Temu Watch #12: Update on Markets, Advertising & Logistics Strategies

Important Note on Temu Watch series

This report will be my last publication on Tech Buzz China. I am continuing my writing on China Digital Retail Report (CDRR), where I will post weekly about insights from Chinese tech and business media, videos of interviews and keynotes and a monthly deep dive review full of exclusive insights. The latter are comparable to my publications on Tech Buzz China in the past 3.5 years.

The Tech Buzz China team will continue to publish reports on Chinese internet companies, so please continue to follow and support them, but on CDRR I will fully focus on activities of these companies in online and offline retail, including e-commerce, local services and cross-border e-commerce. My Temu Watch and TikTok Shop Watch series will also continue on CDRR. CDRR will have a free and a paid subscription. If you want to continue receiving my updates in your inbox or Substack app, please subscribe to CDRR.

Leaves me with thanking you as readers for your interest in my work and wishing the Tech Buzz China team all the best with their continued efforts in bringing reliable China tech news, research and (investor) trips to a wider audience.

Now, on with the show …

Ed Sander, China Digital Retail Analyst

Contents

Introduction

This report is the first of two new publications with updated insights on Temu. They were compiled from over 15 interviews with Chinese experts close to Temu. This first report, Temu Watch #12, is available for free to read on Tech Buzz China.

In the text below, we share updates on Temu’s business development across global regions, as well as the progress of different operational models, merchant margins, advertising spending in the last quarter, and adjustments to logistical processes.

Temu Watch #13, available on China Digital Retail Report later this month, will include updated information on Temu’s GMV, profitability and plans for 2026.

Markets

The International Post Cooperation (IPC) recently published its latest edition of the Cross-Border E-Commerce Shopper Survey. In this survey, 30,970 participants from 37 countries worldwide were asked where they made their last cross-border e-commerce purchase. They found that in 24% of all cases, the answer was Temu, equal to Amazon. [Note: this says little about purchase frequency and even less about order value. Also, Amazon is not active in all countries surveyed.] [1]

</em>")

Source: IPC [1]

Meanwhile, with 246 million monthly active users, Temu ranked third among global e-commerce apps in 2025, according to Similarweb. Amazon remained the market leader with 651.7 million users per month, followed by Shopee with 392.8 million. [2]

Temu’s main business scope covers the Middle East, the United States, Europe, Australia, New Zealand, and the Japanese and South Korean markets.

Among Chinese players, Temu stands out globally with approximately 15% market share, while Shein follows closely behind with over 10%. Meanwhile, TikTok and AliExpress have market shares between 8% and 9%. However, an interesting contrast emerges in the global market's geographical distribution. AliExpress and Shein have covered over 200 countries, while Temu and TikTok’s international expansion is relatively limited. Specifically, Temu’s business spans over 100 countries, primarily in North America, Europe, and Latin America, with limited penetration in African and Middle Eastern markets.

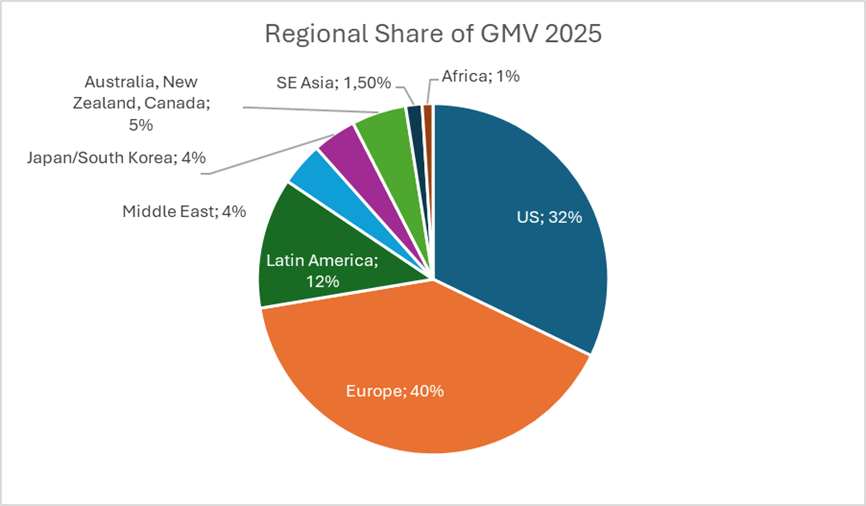

In 2025, Europe was the primary source of Temu’s revenue, accounting for approximately 40% of total merchandise trade volume, while the United States accounted for about 30%. Latin America reached 12%; the Middle East and Japan/South Korea each accounted for about 4%; Australia, New Zealand, and Canada combined accounted for 5%; Southeast Asia for 1.5%; and Africa for 1%.

Looking ahead to 2026, the European market’s share is projected to rise slightly to between 40% and 45%, the US market’s share is expected to remain at 25%-30%, the expected share of the Latin American market is expected to increase to 15%, and the total merchandise trade volume share from regions outside Europe and the US is planned to increase to 30%.

Temu’s current strategic focus is on the Latin American and Southeast Asian markets. Both Southeast Asia and Latin America will see annual growth rates exceeding 30%. While the Middle Eastern e-commerce market is growing rapidly, Temu’s expansion in the region has been slow, primarily due to political and regional instability, with Israel as a prime example.

In terms of market potential, the Middle East's future development is similar to that of Latin America, while Southeast Asia's growth potential significantly exceeds that of both regions. While the Latin American market is geographically distant, it possesses enormous consumer potential despite high logistics costs. The Middle East, comprising 17 countries including Egypt, Iran, Israel, Lebanon, Pakistan, Palestine, and Saudi Arabia, boasts a large population and strong purchasing power.

Looking at the broader market outlook, the total transaction volume of Chinese e-commerce on overseas platforms was expected to reach $500 billion by the end of 2025, with Temu projected to account for approximately 18%, equivalent to $100 billion. Looking ahead, the development of the cross-border e-commerce industry will primarily rely on increasing repurchase rates among existing users and attracting new consumer groups.

USA

Among Temu’s markets, the US is the most mature, and the company has already established a strong foundation in US marketing, compliance management, and overseas supply chain operations.

In 2025, growth in the US region lagged behind Temu’s overall business performance, primarily due to the elimination of tariff exemptions for packages under $800 in the second quarter. Furthermore, business recovery was slow in the third quarter, returning to pre-tax-adjustment levels only by September.

