The Thirty-Minute Trap, Mutated: A Retrospective on China’s Instant Retail Reckoning

Meituan, Alibaba, and JD.com fight over who delivers groceries faster: the cost of convenience—profitability or permanent subsidy dependence.

Things that caught our attention

Alibaba’s Q4 revenue missed estimates slightly, while adjusted EBITDA slid 61% – though cloud and international e-commerce grew. The company plans to keep prioritizing AI + cloud integration with e-commerce. (财联社, May 13, 2026)

JD.com posted Q1 revenue of RMB 315.7 billion (USD 43.5 billion, +4.9% YoY), while retail operating profit hit a record RMB 15 billion (USD 2.07B) as active users surpassed 740 million and R&D spending jumped 59% – despite a ~RMB 600 million (USD 83M) antitrust fine from China’s market regulator that weighed on GAAP net income. (第一财经,May 12, 2026)

State Administration for Market Regulation (SAMR) launched a new anti-unfair competition enforcement push, targeting platform economy, tech, and “involution-style” competition via data, algorithms, and platform rules. Authorities will strengthen trade secret protection and boost compliance oversight on platforms, aiming to curb predatory pricing and promote fair, quality-based competition. (National Business Daily, May 13, 2026)

Table of Contents

A year in review: how big was the burn, really?

So where did the spending go? The migration from coupon to AI agent

Market Share: Three Estimates, Three Conclusions

Three operating models. So which one survives?

Why couldn’t the unit economics hold?

The Rider Asymmetry: Why JD.com Bought Food Delivery

The China-US Cost Differential

The three platforms, six months later

Where did the value actually go? The neutral logistics layer

What is the regulator actually trying to do, and what does it mean for everyone else?

So if you wanted exposure to this market, what would you actually own?

What we’re watching in the next two weeks

Introduction

Last year, all eyes were fixed on the meal-delivery and instant-retail subsidy war between Alibaba, Meituan, and JD.com. We covered the early innings in real time, and in February we returned to the supply-side response in China’s Internet Companies Get Cooking. Six months on, the subsidy phase has been substantially throttled by regulators, the FY2025 results are disclosed (not guided), and the damage to the stocks is visible. But the competition itself has not ended. It has migrated into a new channel that didn’t exist when we first wrote about this category in 2023, and one of the core questions we asked back then (can a standalone front-warehouse operator ever make money?) has just been answered by M&A rather than by profitability.

This piece is a retrospective on how the cycle actually played out, scored against the calls we made along the way, with an updated read on where the underlying case still points. The headline number for context: combined sales and marketing expense across the three platforms ran to approximately 220 billion yuan (~$30.6B FX) in 2025, with 173 billion (~$24.1B) of that representing the year-on-year increase. That is the largest single-category marketing spend in the history of China’s consumer internet, and it failed to produce a winner.

About this piece

This note draws on TBC’s three-year coverage of the category, FY2025 actuals disclosed in March 2026, Chinese-media analysis of the marketing-spend math (Sina Finance, The Paper, Tencent News), JPMorgan and UBS sell-side research, and Chinese commentary from late March through early May 2026. Prior TBC pieces are linked inline where relevant; the full list is in References. Free subscribers get the summary and year in review; paid subscribers get the company breakdowns, the positioning, and the May earnings catalysts.

Summary View

The headline subsidy format was throttled by regulators; the spending itself has migrated. State Administration for Market Regulation (SAMR) flagged the food-delivery price war as a top-ten “involutionary competition” enforcement case in late January 2026 and summoned seven platforms again on February 13. Direct consumer subsidies are now harder to run. But on February 6, between those two SAMR actions, Alibaba ran a 3 billion yuan (~$420M) Qwen milk tea giveaway: 10+ million free orders in nine hours, framed as “AI agent adoption” and thus protected by Beijing’s “new quality productive forces” framework. Wang Xing’s FY2025 call warned that ongoing competition would keep pressuring near-term earnings, without explicit guidance.

