Need for Speed 3: Coming soon, from a Meituan warehouse near you!

About 'front-end warehouses' and 'lightning warehouses'

Things that caught our attention

Things that caught our attention

Tech Buzz China founder Rui Ma has made her TV debut in an episode of the documentary series NOVA called ‘Inside China’s Tech Boom’. You can watch the episode here. Rui and Kaiser Kuo (of Sinica podcast fame) will host a screening and panel discussion on Tuesday, November 14th, from 6:30-8:00 PM in New York City, organised by the AsiaSociety. Tickets can be bought here.

In 2018, Alibaba opened an experimental shopping mall called Qinchengli next to its Xixi campus. Chinese media outlet Lianshang recently wrote about the disappointing status quo of the mall. Tech Buzz China writer Ed Sander, who has visited the mall many times with his study tours, summarized the article and added his own thoughts in a LinkedIn post.

Latepost recently published interesting new figures on Temu, Pinduoduo’s cross-border e-commerce platform. Ed summarized them in a LinkedIn post. (source) You can read more on Temu in one of our most popular articles of 2023 so far, Temu: from $0 to $3 billion in 10 months.

The Wire China published an article on Cotti Coffee (paywalled). Tech Buzz China provided information and opinions about Cotti for this publication, based on our recent deep-dive Coffee Wars: How the arrival of Cotti has sparked a price war.

E-commerce on Douyin is hitting new highs with a staggering nearly 2 trillion yuan GMV from Jan-Oct this year, soaring close to a 60% year-on-year increase. (Source)

Chinese EV makers are revving up for a blockbuster 2024! Exclusive scoop from 36Kr: Li Auto's forecast to zoom past 800,000 units, doubling their 2023 sales. NIO's gearing up for a 230,000+ finish line, while XPeng targets 280,000+ (not incl. sub-brands like Alps & MONA). (Source)

Earlier this year we wrote about Douyin’s food delivery initiatives in Food Fight! Douyin’s local services business. Douyin’s main competitor, Kuaishou, has now also started to offer home delivery with some group-buying deals of KFC, Haidilao and other restaurants. As with Douyin’s earliest moves into food delivery, the merchant arranges delivery for orders he received through Kuaishou. (Source)

Introduction

We have taken two deep-dives into China’s bustling instant-retail market in the past months. First, in Need for Speed: Instant Retail, we looked at the marketplace platform model operated by the likes of JD Daojia, Meituan Shangou (Flash Shopping) and Alibaba’s Taoxianda. Later, in Need for Speed 2: Can the front-end warehouse model ever be profitable?, we looked at the model operated by MissFresh, Dingdong and Pupu Supermarket.

In both articles, we skipped over two related aspects: the front-end warehouse business of Meituan Maicai and the Meituan Shangou-related operating model of ‘lightning warehouses’. In this article, we will return to the instant retail market once more to explain how Meituan delivers goods from different types of warehouses hidden within residential areas.

We suggest reading the previous two articles if you are unfamiliar with the business models of front-end warehouse and instant retail marketplaces.

Freya Zhang, Ed Sander & Rui Ma

(click on the images above for information on the Tech Buzz China team)

Meituan Maicai

An Ella supermarket in Beijing, early 2019.

In 2019, Meituan closed its failed Ella (小象, Xiao Xiang, literally ‘Little Elephant’) supermarket business, which had been an attempt to copy Alibaba’s Hema. The concept was replaced with initiatives in community group buying, Meituan Select (Meituan Youxuan, 美团优选), and the front-end warehouse model, Meituan Grocery (Meituan Maicai, 美团买菜). The latter continued to use Ella’s elephant logo, albeit with a green instead of brown colour. Later, Meituan hired some retail experts to build the business.

Meituan Maicai (‘Meituan Grocery’) is an app separate from Meituan's main app and was launched in January 2019 with around 1,500 SKUs. Meituan Maicai opened front-end warehouses in the first-tier cities (Beijing, Shanghai, Guangzhou and Shenzhen) as well as in Foshan, Dongguan (both close to Guangzhou), Langfang (between Beijing and Tianjin) and Wuhan. It later closed down Meituan Maicai in Wuhan and Dongguan. It replaced it with Meituan Select. [2] After the demise of MissFresh (see Need for Speed 2), Meituan Maicai is the third largest player in the front-end warehouse market after Dingdong Maicai and Pupu Supermarkets. Meituan sales volume is about 60% of Dingdong’s, while Pupu’s volume is close to Dingdong’s.

Meituan Maicai delivers goods within a radius of 3 kilometres from its warehouses and has no guaranteed delivery time. However, like others, the app promises delivery within 'as short as 30 minutes'. Above 29 RMB, Meituan Maicai delivers the goods for free; below that amount, they charge 3 RMB.