In the US e-commerce market, Walmart and Amazon are the two major platforms, together holding approximately two-thirds of the market share. Of the remaining market share, cross-border e-commerce platforms account for one-third, with Temu and Shein holding approximately 60% to 70% thereof, while AliExpress and TikTok together hold the remaining 20% to 30%.

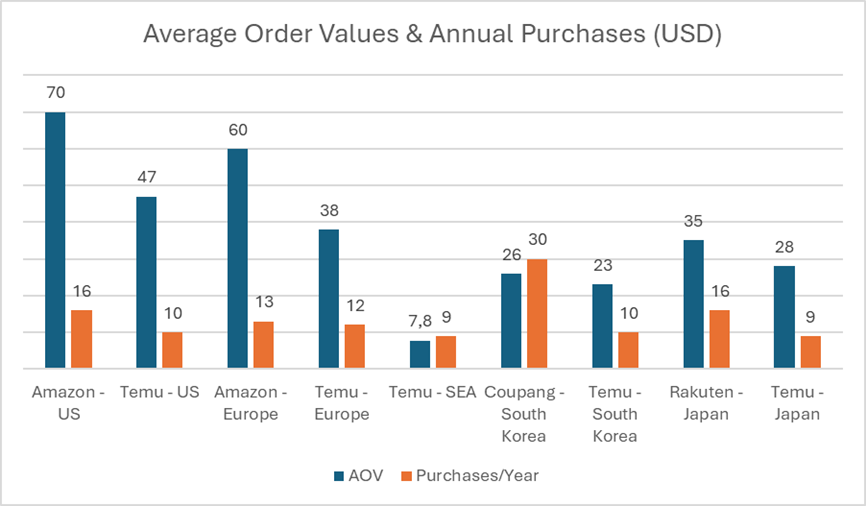

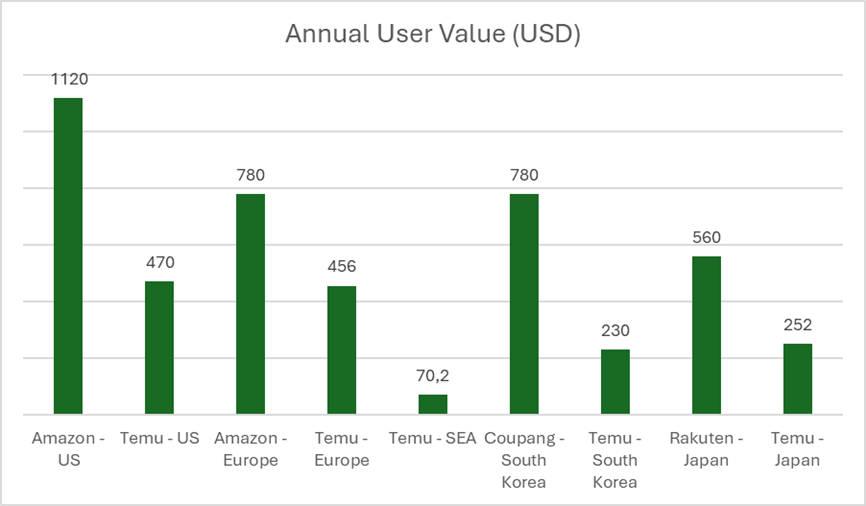

In the US market, Amazon’s cost to acquire a user exceeds $100, with users spending approximately $1,120 annually, averaging $70 per order and 16 orders per year. In contrast, Temu’s average order value is $47, with 10 orders per year and an annual user value of $470.

In 2023, Temu surpassed 30 million users in the US, and planned to add approximately 15 million users each in 2024 and 2025, aiming to achieve second place in the US e-commerce market. Temu currently has approximately 60 million users in the US, while Amazon has 300 million, a significant difference in user scale. While the company is poised to take a leading position in the European market, it faces a considerable gap in competition with Amazon in the US. Still, the company plans to achieve the largest scale in business among all Chinese cross-border e-commerce companies.

According to Temu, American consumers don’t have the same strong demand for low-priced goods on e-commerce platforms as Europeans do; they are more willing to pay extra for high-quality products. Furthermore, consumers are sceptical about the quality of products from Chinese e-commerce platforms. In the categories of electronics, licensed goods, branded products, and high-value goods, American consumers trust Amazon more.

In the food and fresh produce sector, American consumers prefer traditional retailers like Walmart, making it difficult for Temu to make significant inroads. American brands have strong independent sales channels and do not rely on distributor systems, making them unwilling to implement price reduction strategies on Temu, a significant difference from the situation in the Chinese market.

The regulatory environment in the US market has stabilised, with tariffs remaining around 25% and having a minimal impact on business operations. Temu has changed its operating strategy; previously, duty-free parcels under $800 were shipped directly via airmail, but now most goods are stocked within the US, either using the semi-managed model or forward warehouses for the fully managed model (see Temu Watch #10). The company employs a fully managed forward warehousing strategy, leasing overseas warehouse facilities to pre-ship goods to the US by sea to avoid high tariffs and reduce air freight costs. To reduce costs, approximately 97-98% of goods shipped to the US market under a semi-managed model are imported from China.

Clearance Sales Market

The US has a surplus inventory market of approximately $50 billion annually, and Temu aims to capture one-third of it. However, most merchants don’t rely solely on Temu for inventory clearance, employing various sales strategies, including secondhand platforms like eBay and offline retail channels. Notably, offline retailers like Dollar Tree have gradually recovered and successfully diverted a significant amount of surplus inventory, thanks to Temu’s influence. This suggests that Temu has not yet fully attracted merchants or become the optimal choice for clearing surplus inventory.

The US offline clearance sales channel is revitalising, primarily due to two key factors. First, there’s the issue of delivery time. With Temu’s fully managed operation model, goods took 10-11 days to reach US buyers. While semi-managed and localised operations can shorten delivery time to about 3 days, this remains a competitive disadvantage. Second, Temu’s price competitiveness is weakening. Its significant price advantage of 50-70% over offline retailers has shrunk to 80-90%. Consumers are naturally unwilling to wait more than ten days for a small price difference. More importantly, low- and middle-income consumers, as well as non-middle-class consumers in the US, mainly rely on brick-and-mortar stores, with approximately 80% of transactions for these goods completed offline.