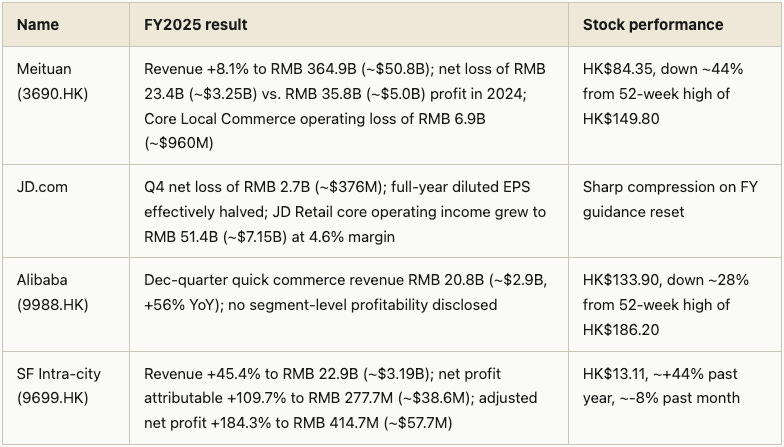

The earnings damage is disclosed, not guided. Meituan reported an FY2025 net loss of RMB 23.4B (~$3.25B) against a 2024 profit of RMB 35.8B (~$5.0B). JD.com’s full-year diluted EPS was effectively halved. Alibaba’s December-quarter quick commerce revenue grew 56% YoY without standalone profitability disclosure.

The market repriced, with the cleanest attribution at the most concentrated names. Meituan, where Core Local Commerce is the dominant business line and that segment swung from profit to a 6.9 billion yuan (~$960M) operating loss, is down approximately 44% from its 52-week high. JD.com’s diluted EPS was effectively halved, with management explicitly attributing the decline to food delivery and new-business investment. Alibaba’s roughly 28% drawdown is harder to attribute purely to instant retail: it reflects the net of instant retail losses, a heavy AI/cloud capital spending cycle (RMB 126B / ~$17.4B in FY26, up 46% YoY, with cloud infrastructure spending surging over 200% YoY), and broader China consumer softness, partially offset by Cloud Intelligence Group growth of 36% in the December quarter. We’re confident in the subsidy-cycle attribution at Meituan and JD.com; less so at Alibaba.

The most thesis-relevant new development is M&A. On February 5, 2026, Meituan acquired 100% of Dingdong Maicai’s China operations for approximately $717M (~RMB 5.15B), outbidding JD.com. The only independent front-warehouse operator with proven turnaround unit economics now sits inside Meituan’s stack. The standalone-investability question we asked in October 2023 has been resolved by consolidation rather than by independent profitability.

The neutral logistics layer is where the case still holds. SF Intra-city (9699.HK) reported FY2025 revenue of RMB 22.9B (~$3.19B, +45.4% YoY) with profit attributable to owners +109.7% and adjusted net profit +184.3%. The shares are up roughly 44% over the past year. We continue to view this as the cleanest setup on fundamentals.

A year in review: how big was the burn, really?

The summer of 2025 marked the largest concentrated capital deployment China’s consumer internet has ever committed to a single category. Alibaba committed 50 billion yuan (~$7.0B) over twelve months to Taobao Flash Delivery (淘宝闪购), since rebranded as Taobao Instant Commerce. JD.com launched multiple ten-billion-yuan (~$1.4B-each) rounds funding Seconds Delivery (京东秒送) and a parallel food-delivery push that, as we argued in Go Fetch!, was about manufacturing rider density rather than competing on lunch share. Meituan, as incumbent, defended at materially lower absolute cost.

The marketing-expense numbers tell the cleanest story. Per Tencent News, the additional marketing spending in Q2-Q4 2025 broke down as Alibaba +83.7B yuan (~$11.6B), Meituan +38.7B (~$5.4B), JD +34.7B (~$4.8B), for about 156.8B yuan (~$21.8B) combined over nine months. The Paper put cumulative Q2-Q3 subsidy outlays at over 220B yuan (~$30.6B), more than every prior major Chinese internet subsidy war combined. Sina Finance put total annual marketing spend at roughly 173B yuan (~$24.1B) (1,730 亿元). Alibaba’s Q3 2025 marketing alone hit 66.5B yuan (~$9.3B), +105% YoY, a record for any single quarter. Alibaba was the aggressor; Meituan ran at less than half Alibaba’s pace. [Note: those three numbers don’t reconcile to one “total burn” figure because they measure different things. Each is correct in its own frame.]

