actually took 50 minutes or more in 2022. [13]

Meanwhile, Dingdong's Beijing delivery drivers have lost income. During the pandemic, they could deliver 108 daily orders and 2,800 a month, earning about RMB 10,000. Now, they make RMB 3,000 plus 3 RMB per order, with about 60 orders daily. While still working 13 hours a day and 26 days a month, their average income has dropped by about 25%. [13]

While there is a positive way of looking at the Q2 2023 results, Dingdong’s share price fell to its all-time low of $1.90 after its release. [19]

Dingdong might have more up its sleeve though. It has moved from only offering fresh produce to adding other food products, competing with online supermarkets like JD Supermarket and Tmall Supermarket. It wants to become a new-generation food company and is considering becoming a ‘brand owner’ and making its private labels available to others in the future. [32]

Dingdong has created a methodology for product development based on three main points: [9]

Capture consumption trends early through user research (e.g. the establishment of pre-fabricated dishes in 2020). Its research consists of trend analysis (e.g. the need for healthier food) and real-time customer feedback.

They wish to become a food R&D company and find suitable suppliers.

Maximizing the platform's potential, e.g. through strategic cooperation with suppliers on production, supply, sales and product branding.

In other words, Dingdong also wants to become a B2B food supply chain company (to third parties) and increase investments in supply chain, food R&D and processing accordingly. [27]

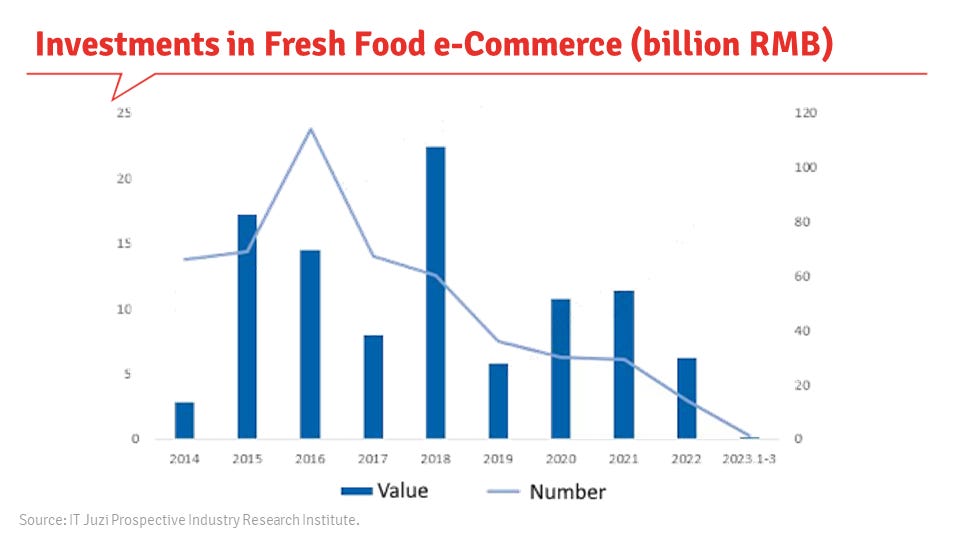

With investments into fresh food e-commerce having dried up (see graph below), Dingdong would have to show it could continue to hold up its own pants.

Graph source [23]

Front-end warehouses versus alternatives

The jury is still out on the future of the stand-alone front-end warehouses as a model for fresh food and grocery delivery. While the front-end warehouse model struggles with sustainable profitability, other (instant retail) propositions can also deliver fast and fresh (e.g. Hema, JD Daojia, Ele.me). [27] These alternatives seem more sustainable; Hema and Dada Nexus have become profitable this year.