When Temu’s price advantage diminishes, these users are more inclined to return to traditional offline shopping. Against the backdrop of inflation, brick-and-mortar retail channels pose significant competitive pressure on Temu. In physical stores, the price already includes all taxes and fees, whereas on Temu, consumers must pay additional taxes, reducing the platform’s attractiveness.

Europe

The European e-commerce industry is projected to grow at around 20% in the future, higher than the US’s 10%, but still lower than the 30% growth rate in Latin America and Southeast Asia.

The European e-commerce market features a diverse competitive landscape, unlike the North American market, where a single company dominates. While Amazon holds the top market position, local e-commerce companies and Chinese cross-border e-commerce platforms have roughly equal market share. The more balanced competitive landscape in Europe provides broader market opportunities for various platforms, particularly benefiting Chinese cross-border e-commerce platforms. By establishing their own warehousing facilities and pan-European logistics networks, Chinese e-commerce companies can manage logistics and goods more efficiently.

In the European market, Amazon’s average order value is $60, with 13 orders per year and an annual user value of $780. Temu’s average order value is $38, with 12 orders per year and a relatively low annual user value.

Since expanding into the European market in 2023, Temu has seen rapid growth in users. Temu has 130 million active users in the European market, while Amazon, which has been operating in Europe for many years, has 181 million, according to its DSA transparency report.

Asia

In Southeast Asia, Temu’s operations in Vietnam were suspended due to Ministry of Industry and Information Technology approval processes but have now resumed; meanwhile, Indonesia’s regulatory policies are gradually easing, providing opportunities for entry for Chinese cross-border e-commerce companies.

Chinese cross-border e-commerce platforms have captured 50% market share in Southeast Asia; however, this growth is primarily driven by price wars and lacks long-term sustainability. Currently, the Southeast Asian e-commerce market is dominated by Lazada and Shopee, companies with strong local foundations. Therefore, Chinese cross-border e-commerce companies are unlikely to pose a direct threat.

Temu’s average order value in Southeast Asia is $7.80, with an average of 9 purchases per year. In this market, Shopee holds approximately 50% market share, with users averaging about 15 purchases per year. Lazada and TikTokShop each hold 17-18% market share, while Temu’s share is around 12%.

In addition to North America, Europe, Southeast Asia, Latin America, and the Middle East, Japan and South Korea are considered important markets for future development. The Japanese and South Korean markets are enormous and demonstrate significant growth potential.

AliExpress held a 70% to 90% cross-border market share in Japan and South Korea before emerging competitors like Temu, Shein, and TikTok entered the market. However, these new rivals gradually eroded AliExpress’s market position by improving warehousing and delivery and offering price subsidies.

Temu’s performance in the Japanese and South Korean markets is outstanding. Specifically, Temu’s monthly gross merchandise volume (GMV) in South Korea is approximately $350 million, while in Japan it exceeds $600 million. By the end of 2025, the combined transaction volume in these two markets accounted for 8% to 9% of Temu’s global monthly GMV, clearly demonstrating the significant role of the Japanese and South Korean e-commerce markets in Temu’s business. [Note: these figures differ from the 4% quoted by a different expert above.]

The Japanese and South Korean e-commerce markets are projected to grow at 20% annually, surpassing the European market's growth rate. This growth is partly attributed to the untapped potential of the cross-border e-commerce sector.

In the South Korean market, Coupang is Temu’s major competitor, with an average order value of $26, 30 purchases per year, and an annual user value of $780. In contrast, Temu’s average order value is $23, with 10 purchases per year and an annual user value of $230.

In the Japanese market, Temu’s average order value is $28, with 9 purchases per year and an annual user value of $252. Local competitor Rakuten’s average order value is $35, with 16 purchases per year and an annual user value of $560.

Latin America

The rapid expansion of Chinese e-commerce platforms in Latin America is reshaping the region’s competitive landscape. Firstly, in emerging markets like Brazil, attracting new customers who have never shopped online before is crucial, and platforms typically employ subsidies, free shipping, and low-priced products to attract new users. Notably, Temu and Shein are performing better in Latin America than they have in Southeast Asia. Shein, in particular, with its small-batch, rapid-reorder model and efficient supply chain management, is well-suited to the Brazilian market.

Looking at market prospects, internal data from TikTokShop indicates that Brazil and Mexico will be the fastest-growing markets by 2025, and TikTokShop will focus its resources to further strengthen its position against Shopee. However, the advantages of traditional platforms are being challenged. Shopee’s self-operated logistics system is gradually being eroded by Chinese e-commerce companies, which are achieving this by partnering with J&T Express or collaborating with warehouse service providers in target markets.

Temu has designated Latin America as a key development region for 2026 and launched a partner program in Brazil, aiming to expand its customer base by driving user growth and increasing traffic. Notably, Temu’s 14th self-operated warehouse in Brazil was expected to officially open in Rio de Janeiro in December or early 2026. In terms of its overall development strategy, Temu employs a diversified infrastructure approach, including self-operated warehouses, certified warehousing, third-party warehousing, and partnerships with local logistics and delivery companies, to strengthen its infrastructure system. In contrast, TikTok and Shein have similar expansion plans in Latin America, but their main strategy is to attract consumers through price incentives rather than investing heavily in infrastructure construction.

Customer loyalty is high in the Latin American market, and cross-border e-commerce requires significant investment to attract new users. MercadoLibre dominates the Latin American market, making it Temu’s main competitor. Although MercadoLibre’s growth rate may lag behind Temu’s in the first half of 2025, it accelerated its growth in the second half by implementing specific strategies to address the challenges of cross-border e-commerce.

Meanwhile, Shopee’s expansion in the Latin American market has surpassed Temu's, and its scale is also larger, although both have similar growth rates. While Shopee underperformed in some regions, such as Chile, and ultimately withdrew, as Temu’s second-largest competitor, its business coverage still surpasses Temu’s, maintaining its leading position in overall scale.

Temu has just launched a local-to-local business model in Brazil, primarily using a semi-managed operation. However, under this model, most merchant and product resources come from competitors such as MercadoLibre and Amazon. With rising tariffs, its price advantage is not significant.

The latest data shows that Temu’s performance in the Brazilian market is remarkable. In December 2025, Temu’s traffic surpassed MercadoLibre, making it the most visited e-commerce platform in Brazil. This change has had a profound impact on the entire market landscape. Analysing order value, MercadoLibre and Shopee have similar average order values, with the average order value in the Brazilian e-commerce market ranging from $11 to $14, slightly higher than in Southeast Asia. This price range provides competitive space for new entrants.