Most front-end warehouse companies initially focussed on high-frequency fresh products. Meituan and Pupu have gone beyond fresh food (30% of their assortment) and added other food products to increase their average order value. Reducing the share of fresh produce means lower loss rates (spillage and spoilage) and a potentially higher gross margin of the product mix. Unlike its competitors, Dingdong Maicai tends to stick to the fresh food category (50-60%), hoping to bind customers with its wider variety of fresh food. [1]

Compared to its competitors, Meituan Maicai followed a different growth strategy, limiting geographical expansion, focusing on the first-tier cities, and not investing upstream into the supply chain. Instead, it cooperated with large, high-quality distributors. [2] In November 2021, Meituan Maicai added live seafood to their assortment. [6] Unlike some of its competitors, Meituan Maicai never rushed into the sinking market but stuck to the four first-tier cities and their surrounding areas.

As we have seen in Need for Speed 2: Can the front-end warehouse model ever be profitable?, the front-end warehouse model can survive in first and some second-tier cities because consumers have the required spending power of RMB 65-80. In lower-tier cities, insufficient consumer demand, purchasing power and order sizes cannot support the costs of front-end warehouses, distribution and product loss. As such, the front-end warehouse model can only cover a few dozen cities at most. Therefore, The reserved strategy of Meituan Maicai seems to have been a wise one. [8]

In 2021, seeing the changing consumer habits due to the pandemic, Meituan increased the number of front-end warehouses from 200 to more than 400. In September 2021, Meituan upgraded its ‘food + platform’ strategy to ‘retail + technology’, stressing its entrance into the physical e-commerce market. It aimed to use technological means and basic retail skills to improve efficiency to meet consumer’s need for convenient shopping. [5] A month later, three business units, Meituan Maicai, Meituan Select and B2B food distribution division Kuailü, were integrated into a special retail group managed by five core managers of the company. [8]

Meituan Maicai app.

In early 2022, Meituan began cost reductions and efficiency improvements in its retail business. When Meituan was reported to start job cuts to lower costs in April 2022, Meituan Select (Community Group Buying), Meituan Maicai, and Kuailü (‘Fast Donkey’) faced the deepest cuts of up to 20%. [7]

Some of its 400 front-end warehouses showed poor sales and unit economics. Meituan closed warehouses with low square meter efficiency and spent the year reducing loss of goods, optimising assortment and controlling labour costs. [1]

In the first three quarters of 2022, the impact of the pandemic in Beijing, Shanghai, Guangzhou and Shenzen led to a decline in GMV, while order volume increased again in the fourth quarter. That year, gross profit margins were acceptable, exceeding 20% (but remember that Dindong needed more than 30% to become profitable). Meituan, like Dingdong, has also launched private labels.

In the first quarter of 2023, Meituan Maicai’s transaction volume increased 50% year-on-year [4] and was said to have reached a positive operating result. In 2023, Meituan Maicai claimed its turnover speed had tripled, and warehouse costs were reduced by 60%. [5] In early 2023, Meituan’s average order value had reached RMB 50.

Meituan Maicai started a new round of expansions in East China, (re)entering Suzhou. Having lowered costs and improved efficiency, Meituan seemed no longer reluctant to enter a more competitive market where Dingdong had a strong presence. In the first quarter of 2023, Meituan had 500 front-end warehouses and 1.1 million daily orders. [1]

Meituan uses big data of its 678 million transacting customers (2022) to drive the company's decision-making and to determine its product assortment. To ensure 30-minute delivery, Meituan regulates manpower by analyzing real-time conditions like weather, the impact of marketing activities, etc.

Outside a Meituan Maicai front-end warehouse, Beijing, July 2023.

(Note: the section below is only available to paid Tech Buzz China subscribers)

Organisation

Meituan is organised around the scenarios of eating at home or eating out. Eating at home can be done by cooking, using ingredients home delivered by Meituan Maicai or Meituan Select, or by food delivery (Meituan Waimai).

Under the Ella organisation, products were selected by the Merchandise Department. Some of these were private labels, including the Xiang Da Chu (象大厨, ‘Elephant Chef’). This private label started with some cooked foods and branched into frozen products. Under Meitian Maicai the private label share is 20-30%.

Meituan’s failed Ella supermarket, Beijing 2019.

After purchasing, goods are shipped to a Meituan distribution centre (DC), where some products are processed and packaged as private label brands. Standard products don’t get secondary packaging. Shanghai used to have one DC, but later, it was split into two separate DCs in different locations: one cooled warehouse for fresh produce and one with regular temperature.

The monthly costs of a central warehouse (DC) of Meituan Maicai break down as follows:

Rent: RMB 600,000

Personnel: RMB 560,000

Utilities: RMB 230,000

The monthly transportation costs to 120 front-end warehouses in Shanghai add up to RMB 2.16 million.

Goods are distributed from the DCs to front-end warehouses equipped with cold and frozen storage. Each front-end warehouse has three departments responsible for warehouse management, distribution (delivery) and customer acquisition. Front-end warehouses service consumers in a 3 km radius.

Although Meituan Maicai and Meituan Select (community group-buying) are entirely independent business units, they do share resources like the advertising resources of Meituan’s power bank division. Meituan does, however, not share drivers between Meitian Waimai (food delivery) and Meituan Maicai, and both use different clothing and boxes (black-yellow versus green), with Maicai’s boxes being much larger, so they can fit orders for up to 6 households in one trip.