By late autumn, Meituan was guiding to a near-record net loss, Fitch had called the pricing unsustainable, and the regulator was telegraphing intervention. It arrived in two phases. The January 2026 Economic Daily editorial paired with on-site SAMR investigators marked phase one; the February summoning of seven platforms converted policy into ongoing supervision. By the time FY2025 results landed in March, the headline subsidy format had been substantially curtailed. The spending behind it had not. Which leads to the part of the story Chinese commentary in April caught up to: the war didn’t end, it changed shape.

So where did the spending go? The migration from coupon to AI agent

If you tried to order a milk tea in China during Lunar New Year, you already know the answer. On February 6, 2026, Alibaba launched the Qwen “Chinese New Year Treat Plan”: a 25-yuan (~$3.50) no-threshold voucher for free milk tea redeemable at 300,000+ partner outlets (Mixue, HeyTea, Chagee, Luckin, others). Users claimed vouchers by updating the Qwen app and ordering via voice or text. Over 10 million orders cleared in nine hours, Qwen briefly topped the China App Store ahead of Tencent’s Yuanbao, and the committed budget was approximately 3 billion yuan (~$420M).

Stripped of the AI framing, this is a category subsidy. The economics are indistinguishable from the consumer coupons SAMR has been throttling. The framing is materially different: technically an AI agent adoption promotion, sitting inside Beijing’s “new quality productive forces” framework, with real regulatory cover. The same week SAMR was summoning the major platforms over excessive competition, Alibaba was running the largest single-day instant retail subsidy event of the cycle. JD.com, Tencent, and ByteDance ran parallel red-envelope and AI-adjacent campaigns through the same window. Pinduoduo’s October 2025 entry runs from a more aggressive pricing playbook that pre-dates the SAMR pressure and is harder to fence in.

Two implications. First, the headline subsidy phase is exhausted, not ended. The dominant frame in Chinese commentary as of April 2026 is 卷不动了 (juǎn bu dòng le, “can’t be rolled anymore,” the exhaustion phase of involutionary competition): the platforms cannot afford another year at the 2025 scale, but they have not stopped competing. They have shifted into AI agent adoption (Alibaba’s Qwen channel), supply chain investment (JD.com’s 7Fresh Kitchen build-out), and operational efficiency (Wang Xing’s pivot to “service experience, operational efficiency, and mid-to-high-end markets”). CBNData and 36Kr calling 2026 a year of “infrastructure competition” is now consensus. Second, the case for the neutral logistics layer strengthens, because category orders keep flowing regardless of which channel funds them.

FY2025 Scorecard

The directional implication is consistent across the four names: the platforms that contested the subsidy cycle paid for it in earnings and in valuation, while the neutral infrastructure operator captured a doubling of profitability and a strong relative return.

Market Share: Three Estimates, Three Conclusions

Estimates of post-cycle market share diverge materially depending on whose methodology you accept:

JPMorgan (November 2025): Meituan held ~60% share; Alibaba captured ~9 percentage points of share growth at the cost of approximately 80 billion yuan in subsidies; JD.com bought option value rather than meaningful share.

UBS (February 2026, based on rider-app usage data): Meituan ~67%, Alibaba ~23%, JD.com ~10%. The proprietary-network bias of this methodology favors Meituan.

Yiguan Analysis (end-2025, by gross transaction value): Taobao Flash Purchase 45.2% and Meituan 45.0%, essentially tied. JD.com balance.

The JPMorgan framing is the cleanest cycle narrative: Meituan defended the incumbent position with the lowest absolute losses, Alibaba converted approximately 80 billion yuan of subsidy spend into roughly nine share points (an implied 8.9 billion yuan per share point), and JD.com used the cycle to buy a long-term position in rider density rather than chase share. The 22-point spread between JPMorgan and Yiguan on Meituan’s share reflects the genuine measurement difficulty (GMV captures basket size, rider-app data captures order volume, consumer survey captures stated preference). We weight JPMorgan most heavily because it tracks the consensus among investment-bank analysts whose calls have informed the share price.

