Keeta, Meituan’s overseas expansion - Part 2: Battle for Brazil … and the world?

How Meituan met a familiar competitor and battles a giant in Brazil.

Content

Things that caught our attention

The short video drama market has overtaken the cinema market.

How a Chinese mapping app, Amap, brings trust and sees user numbers explode

The top 14 AI universities for 2025 are all Chinese institutions.

Why does China care so much about ‘zero emissions’? (by Rui Ma)

Introduction

Earlier this month, we examined how Meituan selected markets and launched its international food delivery brand Keeta in Hong Kong and the Middle East. In this second of two reports on Meituan’s global moves, we take a closer look at its launch in Brazil, developments in profitability, and the outlook for Meituan’s globalisation.

These two reports are compiled from seven interviews with experts close to relevant companies during July to November 2025, as well as reports in the Chinese tech media over the past three years that chronologically outline the development of Meituan’s overseas business.

Because this report continues the paid section of the first report, it is available only to paid subscribers. Become a paying subscriber to unlock the full report and support our in-depth research into key China tech trends.

Ed Sander, Tech Research Analyst

Picking a market in Latin America

After Hong Kong, Meituan expanded its Keeta brand, which offers food delivery, to more than 20 cities in Saudi Arabia, as well as to Qatar, Kuwait, Dubai, and Abu Dhabi. Next, it set its eyes on Latin America. Two markets are usually prioritised in such expansions: Mexico and Brazil.

The outlook for Brazil’s food delivery market remains positive, although the total market value in 2024 is projected at $18.6 billion, down from the previously predicted $28 billion. It is projected to grow to $21 billion by 2026. Euromonitor International reported even higher numbers. From 2019 to 2023, Brazil’s food delivery market grew by 50.8%, reaching a total size of 139 billion Reais (~$25.5 billion) and an annual growth rate of about 15%-20%, which is much higher than the global average. [1]

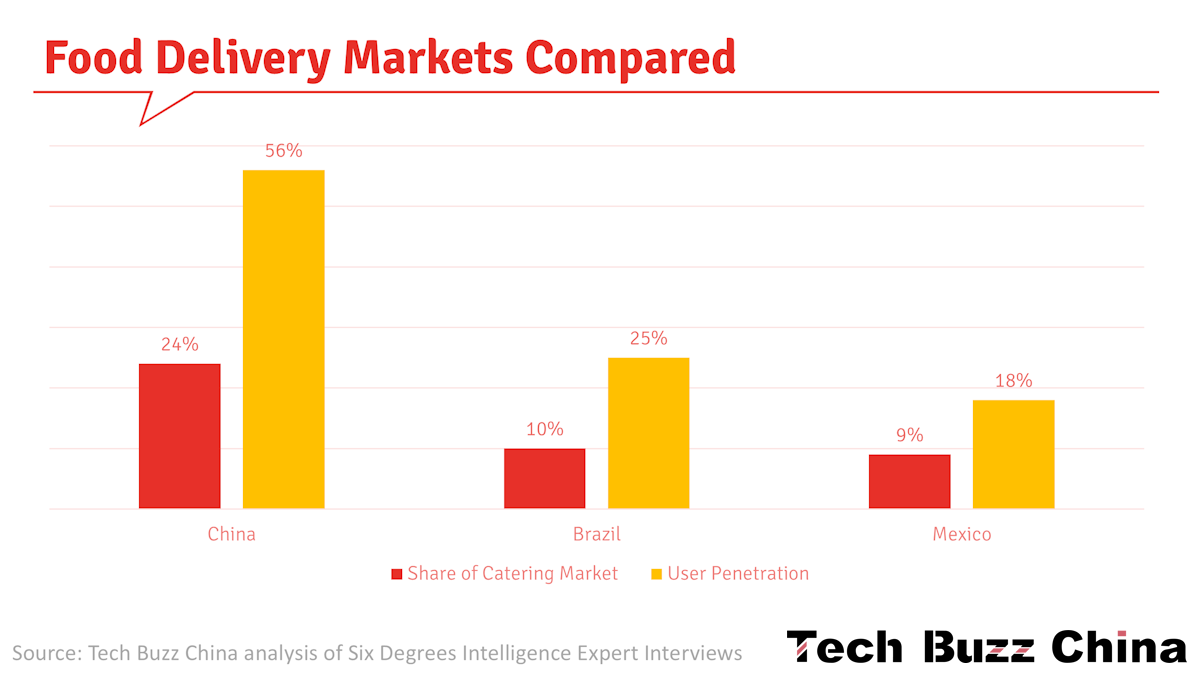

Brazil has over 200 million people, 90% of whom have internet access, demonstrating a high level of digitalisation. Currently, about a quarter of Brazilians use food delivery services. Based on the total number of internet users, the share who have used food delivery services is between 22% and 25%, compared with over 50% in China. Ordering frequency is relatively low. This indicates significant room for market growth, particularly by increasing the frequency of user orders. As the market continues to develop and mature, we may see greater innovation and competition, which will help drive the industry's growth.