Inside a Meituan Maicai front-end warehouse, Beijing, July 2023.

Meituan Maicai’s business hours are 6:00 to 23:00, but order volume peaks between 16:00 and 20:00 hours, accounting for 30%-40% of a working day’s order volume. 10:00 to 12:00 sees another peak. Couriers deliver 40-60 orders daily, with an average one-way riding time of 20 minutes and 3 - 7 orders per trip, increasing to 6-7 orders per trip during peak hours. The average delivery distance per order is 3.6 km.

The overall loss rate at Meituan Maicai is 3.5%, of which 60% is expiry date loss and 40% breakage loss. The loss of fresh food is 1.9% and seafood 3-4%.

Upgrading warehouses

The small 200 square meters warehouses Meituan Maicai started in 2019 have basically all been closed; they couldn’t generate enough volume. Meituan’s second generation of front-end warehouses, measuring 300-500 square meters, could hold 3,000 SKUs and generate 800 - 1,200 orders daily. [1] These warehouses have reached break-even.

Meituan typically signs warehouse contracts for 1-2 years and is now replacing all first and second-generation warehouses, with about 20% remaining at the start of 2023. The recently opened third-generation warehouses are larger at 600-800 square meters (6,000 SKUs). Meituan is no longer opening new locations smaller than that. While there is no upper limit, new warehouses are usually not larger than 1,000 square meters. Large warehouses can have 3,000 daily orders; some in Beijing and Shanghai even reach 5,000-6,000. Large front-end warehouses, like the ones Pupu Supermarkets uses and those that Meituan Maicai has shifted towards, are considered the most efficient and lowest-cost approach. [4]

In 2023, Meituan Maicai was still in the process of selecting the right products, and consumers still associated the platform with fresh products in a narrow sense, such as fruits, vegetables and meat. [4]

But even third-generation warehouses might close when it is found that they could move to a better location. At the start of 2023, most warehouses saw 1,500-1,600 orders, about 100-200 orders below Dingdong’s warehouses. At 1,600 orders, warehouses break even. They need to reach about 30,000 households to do so.

Some individual warehouses might break even at a slightly lower volume if they have lower costs (e.g. rent). But if a warehouse still has less than 1,000 orders, it will be closed or replaced.

A former Meituan Maicai front-end warehouse, Beijing July 2023.

The first Suzhou warehouse was about 600 square meters large. In 2022, Meituan shut down Suzhou’s operation because of the pandemic and lack of profitability. Meituan had also learned that Dingdong’s operation in Suzhou wasn’t profitable.

Currently, Suzhou’s relaunched operation is supported by the Shanghai distribution centres (DCs) since Shanghai is close to Suzhou. Meituan plans to open six front-end warehouses in Suzhou and expand to surrounding areas later. The Suzhou operation is expected to be profitable within a year. Based on the required 30,000 households per warehouse, Suzhou is not expected to exceed 20 front-end warehouses.

Meituan follows a very data-driven approach in its expansion of warehouses. From 2019 to 2022, Meituan only opened a little over 100 warehouses in Shanghai and maybe a few more in Beijing and Shenzhen. Beijing and Shenzhen have 13-14 districts, each with 10-12 warehouses. Shanghai has ten districts and less than 120 warehouses. With all the competition in the sector of front-end warehouses, it’s now getting harder to find places to open them.

Post-pandemic

In 2019, before the pandemic, Meituan Maicai was in an early development phase and used promotional activities to develop new consumption habits among consumers. Yes, you guessed it: subsidizing through coupons and discounts. Meituan was losing around RMB 28 per order, while competitor Dingdong, who had been in business for two years, was still losing RMB 18-20.

During the pandemic, high volumes turned the business profitable. A single warehouse could fulfil 7,000-8,000 a day if human resources allowed it. There was even a warehouse doing 10,000 orders per day. While the pace of growth might have slowed down after the pandemic, the overall business of Meituan Maicai has maintained double-digit growth. Before the pandemic, Meituan Maicai had 1,000 - 1,200 daily orders in the Shanghai region. After the peak during the pandemic, orders have stabilized at 1,600 per day.

According to a former Meituan Maicai manager, the overall Meituan Maicai business has broken even. This might feel counterintuitive because, during the pandemic, grocery delivery often was the only way to get food, and the necessity for home delivery has disappeared. However, the pandemic introduced a lot of consumers to these delivery options, and their habits have changed. During the pandemic lockdowns, people could not go out to buy groceries. Post-pandemic, many people in first-tier cities don’t have time to do groceries (or prefer not to spend their limited leisure time on such trivial things). People can place an order when getting off work or riding the subway, and their purchases will be delivered after they get home.

Meanwhile, the Chinese government has implemented policies to support physical vegetable markets and stores in the ‘real economy’. But post-80s and post-90s generations often prefer to buy online and get groceries home-delivered. That’s one of the reasons why traditional supermarkets are in decline or have been forced to adapt and start home delivery. Take, for example, Carrefour, which has closed the majority of its stores (with one of its former locations in the Longemont shopping mall in Shanghai now being used by Alibaba’s new Hema Premier store).