Front-end warehouses are also a more expensive option for consumers. In May 2021, a report by Soochow Securities comparing community group buying, traditional supermarkets and front-end warehouses found that the latter category had prices at 121%-136% of those at regular supermarkets. [3]

The operational costs of the front-end warehouse model are about RMB 10-13 per order, higher than in traditional retail, community group buying and marketplace-based instant retail. At Dingdong, these costs are about 24% of the sales price and at Pupu 20%. [27]

According to a writer at 36Kr [17], the operational costs of a front-end warehouse are two times that of platform e-commerce (we assume he meant marketplace instant retail like JD Daojia here), three times that of central warehouse e-commerce (we assume he meant webshops like Tmall Supermarket and JD Supermarket) and six times that of community group buying.

On a more positive note, compared to the shrinking market of offline supermarkets, companies can achieve 50% YoY growth in the front-end warehouse market. [30] And compared to a Hema supermarket, the initial investment in a front-end warehouse is relatively low, e.g. RMB 500,000 for a 300 square metre warehouse. A Hema Fresh store of 3,000 - 5,000 square metres can come with an initial investment as high as RMB 30 million and costs RMB 600,000 to 1 million in monthly rent alone. [17]

Dingdong is profitable, but only with a tiny non-GAAP margin. It has cut costs and improved efficiency but at the expense of pressure on staff and possible damage to customer experiences. Dingdong's thin margins would quickly evaporate if another subsidy war with any other grocery delivery competitor broke out again. Meanwhile, Pupu, which is trying a slightly different model with larger warehouses, is not profitable yet.

Front-end warehouses are also a model that can’t be scaled up very fast and, in most cases, doesn’t have its own online customer acquisition channel. Alternatives like Hema, 7Fresh, JD Daojia and Meituan Shangou can tap into their parent company's main apps and ecosystems.

Shanghai accounted for RMB 12 billion, almost half of Dingdong’s GMV. For Pupu, its home base of Fuzhou, accounted for RMB 7.7 billion. It also used to be half of its GMV, but the share has decreased with the growth in other cities. [27] These two companies are expected to maintain their regional dominance (Pupu in Fujian and Guangdong, Dingdong in Shanghai and Zhejiang). Improving the density of warehouses in their core regions and avoiding large-scale cross-regional operations will be key to reaching or maintaining frail profitability. After all, reaching break-even in a new city can take 2-3 years. [27]

Others like Sam’s Club, Hema, Yonghui and Meituan Maicai are expected to operate nationally. The strength of players like Meituan Maicai might depend on how well their apps (e.g. meal delivery) perform in a specific region. [26]

One of the limitations of the front-end warehouse compared to other instant retail models is that the SKUs are limited, and other forms can provide a much wider range of products and services. A consumer who wants to cook one day and order takeaway the next might be more inclined to use the Meituan app.

According to Pupu’s research, the proportion of China’s population born after 1995 has reached 17.5%, and half are willing to pay for instant retail. The question remains: which form of instant retail?

Source: [23]

And what became of MissFresh?

In May 2023, some shareholding MissFresh employees were invited to sell their stock. The company’s market value had dropped from $3.5 billion at its IPO to $4.83 million. Suppliers sued, and courts ruled against MissFresh, but since most of their warehouses were leased, there were few fixed assets to enforce. [38]

On June 13th 2023, MissFresh received a notice to delist from Nasdaq, two years after its IPO. Its share price had fallen below $1 for 30 days.

In August 2023, MissFresh finally released its 2022 financial report. Its revenue had plunged to RMB 2.8 billion, while losses narrowed to RMB 1.52 million. But none of that really mattered anymore because the company had, in essence, already shut down in July. MissFresh only held RMB 48.96 million in cash (equivalents), and its total liabilities were more than nine times its assets. [19]

That same month, MissFresh was back in the news. It had sold 88.1% of its outstanding shares for $27 million to two investors, valuing the company at $30 million, far above its market capitalization of $4 million before the deal. Voting rights of all shares were given to Xu Zheng, MissFresh’s CEO, who had taken over the shell of the company. The investment avoided the looming delisting of MissFresh.

At the same time, MissFresh bought a company called Mejoy Infinite Limited for $12 million. It plans to provide digital marketing services through this unknown Hong Kong company and ‘revolutionise the neighbourhood retail business’. [15]

Anybody interested in these services?