Particularly noteworthy is the competition in product categories. Fashion apparel accounts for approximately 30% of revenue on MercadoLibre and Shopee platforms, and Temu and Shein’s operating models pose a direct threat to this important category. This threat is not only reflected in price competition but also in supply chain and business model innovation. From a merchant ecosystem perspective, MercadoLibre and Temu have a high degree of merchant overlap, meaning that Temu’s traffic and sales growth will directly intensify competition with MercadoLibre and Shopee, creating a more intense three-way competitive landscape.

Operational Models

In the fully managed model, Temu negotiates the wholesale price with the supplier, although ownership remains with the supplier until the goods are sold. If the goods remain unsold in the warehouse for more than 20 days, they can be returned to the supplier. In this model, after a sale, the system typically confirms receipt after 15 days, and Temu settles payment on a T+1 basis according to the pre-agreed price. In the fully managed model, losses from returns are borne by the platform.

In US operations, companies often employ a semi-managed model. Products are first shipped to a US warehouse, and after a customer places an order, last-mile delivery services like UPS or DHL handle the shipment, typically taking 3 to 5 days. Payment to US suppliers is settled the day after the customer confirms receipt. Temu returns the pre-agreed purchase price to the supplier and profits from the price difference.

In the semi-managed model, ownership of the goods and inventory management are handled by the supplier, who usually already has other business activities or sales channels in the US. In contrast, in fully managed operations in the US market, platforms reduce inventory risk by decreasing the number of suppliers—for example, from 10 to 2 for a particular product category—while simultaneously gaining economies of scale by expanding the scale of individual suppliers.

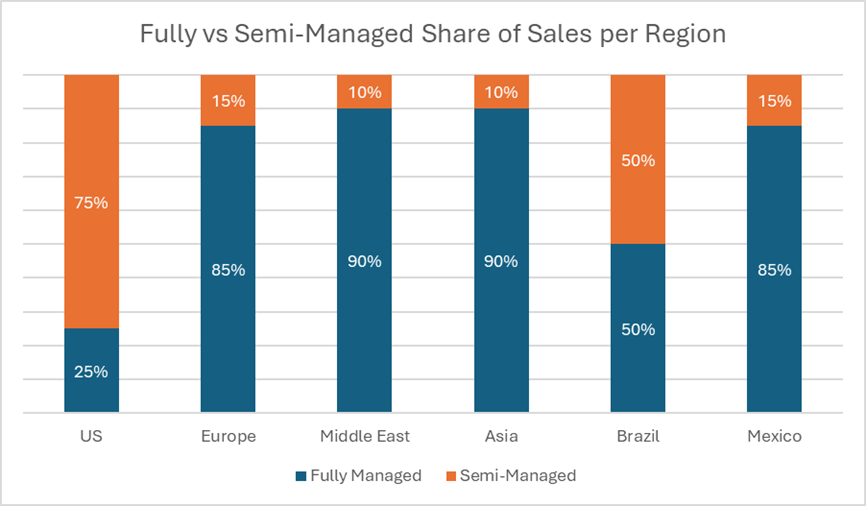

In 2025, Temu’s fully managed services accounted for 65-70% of its business, while semi-managed services comprised 20-30%. Significant differences exist in the operating strategies employed across regions. The US region primarily relies on a semi-managed model, accounting for 75%, while the fully managed model accounts for 25%. In Europe, the fully managed model is dominant, with the semi-managed model accounting for only 15%. In the Middle East and Asia, 90% use the fully managed model, with 10% using the semi-managed model. In Latin America, Brazil employs a hybrid strategy, with fully managed and platform models each accounting for 50%; Mexico uses approximately 85% of the fully managed model and 15% of the semi-managed model.

Last year, only about one-third of the target for semi-managed and local-to-local models in the US market was achieved, while the achievement rate in Europe and other regions was half. Therefore, 2026 will focus on promoting these two models to increase their share of the total merchandise trade volume.

The local-to-local program has been launched in over 30 countries worldwide. [3] However, the semi-managed model and local-to-local operations currently have low revenue, essentially breaking even. Specifically, local-to-local operations have a 6% commission rate, while the semi-managed model, which relies solely on advertising revenue and has not yet begun charging commissions, has an even lower rate.

Y2 model in Europe

Temu launched the Y2 operating model in Europe in November 2025, similar to the model launched in the US in the second quarter of 2025 to address the repeal of the T86 policy (de minimis). This model is similar to the semi-managed model, but instead of asking merchants to store goods in overseas warehouses, it enables Chinese merchants to ship directly from China to US consumers after the order is received. The goal of the Y2 operating model is to convert some fully managed merchants to semi-managed operations, particularly those selling fashion accessories or high-profit 3C products.

Strategically, the launch of the Y2 operating model is to address potential cross-border operational fluctuations following policy adjustments in the first quarter of 2026, ensuring a smooth transition and avoiding significant impact on core business. Although semi-managed and local-to-local operations weakened the price advantage, Temu’s overall strategy is to shift towards high cost-effectiveness rather than simply pursuing the lowest price.

It’s worth noting that the Y2 model aims to shift the burden of tax reform from the platform to sellers and their logistics systems, providing sellers with more flexible adjustment options to avoid a severe impact on business traffic after the removal of tax exemptions.

Merchants

Temu faces some core challenges in its merchant recruitment process. First, the main issue lies in the allocation of pricing control. Currently, most semi-managed merchants have pricing power controlled by Temu, with only a few high-quality merchants or well-known overseas brands able to participate in joint pricing or independent pricing. This weakens merchants’ motivation to migrate from high-yield platforms like Amazon.

Although the local-to-local model lowers the entry barrier and offers preferential policies on commissions, security deposits, and advertising fees, the recruitment results remain unsatisfactory. The retention rate of newly joined merchants is low, and the churn rate is high, directly impacting the achievement of overall goals.

A merchant leaving Temu and sharing his experience on LinkedIn.

Regarding merchant recruitment in the US, the localisation model faces challenges, with only one-third of the planned recruitment expected to be completed by 2025. Notably, during Black Friday in November 2025, the company tried an incentive program offering $1,000 back for referring merchants, which achieved some success, but this method is not sustainable in the long term.