Inside a Meituan Maicai front-end warehouse, Beijing, July 2023.

Meituan Maicai compared to …

Dingdong is the market leader in Shanghai, followed by Meituan and Sam’s Club.

… Dingdong

Dingdong, which we discussed extensively in the previous part of this series, has better coverage in its home base of Shanghai. Dingdong has about 200 front-end warehouses in the city, Meituan 120. Meituan might not be present in certain areas where customers want to buy online, leaving Dingdong as the only option.

Dingdong attracted capital when it became a preferred supplier during Shanghai lockdowns. It also received a lot of recognition from consumers. Furthermore, Dingdong has proven itself very capable of reducing costs and improving operational efficiency.

Meituan, on the other hand, has strong brand awareness and can use traffic generated in the main Meituan app. It is very strong in customer acquisition. Meanwhile, Dingdong has to rely on (offline) customer acquisition, e.g. promotional activities around subway stations in the morning. Many of Meituan Maicai’s webmasters used to work at Dingdong, switching employers during some of Dingdong’s more difficult periods.

Despite its promise to deliver in 29 minutes, Dindong’s average delivery time is more like 40-50 minutes. Meanwhile, Meituan Maicai claims that 80% of its orders are delivered within 30 minutes. But many consumers beg to differ and say that while 30 minutes is advertised, it usually takes Meitan Maicai an hour to deliver, thereby not doing any better than Dingdong.

… Sam’s Club

Sam’s Club mainly focuses on wholesale and memberships. It combines front-end warehouses and large physical stores and is doing very well at the moment. Sales at Sam’s Club are impressive, especially during weekends. Its offline stores sometimes sell RMB 3-4 million per day. Around these ‘mother stores’, Sam’s Club has set up many ‘sub-warehouses’, which are basically front-end warehouses. The integration of Sam’s Club’s membership model with low prices (through a very limited number of SKUs) and China’s instant retail approach has resulted in a remarkably successful transformation into the Chinese market, especially for a foreign brand.

At Sam’s Club, Meituan Maicai is seen as one of the main competitors for the future. Without a doubt, this also applies the other way around.

Sam’s Club and JD Daojia (or is it competitor Ele.me?!) couriers in Beijing, October 2023.

… JD Maicai

Jingdong (JD.com) launched JD Maicai earlier this year. Like Meituan, JD has its own army of delivery drivers. That advantage, combined with a still very large fresh food market, must have been a reason for JD to try out the front-end warehouse model. JD must have seen the market's growth during the pandemic and wants to get a slice of the big cake. Like Meituan, JD should be able to build on its brand awareness and primary app traffic.

Another possible reason for JD’s interest in the front-end warehouse model is that it lacks user scale and consumption frequency. According to Lianshang, this is one of the main reasons for JD’s low valuation at the moment. [9] A high-frequency business like grocery shopping could help improve users' traffic to its app.

According to a former Meituan Maicai National Operations Manager, the strongly centralized Meituan has lower levels of autonomy at its warehouses than Pupu and JD Maicai. As a result, warehouses respond slower to emergencies than those of its competitors.

While Meituan Maicai operates in only seven cities, JD Maicai already operates in more than 20. How much impact JD will have on players like Dingdong and Meituan will depend on JD’s determination. In the past, it has shown this was often lacking in areas such as store + warehouse (7Fresh) or community group buying (Jingxi). Furthermore, JD is a latecomer to the market.

Meituan Lightning Warehouses

While you can see Meituan Maicai’s green-clad couriers zipping around residential areas of China’s major cities, there are also yellow Meituan couriers. Some of these deliver food; others work for Meituan’s instant retail marketplace, Meituan Shangou (Meituan Flash Shopping a.k.a. Meituan Instashopping). Meituan Shangou provides a platform and delivery to third-party sellers. It’s like upgrading the delivery of meals from restaurants to delivery of any physical product from any store.

Compared to front-end warehouses, the instant retail marketplace platform model of Meituan Shangou, JD Daojia and others offers a lower proportion of fresh food. Most orders include medicine, flowers, consumer electronics, etc. and therefore have a higher volume. These platforms can often build on other main businesses, like food delivery (Meituan) or robust logistics infrastructure (JD), which can share traffic and costs and keep up relatively stable growth.

For instance, Meituan’s food delivery performs well in Beijing and the northern region, so its instant retail will also perform well there. Therefore, these platforms can even work in third-tier cities if their primary businesses are strong there. However, expanding into areas below third-tier cities will become difficult as their core business cannot expand in these places because, for instance, food delivery has little growth potential in the sinking market.

Currently, the Meituan Shangou platform services about 1 million merchants in 2,000 cities and can add about 100,000 merchants annually. However, as on many other platforms, many merchants are not actually active but have not removed their stores from Meituan. As such, merchant numbers alone don’t say much about actual activity.