Key Takeaways

Cases show that the sustainability of the front-end warehouse model is still unproven. It depends highly on keeping the high operational costs under control, optimising the supply chain (e.g. by direct sourcing and self-processing) and reaching a high profit margin (e.g. through pre-fabricated food and private labels).

MissFresh perished because it could not improve its profitability in time and had invested resources in non-core-business initiatives that might have looked good in the IPO prospectus but failed to deliver in time. MissFresh could not get timely new funding.

Unlike MissFresh, Dingdong seems to have found the right strategic combination and has reached non-GAAP profitability in Q4 2022. But even for them, it remains questionable if the model can maintain the momentum it got during the pandemic. They survived with extra bank funding in 2022 and preferential government treatment during the Shanghai lockdowns.

While MissFresh and Dingdong have tried, the front-end warehouse does not seem to work in the ‘sinking market’ (tier-3 cities and below). A combination of too few orders per warehouse per day and lower AOV than in the big cities will prevent the model from being profitable. This also means that there currently is a ceiling to the business of front-end warehouses.

The leading players (Meituan Maicai, Pupu Supermarket and Dingdong) are strong in their own regions. Moving into the home bases of their competitors could mean new subsidy wars that would destroy the thin margins or make losses balloon further.

Pupu Supermarkets stands out because it uses larger warehouses that can deliver more SKUs. It has not been fully profitable yet, and challenges with recruiting and training staff have put the break on its regional expansion.

While pure players like Dingdong struggle with profitability, established retailers like Sam’s Club have also deployed front-end warehouses to grow their online business. JD.com is also experimenting with the model.

Despite its downsides, the front-end business model does have a relatively unique proposition with the high quality of its fresh produce, owning to short supply chains and direct sourcing. Still, consumers will pay a higher price for this superior quality and convenience.

Sources

Six Degrees Intelligence, a leading global expert network/quantitative research firm that operates in China. Augmented with information from the articles below:

[1] Seeking Alpha, 2021-10-12 [2] GGV 2020-05-28 [3] LatePost 2022-08-05 [4] EqualOcean 2019-02-22 [5] Seekingalpha 2021-10-12 [6] SMCP 2021-04-08 [7] Kr-Asia 2021-04-44 [8] LatePost 2022-04-18 [9] 第三只眼看零售 2023-02-24 [10] Pandaily 2021-04-07 [11] The Bamboo Works 2021-07-08 [12] Jiemian 2021-08-02 [13] TechPlanet 2023-03-02 [14] 金角财经 2023-07-11 [15] The Bamboo Works 2022-01-28 [16] Pandaily 2022-01-28 [17] 36Kr 2022-08-16 [18] Caixin 2022-07-09 [19] The Bamboo Works 2023-09-05 [20] Pandaily 2022-08-23 [21] Caixin 2022-11-16 [22] The Bamboo Works 2022-08-15 [23] 零售商业财经 2023-07-13 [24] 第三只眼看零售 2023-09-01 [25] 第三只眼看零售 2020-11-23 [26] 第三只眼看零售 2023-07-03 [27] 第三只眼看零售 2023-05-24 [28] Linkshop 2023-08-24 [29] LatePost 2023-09-04 [30] 商业观察家 2023-07-02 [31] LatePost 2023-07-27 [32] Linkshop 2023-03-07 [33] Technode 2023-02-14 [34] 第三只眼看零售 2023-05-12 [35] 零售圈 2023-08-05 [36] Pandaily 2022-06-06 [37] Technode 2020-04-02 [38] Latepost 2023-06-14 [39] 新消费日报 2023-05-23 [40] 商业迷 2023-07-16

We would especially like to mention Latepost’s excellent longreads 每日优鲜,多出来的三年 and 叮咚买菜:不能踏进同一条河流 that have been enormously helpful when writing this article.

All visuals by ChinaTalk.nl unless stated otherwise. These visuals may not be used or reproduced without the prior consent of ChinaTalk.nl.