Furthermore, in the US market, many Amazon merchants see Temu as a way to dispose of excess inventory or slow-moving goods, further affecting the platform’s merchant quality. Regarding subsidy policies, Temu provides 30% to 35% subsidies for the semi-managed model, while the local-to-local model allows merchants to set their own prices.

To counter competition from TikTok, Temu has adopted a strategy of attracting merchants through its main domestic platform, Pinduoduo, which accounts for 60% to 70% of its merchants, and restricting these merchants from opening stores on TikTok. Simultaneously, Temu prioritises onboarding opportunities and offers traffic subsidies to the remaining 30% to 40% of its distribution merchants to enhance their competitiveness.

Temu’s online Seller Center.

Promotional Fees & Merchant Profit

Starting in February of 2025, the platform upgraded its promotional system in phases, and it has now achieved near-universal coverage. Although nominally called promotional fees, they are essentially disguised commissions for suppliers. Temu does not charge traditional commissions on product categories; instead, it primarily profits through these promotional fees. Temu’s promotional fees have shown a significant upward trend. From an average of about 6% throughout 2025, they rose to 8-10% in the fourth quarter, and are expected to remain above 8% in 2026.

Temu has implemented new strategies to increase platform revenue, including raising the security deposit for overseas accounts from RMB 10,000 to RMB 30,000 and limiting each supplier to at most two stores. Simultaneously, the platform has raised its compliance standards, requiring merchants to strictly adhere to product listing compliance requirements or risk fines or damage to their brand reputation. Revenue data shows that fines accounted for approximately 3% of the platform’s revenue last year, but in 2025, they have increased significantly. Furthermore, the increased security deposit for overseas accounts has also brought additional revenue to the platform.

Temu’s fully managed model has become less competitive, not only due to tariffs but also because of increasingly fierce competition among similar products on the platform. Furthermore, stricter platform rules have significantly shortened the sales cycle for goods. One expert shared that before 2024, goods typically maintained daily sales of 200-300 units for two to three months, or even half a year. However, in 2025, the sales cycle was compressed to a week, with sales only lasting one to two weeks. Afterwards, the platform system would force price reductions; otherwise, penalties such as traffic restrictions or removal from promotional activities would be imposed. Due to strict enforcement of platform rules, many small merchants abandoned the fully managed business model in 2025.

Temu may impose additional price reductions on top of the merchant’s price, with Temu bearing the cost itself, which merchants cannot intervene in.

Merchant profitability of operational models

Under the fully managed model, suppliers typically maintain a profit margin of 3% to 5% after deducting various costs. Newly launched products may have a profit margin of 8% to 15%, but after three to six months, the profit margin usually falls back to 3% to 5%. This is mainly because the platform uses algorithms and competitive mechanisms to compress supplier profit margins. Under the semi-managed model, supplier profit margins have decreased from over 15% to 8%-12%, a level similar to Amazon’s. In Europe, under the semi-managed Y2 business model, merchants can achieve a net profit margin of 10%.

When assessing the sustainable profitability of fully managed and semi-managed models for merchants, we need to analyse it from the perspective of unit economics, focusing on key factors such as product costs, transportation costs, platform fees, and marketing and advertising expenditures. Looking at recent market performance, the platform provided subsidies during the fourth quarter’s promotional activities, which reduced merchants’ traffic-promotion spending, lowering advertising spending by 2-3 percentage points. Merchants also reduced their traffic promotion spending by approximately 2-3 percentage points by adopting a low-price strategy.

However, changes in cost structure also need to be considered. Due to the large-scale construction of forward warehouse facilities, inventory costs increased by 3-5%, contrasting with the previous direct mail method, where inventory costs were not involved. Specifically, in the fully managed model, the platform reduced procurement costs, resulting in a supply price decrease of approximately 5-10%. Despite increased order volume, merchants maintained a net profit margin of approximately 5% by integrating back-end cost items, including production costs.

In contrast, in the semi-managed model, the platform provides subsidies, especially in the Y2 model, maintaining a higher gross profit margin exceeding 35%. After deducting platform fees, transportation costs, promotion expenses, and cargo losses, the net profit margin is close to 10%, significantly higher than that of the fully managed model. Therefore, from the perspective of sustainable profitability, the semi-managed model demonstrates stronger profitability under current conditions, especially when facing adjustments in platform subsidy policies; its higher net profit margin provides merchants with greater buffer space.

2025 Q4 Advertising

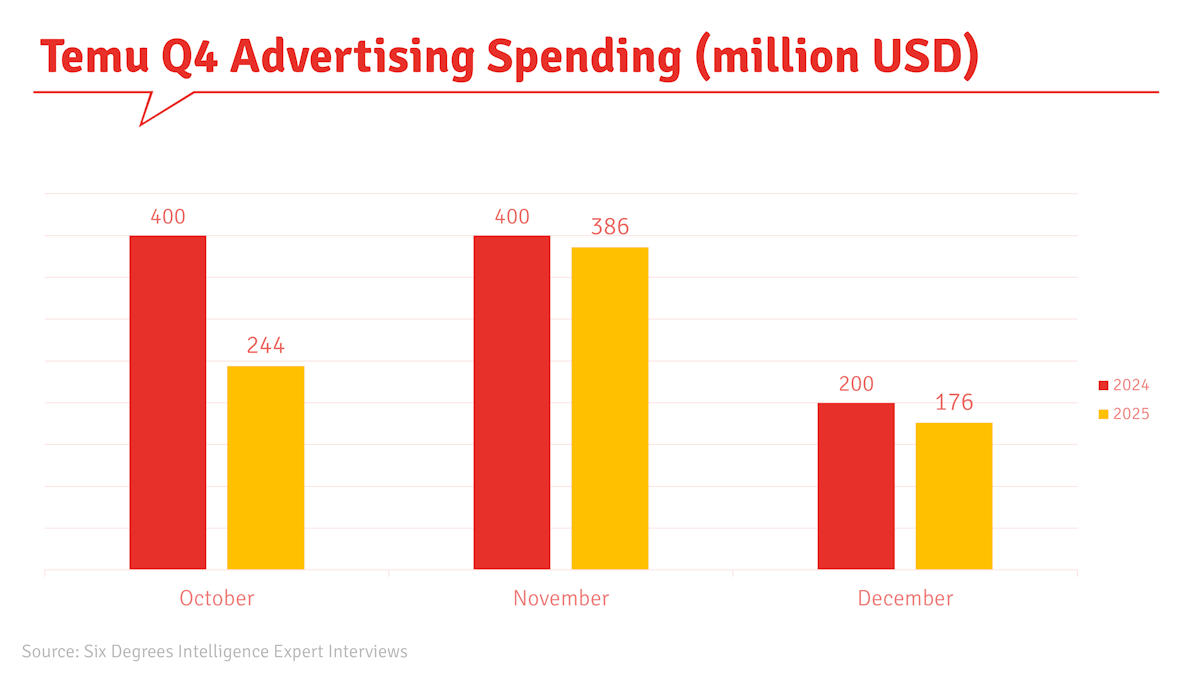

Temu’s overseas advertising spending fluctuated significantly in Q4 2025. October’s spending was $244 million, surging to $386 million in November, while December’s spending, ending on the 26th, was only $174 million, with full-month spending projected to be between $175 million and $176 million. This decline was primarily due to reduced spending during the holiday season.