Meituan Shangou cooperates with more than 4,600 large chain retailers and 370,000 small local merchants. Its 2023 GTV is expected to reach RMB 200 billion, up from RMB 140 billion in 2022. [10]

Solving the problems of instant retail marketplaces

On paper, using Meituan Flash Shopping or other instant retail marketplaces sounds like an excellent opportunity for (smaller) retailers to expand their service area from a few hundred meters to several kilometres. However, the problem with Flash Shopping is that it is often difficult for a merchant to actually make more profit. Since their main business is offline, their online abilities are often lacking. Except for some large supermarkets and verticals, the proportion of online sales could be too small to cover the costs of necessary dedicated staff. Therefore, merchants often need to use service providers and middlemen to help them, increasing their costs. This may lead to poorer product quality (to reduce costs) and a bad consumer experience.

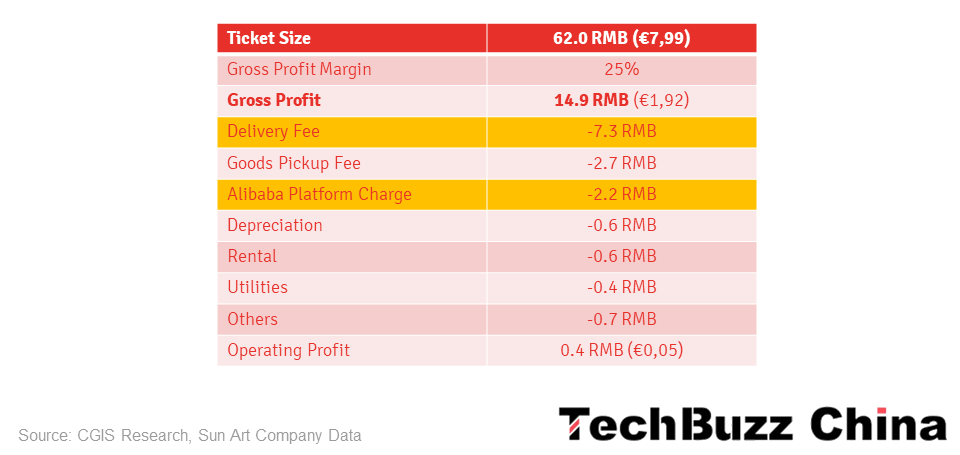

Even RT Mart, which Alibaba invested in, struggled with this problem. With the help of its new owner, it digitized and started offering instant retail services through Alibaba’s Taoxianda (see Need for Speed 2). In 2019, the delivery fee and platform fee ate into RT Mart’s gross profit to the extent that it would hardly make any profit at all on a home-delivered order when not charging delivery costs to the consumer.

Breakdown of RT-Marts order profitability when using Taoxianda instant retail (2019),

Meituan realized that merchants needed to be supported in increasing order volume, conversion and improving their operating abilities. It also found that offline retailers could not meet many long-tail needs.

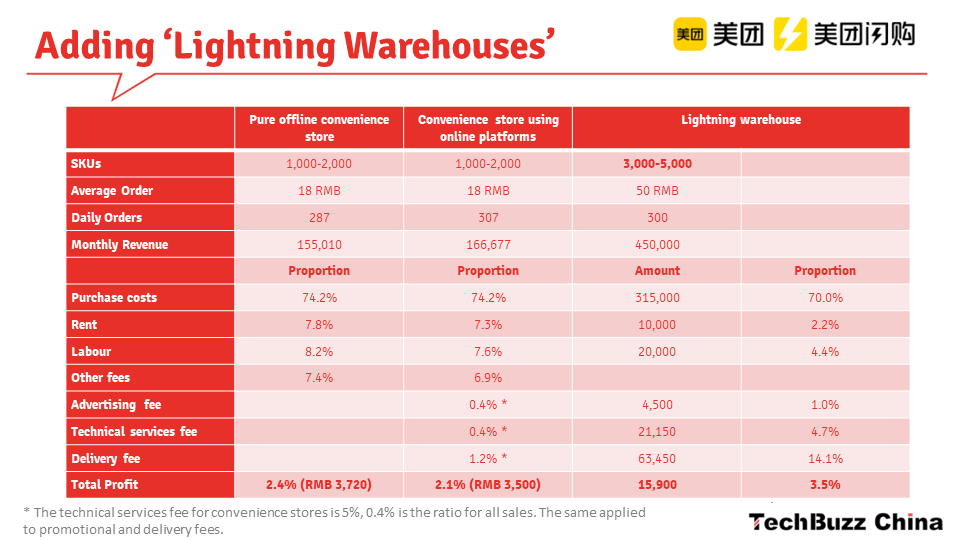

Meituan solved these problems by helping merchants go ‘fully online’ through ‘lightning warehouses’ (闪电仓, shandian cang) in residential areas. A lightning warehouse is basically a 200-square-meter front-end warehouse for Meituan Shangou. If the model of the lightning warehouse had to be described in one sentence, it would be a ‘pure online convenience store, opened 24/7’. Compared with offline stores, lightning warehouses have more SKUs, higher staff efficiency and better profitability for the merchant.

Economies of scale will reduce costs. Tianfeng Securities calculated three scenarios: [4]

A traditional offline convenience store: 2.4% net profit.