Three operating models. So which one survives?

The three-model framework we laid out in 2023 (platform aggregation, front-warehouse, store-warehouse hybrid) is fundamentally unchanged. What’s changed is the survivor list: aggregation is consolidating, hybrid is durable, and the front-warehouse model has just lost its last meaningful independent.

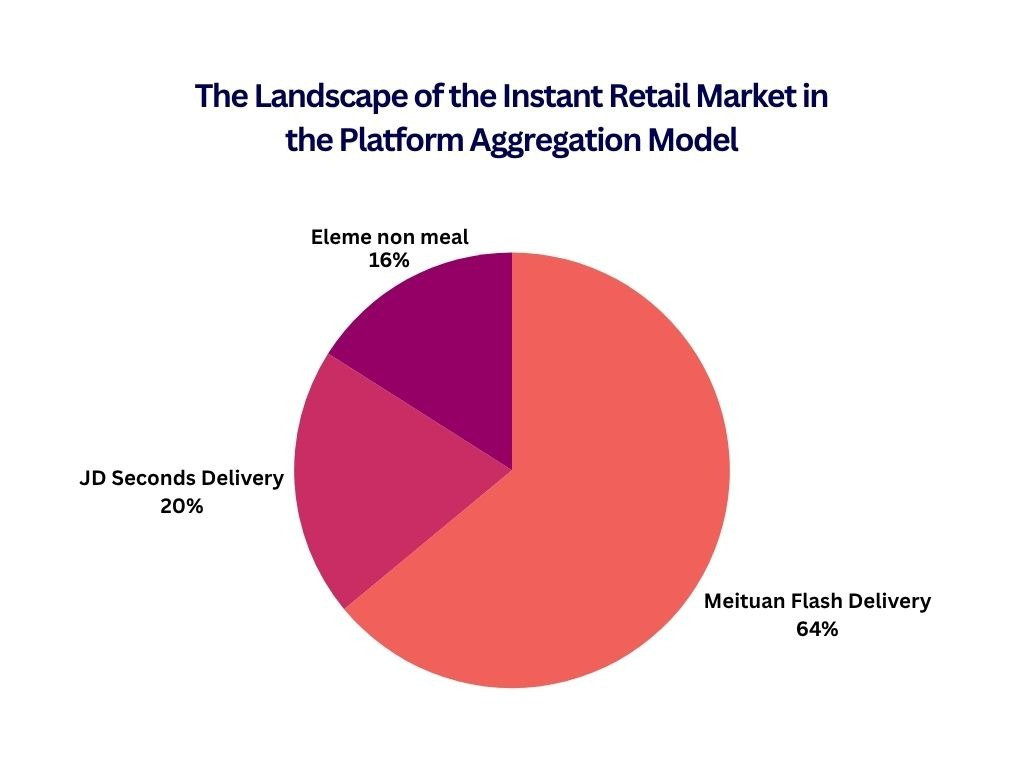

Platform aggregation (Meituan Flash Delivery, JD Seconds Delivery, Taobao Instant Commerce) is asset-light: platforms intermediate between consumers and existing retail outlets without owning inventory. The fundamental weakness, which we have flagged repeatedly, is that platforms own the customer relationship and absorb every reputational hit while exercising limited operational control over merchants. The subsidy-era response was a stack of platform-funded service guarantees that added cost per order. Meituan’s Lightning Warehouse (闪电仓) build-out, now around 30,000 micro-warehouses with Wang Puzhong’s stated 100,000 target by 2027, is a partial retreat from pure aggregation toward direct supply control. Subsidy spending was effectively bridge financing for that transition.