Regarding media channel allocation, Q4 2025 spending exhibited a clear hierarchy. Meta dominated with a total investment of $359 million, followed by Google with $20 million, while TikTok ranked third with $32.5 million. In its programmatic advertising platform strategy, Applovin became Temu’s core channel, with spending of approximately $22.8 million in Q4 2025.

Additionally, Temu advertises on Google’s DSP platform, Display & Video 360 (DV360), with monthly spending between $400,000 and $700,000, peaking at over $700,000 in November. Its main advertising channels are YouTube and Spotify.

There is a significant shift in regional resource allocation strategies. The North American market’s share rose from 30% in October to 39% in December, while the European market’s share decreased from 46% in October to 40% in December. Meanwhile, the Latin American share declined from 14% in October and November to 10% in December. Notably, North Africa, primarily Morocco, saw its share increase from 2% in October to 5% in December due to the promotion of the Africa Cup of Nations.

From an operational perspective, fully managed creative content accounted for 50% to 60%, while semi-managed content accounted for approximately 40%. Temu Ads merchant-run campaigns primarily utilise fully managed methods, contributing 30% to 40% to Temu Ads’ overall promotion.

Temu’s advertising strategy primarily falls into two categories: performance advertising and brand promotion. Performance advertising adheres strictly to ROI evaluation standards, covering platforms like Google, Meta, and TikTok, as well as other platforms such as Applovin and Unity. Regarding ROI, the evaluation criteria for Q4 2025 were very stringent. The 30-day overall ROI target for North America was set at 40%, with actual achievement rates around 42%-43%. The requirement for first-tier regions in Europe is 40%-41%, while second- and third-tier regions need to reach approximately 44%. Latin America has the highest standard, requiring 47%, while Africa is relatively more lenient, set between 38%-40%.

Meanwhile, the ROI evaluation standards for brand promotion campaigns are relatively lenient, typically 5 to 10 percentage points lower than those for performance advertising. This is mainly because brand advertising may lack information regarding data tracking and performance attribution. From an overall ROI evaluation perspective, the requirement is a combined ROI of 40% or higher over 30 days. This standard applies to all regions except new markets such as North Africa. It’s important to note that increased ad spend is only considered after ensuring ROI data meets the standards. This differentiated evaluation standard directly impacts Temu's marketing budget allocation and ad placement strategy.

Temu saw its 30-day ROAS (Return on Advertising Spend) in the European tier-1 market increase from approximately 40% to the 40%-50% range after implementing Google Campaign Manager 360 (CM360) at the end of May. During the 2025 Black Friday promotion, overall ROAS increased by 7.44% compared to the same period in 2024.

Looking at customer acquisition costs, the cost to acquire a new user in North America is between $45 and $50, while the cost to acquire a returning customer is $13 to $15. In first-tier European regions, the cost to acquire a new user is approximately $50 or higher, while the cost to retain a returning customer is between $14 and $15. In other regions, the cost to acquire a new user is between $30 and $35, while the cost of a returning customer is between $8 and $12.

In 2025, Temu’s initial bidding budget was $4.2 billion, while the target budget for the Meta platform was $2 billion. However, the actual total spending for the year was only $1.83 billion, with $1.02 billion spent on the Meta platform, achieving only 50% of the planned target. The underperformance in 2025 was primarily due to changes in US tariff policy, which led to a complete halt to all advertising activities in the US market during May and June. Simultaneously, the overall advertising strategy became more conservative, a stark contrast to the aggressive spending approach of 2024. Notably, Temu Ads’ bonus promotion played a crucial role in advertising spending in 2025. Without this promotion, the actual spending for the year might have been only one-third of the planned amount.

While both Europe and Latin America maintain similar levels of marketing expenditure at 12-15% of sales revenue, fundamental differences exist in their operational priorities and market strategies. This year, Europe’s primary task is compliance, including adapting to the IOSS reporting system and responding to new tariff policies. Furthermore, price manipulation issues in Germany and product compliance in France have also garnered significant attention. Despite these challenges, marketing investment in Europe remains between 13-15% of sales revenue, demonstrating a strong intention to expand the market.

In contrast, Latin America’s main focus is on optimising its logistics system, particularly by establishing local warehouses and improving last-mile delivery services in Brazil. Mexico’s warehousing network is relatively well-developed, but local warehouse construction in Brazil is still underway. Latin America’s marketing expenditure, at 12-15% of sales revenue, is primarily aimed at increasing penetration among new customers. These differences reflect the different stages of development and market environments in the two regions: Europe places greater emphasis on compliance and standardised operations, while Latin America focuses on infrastructure development and market penetration.

Temu vs Shein Advertising Strategy

Shein and Temu employ drastically different advertising strategies on Google’s advertising platform. Shein allocates over 80% of its budget to search advertising and rigorously controls ad placement across PC, mobile, and TV platforms via platforms like DV360. In contrast, Temu relies on PerformanceMax, an automated Google Ads campaign type that uses AI to place ads across all Google channels (Search, YouTube, Display, Gmail, Maps, Discover), with minimal intervention in ad placement. From a channel allocation perspective, Shein employs a diversified, decentralised strategy, integrating resources from various channels such as DSPs and programmatic ad networks, while Temu focuses on major mainstream media platforms.

Temu’s advertising strategy is mainly direct promotion, with over 70% of its content focusing on promoting a single product, including special offers or usage scenarios; approximately 20% showcases product bundle marketing, such as recommending various power banks; and the remaining 10% is used for marketing activities such as introducing app features, unboxing demonstrations, or social sharing. Although the specific products they promoted differ, both Shein and Temu adopted a product-centric advertising strategy during peak promotional seasons, tending to promote best-selling items or competitively priced products, with highly similar creative formats.