A convenience store that also sells online: 2.1% net profit.

A lightning warehouse: 3.5% net profit.

As can be seen, joining an instant retail marketplace could actually lower the profit of a traditional convenience store while starting a lightning warehouse more than quadruple profits.

Lightning warehouses are a type of front-end warehouse, resembling small stores or small warehouses. Meanwhile, the online presentation of a lightning warehouse in the Meituan Shangou app differs little from that of a convenience store. Still, it can be identified based on the number of SKUs and store information. It typically holds 3,000-5,000 SKUs (double that of a traditional convenience store), including anything from daily necessities and fast-moving consumer goods like fresh fruit to office chairs. It is usually located at the edges of business districts. Meituan couriers that are not delivering food fulfil the orders that are placed with these warehouses. The warehouses themselves have four staff members and are open 24 hours a day. [21]

There are two forms of lightning warehouses. The first involves merchants renting a warehouse in a residential area. The other is a pop-and-mom shop. There are also two types of merchants: the first type already has a convenience store (including pop-and-mom shops), and the other type is a new internet company that needs to rent its own warehouse.

Meituan lightning warehouses use Meituan Morning Glory (美团牵牛花, Meituan Qian Niu Hua), a dedicated instant retail solution, to help traditional offline pop-and-mom stores achieve digital transformation, improve efficiency and reduce costs. Morning Glory also helps brands improve efficiency and operations. The system is used in 40,000 stores across 200 cities. [12]

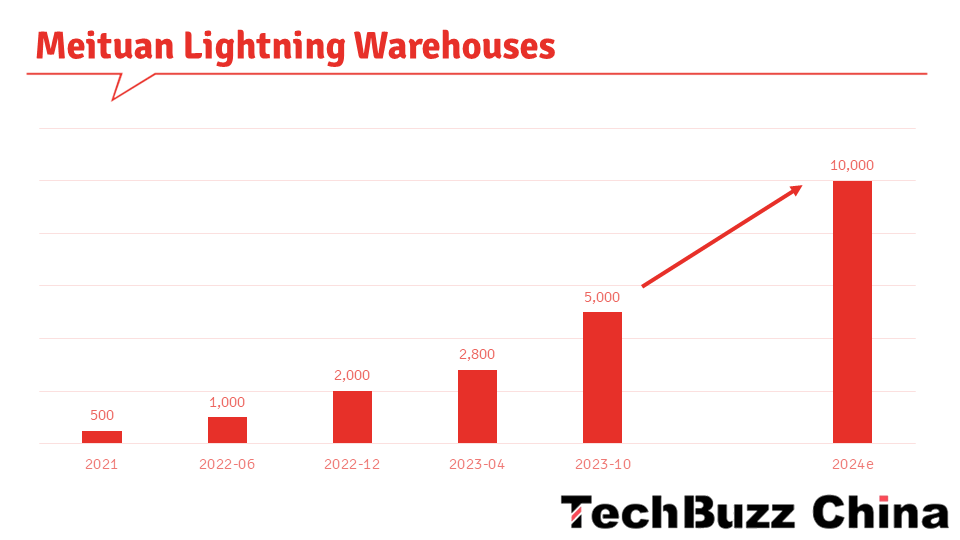

Meituan started implementing lightning warehouses in 2020-2021, launching pilot projects in cities like Shanghai and Beijing in September 2020.

In 2021, there were 500 warehouses, each receiving 290-300 daily orders.

By June 2022, there were more than 1,000 warehouses in 100 cities.

By the end of 2022, 300+ merchants were operating 2,000 warehouses with 320 daily orders per warehouse. 11-12% of them were professional merchants, including convenience stores.

By April 2023, there were 2,800 lightning warehouses.

According to an October report by 36Kr, the number of Meituan lightning warehouses has already exceeded 5,000. [10]

Meituan is giving priority to lightning warehouses. It plans to open 10,000 lightning warehouses between 2022 and 2024.

Meituan has also opened the ‘crooked horse alcohol delivery’ service (歪马送酒, Wai ma song jiu) that runs from lightning warehouses in six cities in Guangdong. It was very successful thanks to the high margins on alcoholic products. [19]

Lightning warehouses are characterized by franchising and pure online operations, and the launch of products in lightning warehouses requires communication and coordination with lightning warehouse franchisees. Meituan enables real-time delivery capabilities, while franchisees independently control the online products, retail prices and profits.

The franchisees independently source goods for their lightning warehouses. Still, Meituan provides advice on product selections, using fast feedback from consumers. User retention is better with lightning warehouses than with regular shops.

Meituan will also guide merchants on location selection before opening a store, decoration layout, and brand traffic support. Merchants have to do the operational work, such as site selection, hiring personnel, purchasing equipment, and preparing resources, including water, electricity, and labour costs.

On the other hand, lightning warehouses have stricter requirements, like 24-hour opening hours and not operating offline. Merchants that start a lightning warehouse on Meituan also sign an exclusivity agreement and cannot operate on other platforms. However, products launched by lightning warehouses are not exclusive, and it is hard to monopolize the sales of specific product categories. Products will overall be more expensive than on, e.g. Tmall, but they have the advantage of speedy delivery.