Dark store / front-warehouse is where the population of independent operators just collapsed. We asked in October 2023, with some skepticism, whether any standalone operator could ever escape the unit economics. The category produced two answers. MissFresh (每日优鲜, Měirì Yōuxiān) was the failure case: bankruptcy and Nasdaq delisting after accumulated losses topping 10 billion yuan (~$1.39B). Dingdong Maicai (叮咚买菜, Dīngdōng Mǎicài) was the proof of concept: average order size up from about 50 yuan in 2021 to over 70, gross margin expansion of ~10 points, and a 13.8% reduction in fulfillment expense ratio. Then, on February 5, 2026, Meituan acquired 100% of Dingdong’s China operations for approximately $717 million (~RMB 5.15B), beating JD.com. Dingdong’s strongest footprint is in Shanghai and Eastern China, exactly where Meituan’s Xiaoxiang Supermarket has been under-indexed; the infrastructure accelerates Meituan’s plan to open ~700 new front warehouses on top of its existing 1,000+. The 2023 question gets a slightly awkward answer: one operator demonstrated the turnaround, then was acquired by the strongest aggregator before it could compound the advantage at scale. Standalone investable exposure to this model effectively no longer exists.

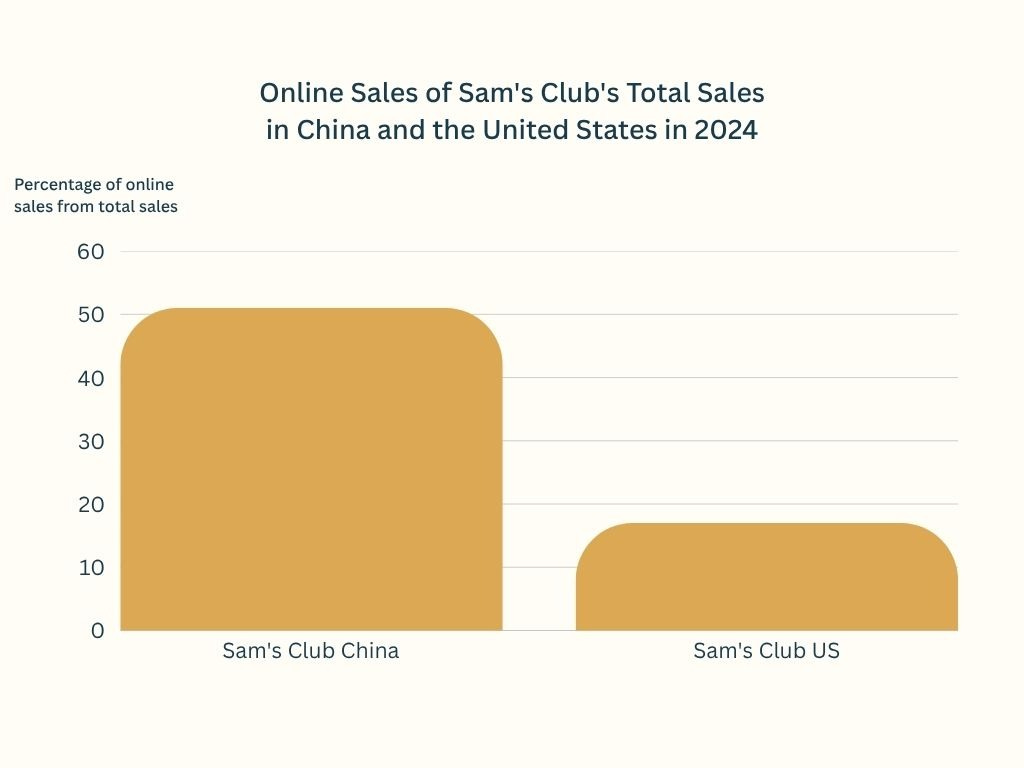

Store-warehouse hybrid (Freshippo, Walmart, Sam’s Club China) turns existing stores into fulfillment nodes that share inventory across digital and physical channels. Per China Daily (December 2025), Walmart China’s e-commerce now accounts for over half of total sales, with Sam’s Club as the dominant share. Sam’s Club’s typical order size of about 230 yuan (~$32), per 36Kr, absorbs even premium third-party delivery economics. Asset-heavy, defended by real estate and supply chain discipline rather than network effects, expanding at the speed of physical retail. We profiled the canonical Alibaba operator in Staggering Hippo in May 2024.