From a product-linking perspective, Shein and Temu have almost no overlap in their product placements. Shein has clear requirements for merchants, stipulating that products sold on other e-commerce platforms, such as Amazon and AliExpress, must use independent product links. In terms of advertising creative formats, the two platforms are highly similar. During the 2025 Black Friday promotion, over 40% of Shein’s marketing content used price comparison ads, displaying the original price and discounted price; another 40% focused on product feature demonstrations or category marketing using usage scenarios; and the remaining 15%-20% covered user experience-related content such as unboxing experiences, customer support, and logistics.

Shein employs a highly centralised authority structure in its team management, with core decisions controlled by a small group of key personnel. Its team leader is a seasoned veteran in Google Ads optimisation, leading to precise operational strategies. In contrast, Temu uses a flatter organisational structure, with country managers and campaign leaders having greater autonomy in decision-making. Notably, Temu excels in its collaborations with major media platforms, securing exclusive support for Meta’s AdvantagePlus feature and AppLovin algorithm – a unique advantage unavailable to other e-commerce competitors.

Logistics

In the cross-border e-commerce industry chain, supply chain management and logistics distribution systems demonstrate the strongest innovation vitality and market development potential. Emerging companies can choose to entrust the entire fulfilment process to a single freight forwarding company to reduce operational risks, while giants like Temu and Shein tend to adopt a segmented cooperation model to strengthen logistics control.

For cross-border e-commerce startups, it is recommended to entrust the entire logistics process from China to the target country to a single freight forwarding company, including transportation from the shipping warehouse to the airport, trunk line transportation, customs clearance, and final delivery. In contrast, large cross-border e-commerce companies like Temu and Shein optimise their logistics chain management through segmented contracting strategies, including domestic transportation in China, trunk-line transportation, customs clearance, and last-mile delivery services in the target country.

Temu has partnered with smart warehouses to optimise and upgrade its dynamic warehouse location management system. For example, when a warehouse has 1 million storage locations, after 200,000 items are shipped, the system automatically reclaims and releases the corresponding space. Warehouse scale, inventory turnover efficiency, and logistics timeliness all impact merchants and the platform. In Temu’s warehousing system, 85%-90% of warehouses are operated by third-party partners; these are considered strategic partner warehouses.

Temu prefers to avoid heavy asset investments, thus deciding against large-scale self-built logistics operations and opting instead for in-depth cooperation with Chinese logistics companies such as J&T Express and Wanyitong. This cooperation model involves outsourcing 80% of orders in a specific region to the logistics partner and reaching long-term warehouse usage agreements. However, in specific regions like South Korea and Poland, the company may build some logistics facilities itself.

By November 2025, Temu owned 14 warehouses globally, with a 15th planned for Ho Chi Minh City, Vietnam, demonstrating its strategic plan to develop in both Latin America and Southeast Asia simultaneously. Temu has already established its 14th logistics centre in Brazil, laying the foundation to cover the entire Latin American region, including Chile, Colombia, and Argentina. Similarly, its European logistics network is centred around Hamburg Airport in Germany.

Strategically, Temu operates three major transit trade hubs in Southeast Asia and Latin America: Vietnam handles Southeast Asia, Mexico covers Latin America, and Canada provides supplementary support. These hubs have effectively driven market growth. However, logistics infrastructure in Latin America is relatively underdeveloped. While Temu mitigates cargo and financial risk through its pan-Latin American logistics hub in Brazil, operating costs remain high.

Behind the excellent performance in Japan and South Korea, the advantage of logistics costs has played a crucial role. Due to the active entry of many Chinese logistics companies into the Japanese and South Korean markets, price competition has intensified, allowing Temu to enjoy lower delivery fees in these two markets. In contrast, in the US and European markets, last-mile delivery costs are as high as over €3 per order, respectively, a significant cost difference.

Taking the Japanese market as an example, the service prices offered by Chinese logistics companies such as ESP are significantly lower than those of local logistics companies such as Yamato, Sagawa Express, Japan Post, and Yamato Express. In addition, in South Korea, Temu has further optimised its cost structure through strategic partnerships, collaborating with Lotte to build a logistics transfer centre in Gyeonggi Province, which includes a 9-story above-ground building and a 2-story underground structure, thereby effectively reducing warehousing and transportation costs.

Europe

Europe has a clear advantage in logistics. Geographical proximity among countries allows for efficient delivery via a pan-European network, and market strategies are relatively stable and reliable. Temu has a more comprehensive strategic footprint in Europe, having established self-operated warehousing facilities in the UK, Germany, France, Italy, Spain, Poland, and the Netherlands, and has formed strategic partnerships with local logistics companies such as FedEx and DHL. Temu has established a warehousing centre in Germany, allowing orders to be shipped directly from Germany to Switzerland or Luxembourg, eliminating the need for shipping from China. This operating model not only improves efficiency but also reduces costs.

Currently, Temu’s expansion in Europe is not yet large-scale; it focuses primarily on building its own warehousing and logistics infrastructure, especially optimising last-mile delivery. A quarter of Temu’s last-mile orders are completed through PUDO (pickup points) and Locker (self-pickup lockers). Users choosing self-pickup can reduce per-order logistics costs from $3 to $2, saving approximately one-third.

Temu employs a stockpiling strategy: when the daily order value exceeds $1,000, it prepares goods in advance via sea freight or the China-Europe Railway Express to reduce logistics costs. However, this strategy also carries risks: if turnover is less than 7 days, the goods may need to be destroyed or shipped back to China.

Currently, in the European market, 85% of orders are fulfilled via air freight, while 15% are handled locally under a semi-managed model. Since Europe still has a tax exemption policy for parcels under €150, and the company’s average order value is $47 [note: another expert claimed this was $38], it has not been affected so far. However, given the potential elimination of the tax exemption policy in 2026, the company plans to utilise the China-Europe Railway Express for transportation and establish local warehousing facilities in Poland and Belgium to better serve the European market. If the European market implements tariff policies in the future, the proportion of air freight will decrease significantly.