Currently, more than 5,000+ merchants are cooperating with Meituan through lightning warehouses.

The economics of lightning warehouses

While front-end warehouses like those of Dingdong Maicai or Meituan Maicai see more orders (800-1,600 per day), the number of online orders a lightning warehouse receives is much higher than those that supermarkets and convenience stores receive through Meituan Shangou or their own delivery services. The average daily order of the lightning warehouse is 300+, which is 40-50% higher than that of ordinary convenience stores.

They are in the initial development and exploration stage, and it is challenging to bring large-scale revenue to franchisees in the short term; Meituan can provide franchisees with corresponding data dashboards to help with user and demand analysis.

The average order value for lightning warehouses is also higher than that of other stores on Meituan Shangou because they offer more SKUs. Marketing activities also help raise the AOV. When a warehouse has 300 orders per day - a volume that can be reached by 70% of the lightning warehouses - its profit margin will be 3.5%. When it reaches 350 orders, the margin will be 4.4%.

An RMB 50 sale (twice the average order value of a convenience store) from a lightning warehouse breaks down as follows:

70% - purchase costs (costs of goods)

2.3-2.5% - rental costs

4.4% - labour costs

4.7% - platform costs (technical service fees)

14% - fulfilment costs (incl delivery)

1% - advertising & marketing costs

3.5-3.8% - net profit

Meituan mainly collects three types of fees that can be seen in the above breakdown:

Delivery fee: the platform gives couriers a guaranteed delivery fee of 3-5 yuan per order, depending on the type of city. For example, the guaranteed minimum delivery fee in third-tier cities is RMB 3 per order, and the guaranteed minimum delivery fee in first- and second-tier cities is RMB 4-5 per order.

Technical service fee: a commission rate of 5-10%.

Advertising fee: franchisees can increase store traffic by placing paid advertisements, such as cost-per-click (CPC) and display adverts (CPM).

Meituan can provide discounts such as commissions, subsidies, and advertising fees for franchisees with larger scale and more resources.

Meituan’s lightning warehouses have 10,000 monthly orders per store, and a store can produce 150,000 to 200,000 orders a year. Top-ranked stores like Jiamei Legou Supermarket, Duo Duo Select and Happy Shop (Haitun Gou) all have 30+ warehouses.

The costs of running a lightning warehouse are substantial. Opening one in a city like Chengdu can cost RMB 400,000 (including rent, manpower, etc). In a first-tier city, the start-up capital needed for a lightning warehouse is even higher at RMB 560,000. The sunk costs are RMB 83,000 and have a payback period of 3 months. The monthly turnover will be RMB 550,000, and the gross profit will be RMB 274,000. The monthly operating costs are RMB 239,00, and the net profit RMB 35,000.

The figures in second and third-tier cities will be different, with net profit being RMB 32,000 and RMB 26,000, respectively. The ROI period is estimated to be two months in second tier and three months in third-tier cities, depending on the merchant's initial investments.

Most warehouses can currently be found in first- and second-tier cities because the lightning warehouse is more suitable for relatively prosperous and dense areas in terms of overall layout planning. Second-tier cities are expected to host 50+ lightning warehouses. There are relatively few such core areas in lower-tier cities.

Mature lightning warehouses have already achieved profitability. A lightning warehouse that has been open for over a year, has a store area of 300 square meters and stocks 5,500 SKUs can achieve a transaction volume of 500 daily orders and an AOV of RMB 40. Revenue can reach RMB 600,000-800,000 monthly, and the overall gross profit rate can reach 30%.

Lightning warehouses vs front-end warehouses

Lightning warehouses are open 24 hours daily, while front-end warehouses usually close at night.

Lightning warehouses vs Meituan Select

There is a significant difference between the business models of Meituan Select (Meituan's community group buying concept) and Meituan's lightning warehouses. Meituan Select belongs to the category of next-day e-commerce, while lightning warehouses provide instant retail.

From a consumer's perspective, there is no concept of an online store in Meituan Select, while a lightning warehouse is like an online store on a platform. With a lightning warehouse, a consumer selects a store in Meituan Shangou and chooses products. On Meituan Select, a consumer does not select a merchant but buys from the platform. In the backend, these goods are provided by merchants, but this is not visible to the consumer.

In the case of lightning warehouses, supply, sales and marketing are all done by the merchants. In the case of Meituan Select, a merchant only supplies the goods, and Meituan does the marketing and sales.

Product selection will also differ between the two business models because they have different target audiences. Meituan Select is focused on price-sensitive consumers and lightning warehouses on speedy delivery for time-sensitive consumers, often charging higher prices.

Lightning warehouses vs Meituan Maicai

Lightning warehouses are also different from the business model of Meituan Maicai. Meituan Maicai is a self-operated B2C platform by Meituan. Its product quality will be higher than that of Meituan Shangou (and therefore lightning warehouses), where merchants, not Meituan, control the quality.

Meituan Maicai's orders are delivered by full-time couriers working for the platform, while Meituan Shangou (and the lightning warehouses) share couriers with meal delivery (Meituan Waimai).

A Meituan courier taking a power nap, Beijing 2023. Photo: Evelyn van Leur-Slager.

As a result, both storage and labour costs, and therefore the potential losses, are higher for Meituan Maicai. With Meituan Shangou (and the lightning warehouses), the merchant bears the costs for site selection, storage and delivery, while the Meituan platform remains very asset-light.

Asset-heavy models like Meituan Maicai are more suitable for high-end urban core areas with high-net-worth customers or customers with high service and quality requirements. It is similar to Hema Fresh or Meituan’s former Ella (Xiao Chang) supermarkets and needs a high density of customers and a large order volume to cover its operating costs. Ella was closed after several years because its operating costs were too high. Meituan Shangou is also suitable for less dense areas, and Meituan Select and group buying models work for low-density areas.

Conclusion

Instant retail has been identified as a new growth market. Data from iResearch shows the compound growth rate of orders is expected to reach 28% from 2021 to 2026. [3] With Meituan Shangou and Meituan Maicai, Meituan has two business models that cater to instant retail customers. Meituan expects its fresh-food e-commerce business to continue growth in the coming years.

There will be competition between these different models because products and service areas overlap. However, Meituan Maicai follows business hours, while lightning warehouses offer 24-hour service. The entry point also differs: Meituan Shangou is available in the Meituan app, but Meituan Maicai has a standalone app. The customers might also differ since many lightning warehouse users are old Meituan Shangou or meal delivery users. As such, the internal competition isn't as intense as you might expect. Moreover, Meituan prefers a certain amount of competition between the two business units. It is willing to have multiple models as long as the consumer chooses one of them and not the competitor.

Meituan Maicai sees high repurchase rates, but its number of locations and market share are low compared to Dingdong. There are several strategies Meituan Maicai can use to improve overall profitability:

Increase coverage in cities it currently operates in (which would, however, require adding more warehouses)

Optimizations (e.g. in route planning for couriers, enabling delivery of more orders per ride)

Further reducing costs (in 2019, the small warehouses had 15-16 staff. Now, a comparable-sized warehouse would only require seven employees)

Increase order value

Increase profit margins through private labels

Meituan plans to increase its investment in Maicai, expand the number of locations, improve timely delivery, service quality and, thereby, repurchase rate.

Meanwhile, Meituan Shangou could fail if smaller merchants cannot make an extra profit through the service, which comes with additional requirements in staffing and costs for technical fees and delivery. With lightning warehouses offering better profitability, we can expect Meituan to further push this form of instant retail .

Meituan CEO Wang Xing initially expected community group buying (Meituan Select) to bring in 300-400 million new users to the company. Those new users would feed into its meal delivery and in-store (group-buying) business. But between 2020 and 2022, Meituan saw its user numbers grow from 480 million to 679 million, falling short of Wang Xing’s expectations. [11] It’s obvious that the high-frequency use must also come from other initiatives like Meituan Shangou and Meituan Maicai.

Starting this year, Meituan has stopped disclosing its annual active user numbers. And we all know what that means …

Key takeaways

Meituan Maicai limited itself to first-tier cities and surrounding areas, while its competitors found the front-end warehouse model challenging to operate outside the upper-tier cities.

Scale and number of fast-moving SKUs is essential in the front-end warehouse business. Meituan Maicai has been replacing smaller warehouses with larger ones that can hold 6,000 SKUs.

While Dingdong is ahead of Meituan Maicai regarding volume and profitability, Meituan might have the upper hand because it can divert traffic from its main app and share costs with other Meituan divisions.

As another player that can divert traffic from its main app, JD Maicai could become a strong competitor… if JD shows more determination to make its initiative work than its previous ventures into grocery.

Meituan Maicai might also be seen as a ‘loss leader’ division that guarantees customer acquisition and traffic flow to more profitable divisions in its primary app.

A weakness of Meituan Maica: Meituan’s strongly centralized management could slow down local operations’ responsiveness to local market developments.

While instant retail marketplaces can help convenience stores expand their customer base, it comes with substantial extra costs.

Setting up a lightning warehouse can increase the number of SKUs offered and, thereby, average order value. It could turn instant retail into a more profitable business for convenience stores.

Sources

Six Degrees Intelligence, a leading global expert network/quantitative research firm that operates in China. Augmented with information from the articles below:

[1] Latepost 2023-03-16 [2] Latepost 2022-04-18 [3] 零售商业财经 2023-07-13 [4] 第三只眼看零售 2023-07-03 [5] 第三只眼看零售 2023-05-24 [6] Fung Business Intelligence 2021-11-18 [7] Technode 2022-04-11 [8] Equal Ocean 2023-03-30 [9] 联商网 2023-10-19 [10] 36Kr 2023-10-12 [11] 36Kr 2023-10-18 [12] 第三只眼看零售 2023-09-20

All visuals by ChinaTalk.nl unless stated otherwise. These visuals may not be used or reproduced without the prior consent of ChinaTalk.nl.