The cost-effectiveness assessment of transporting inventory to Europe in advance via the China-Europe Railway Express needs to be analysed from several dimensions. First, from an industry-impact perspective, the apparel and pet supplies sectors may be significantly affected because the EU has a significant local production capacity in the textile industry. However, it is worth noting that the apparel category accounts for less than 20% of Temu’s overall business, so the overall loss is manageable.

USA

In US operations, front-end transportation primarily relies on sea freight. Container shipping typically takes 1 to 2 months, while express shipping takes 30 to 35 days. In contrast, European logistics mainly rely on air freight. Products are shipped from Guangzhou’s warehousing centre in China, transported to their destination via third-party service providers like YunTu or chartered flights by China Eastern and China Southern Airlines. Last-mile delivery is handled by local service providers, with an overall transit time of approximately 7 days.

Before the US policy adjustment on May 2, 2025 (cancellation of de minimis), companies relied on air freight for about 85% of their products; after the policy change, the share of air freight fell to 2%, with the remaining products transported by sea. This shift made the operating model more similar to that of Amazon merchants. Currently, air freight is mainly used for high-value products, such as tablets and commercial drones, to reduce inventory turnover risk; while low-priced products such as data cables and charging heads rely almost entirely on sea freight.

While the US’s elimination of the $800 tax exemption increased consumer purchasing costs, the overall market price level also rose, but consumer demand did not decrease significantly; the impact on businesses was relatively small. After the policy change, companies no longer used the T86 customs clearance model (de minimis) and switched to the T01 and T10 general trade models, paying tariffs like other importers (see Temu Watch #9 for a detailed explanation of T86, T01, and T10). To cope with this change, the company analysed sales data for forecasting, shipped goods to overseas warehouses in advance, and maintained inventory turnover in US warehouses at 15-20 days. However, inaccurate forecasts led to unsold products, prompting the company to request price reductions from suppliers to avoid high labour and warehousing costs.

Temu is currently employing three clearance methods: first, a B2C cross-border small parcel model; second, the BBC model, which consolidates small packages in China into larger packages for shipment to the US; and third, a B2B model, which converts small SKU-based packages in China into larger packages for shipment to the US. In practice, Temu collaborates with third-party logistics companies. In T01 and T11 operations, customs primarily reviews the HS Code (Harmonised System code; a standardised 6-digit numerical method used worldwide by customs authorities to classify traded products) and the declared value of the large packages.

It’s worth noting that the declared amount is adjusted; for example, a $1,000 large package can be declared as $700 or $800, as the current inspection rate for Chinese cross-border e-commerce is relatively low. If taxes increase significantly in the future, Temu has also prepared a contingency plan by pushing the Y2 model. Under this model, merchants are responsible for customs clearance along the main route from China to the US and can obtain tax reductions through various channels.

For a parcel shipped from China with an order value of approximately $30, the logistics cost structure is as follows: domestic segment costs (from the merchant’s warehouse to the airport and air transport) account for 30-35%; customs clearance and related taxes account for 40-45%; and last-mile delivery costs within the United States account for 25-30%.

Returns

Returns are rare among Temu consumers, with a current return rate of approximately 3%. This is mainly because the prices of goods are relatively low, and consumers generally feel that the return process is not worthwhile. Even for clothing, the return rate in the US is only 15%, 5% to 6% lower than in the Chinese market.

Regarding the cost structure of returns, the final shipping cost is borne by the consumer. When consumers insist on returning items, platforms often choose to give the item away directly, further reducing the actual return rate. This approach not only reduces operating costs but also improves customer satisfaction.

Data & Payment Infrastructure

Temu has expanded rapidly in recent years, generating substantial demand for data centre providers, some of which is met through overseas cloud computing services. While Pinduoduo’s international business may have initially relied on third-party data centre services, some of its needs have shifted to Alibaba Cloud and Tencent Cloud. This reflects the increasingly close cooperation between internet companies and cloud computing service providers amid globalisation, which has positively impacted the business growth of companies in related industry chains.

Furthermore, the company’s international payment business is handled through third-party platforms, primarily PayPal and Google Pay, with payment gateway fees of around 1.6%.

Temu Watch #13 is available on China Digital Retail Report. It examines Temu’s adjusted pricing strategy, developments in competition and Temu’s GMV and profitability status. It also takes a close look at what to expect from the platform in 2026.

Key Takeaways

Global Market Presence: Temu has achieved a 24% share of last-order share in cross-border e-commerce purchases globally, on par with Amazon, and ranks third among global e-commerce apps by monthly active users.

Regional Revenue Drivers: Europe is currently Temu’s largest revenue source, accounting for 40% of its 2025 merchandise volume, followed by the United States at approximately 30-32%.

Strategic Shift in Operational Models: The platform is moving away from a purely “fully managed” approach toward “semi-managed” models, which now account for 75% of its US business, to help mitigate the impact of losing tariff exemptions.

Dominance in Brazil: In a significant shift for the Latin American market, Temu’s traffic surpassed that of MercadoLibre in December 2025, making it the most-visited e-commerce platform in Brazil.

Adaptation to European Tax Reforms: To prepare for potential 2026 policy changes, Temu launched the Y2 operating model in Europe, which shifts tax and customs responsibilities to sellers to ensure a smooth transition.

Merchant Profitability and Churn: Merchant margins are under significant pressure, often dropping to 3-5% for fully managed products due to platform algorithms, contributing to high merchant churn and dissatisfaction with Temu’s pricing control.

AI-Driven Advertising Strategy: Unlike competitors like Shein, who use manual search strategies, Temu relies heavily on Google’s AI-powered PerformanceMax for automated ad placement across all channels.

Logistics Cost Reduction: To counter rising air freight costs and tariff changes, Temu is increasingly shifting toward sea freight and the China-Europe Railway Express, while establishing “hubs” in Vietnam, Mexico, and Canada.

Customer Acquisition Costs: Acquiring a new user in North America or Europe costs $50, while retaining a returning customer costs significantly less at $15.

Exceptionally Low Return Rates: The platform maintains a low return rate of approximately 3%, largely because low product prices make the return process feel “not worthwhile” for many consumers.

For future editions of the Temu Watch series, please subscribe to China Digital Retail Report.

Sources

The information in this report is compiled from exclusive expert interviews within the Six Degrees Intelligence network, augmented with information from the sources below.

[1] 2026-01-13 IPC [2] 2026-01-05 Chinesellers [3] 2026-01-19 Chinesellers

Images by Ed Sander, unless stated otherwise. These images may not be reproduced without prior consent.