Another potential in the Brazilian market is its high urbanisation rate, which exceeds 85%. Large cities such as São Paulo and Rio de Janeiro have a population of tens of millions. [1]

By transaction value, Brazil’s food delivery market penetration is approximately 9%-10%. Brazil’s food delivery market is growing at 15%-16% annually and is expected to accelerate to 22%-25% in the future. This growth is likely to be driven by new entrants such as Keeta and 99Food. Market leader iFood holds an 80-90% market share and has 55 million users, and its business is primarily concentrated in first- and second-tier cities. In contrast, the market in second- and third-tier cities remains largely untapped, providing opportunities for new entrants. Even if new entrants initially achieve only a 5%-6% market share, the market size could reach $30 billion, and a 1%-2% net profit margin could generate substantial profits.

Brazilian consumers haven’t fully adopted food delivery, primarily due to high prices. Price wars and subsidies, as seen in Hong Kong and Saudi Arabia, can gradually shape consumer habits, especially in categories such as single meals, coffee, fried chicken, hamburgers, barbecue, and tacos.

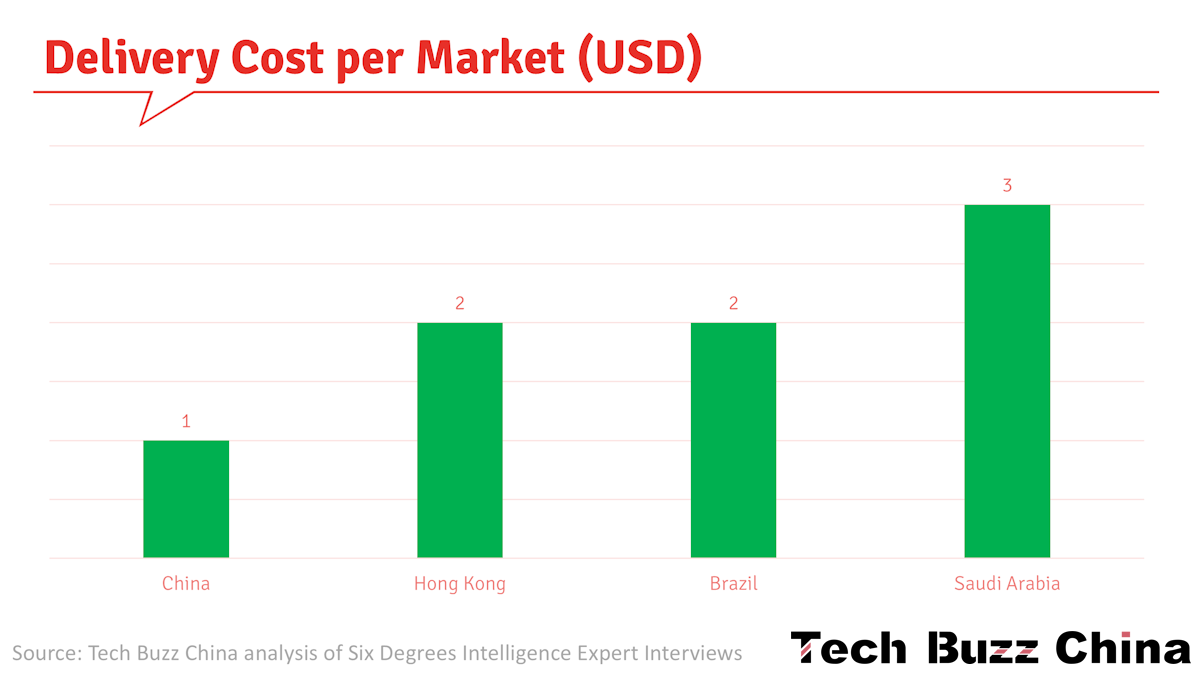

In terms of payment methods, Brazilian consumers prefer cash and instalment payments, with mobile payment penetration lower than in China. Food delivery services are mainly used for family meals, with the average order on the iFood platform costing approximately $10. Compared to China, delivery fees in Brazil are higher. For example, a $7 order might incur a $2 delivery fee, which discourages single individuals and couples. Delivery fees for smaller orders, such as drinks, can even reach $3, further limiting food delivery usage. These factors significantly impact the development prospects and business models of Brazil’s food delivery industry.

Mexico’s food delivery market penetration rates, measured by transaction value and population, are 9% and 18%, respectively, similar to Brazil’s, but the market size is smaller. Mexico’s food delivery market is primarily controlled by the Chinese local services giant Didi, particularly its delivery service, which relies heavily on electric vehicles. This market is significantly influenced by religion and culture, resulting in a relatively simple structure. However, due to underdeveloped infrastructure, Mexico’s food delivery industry faces bottlenecks and relies primarily on ride-hailing vehicles and motorcycles. Despite Brazil’s higher mobile internet penetration, food delivery usage remains low, largely due to limited coverage in major cities and entrenched consumer habits.

Brazil’s food delivery market has a brighter future than Mexico’s, primarily due to Brazil’s larger economy, population, and market size. The development trajectory of Brazil’s food delivery industry mirrors China’s early model, starting in large cities and gradually expanding to smaller towns.

Keeta Goes Brazil

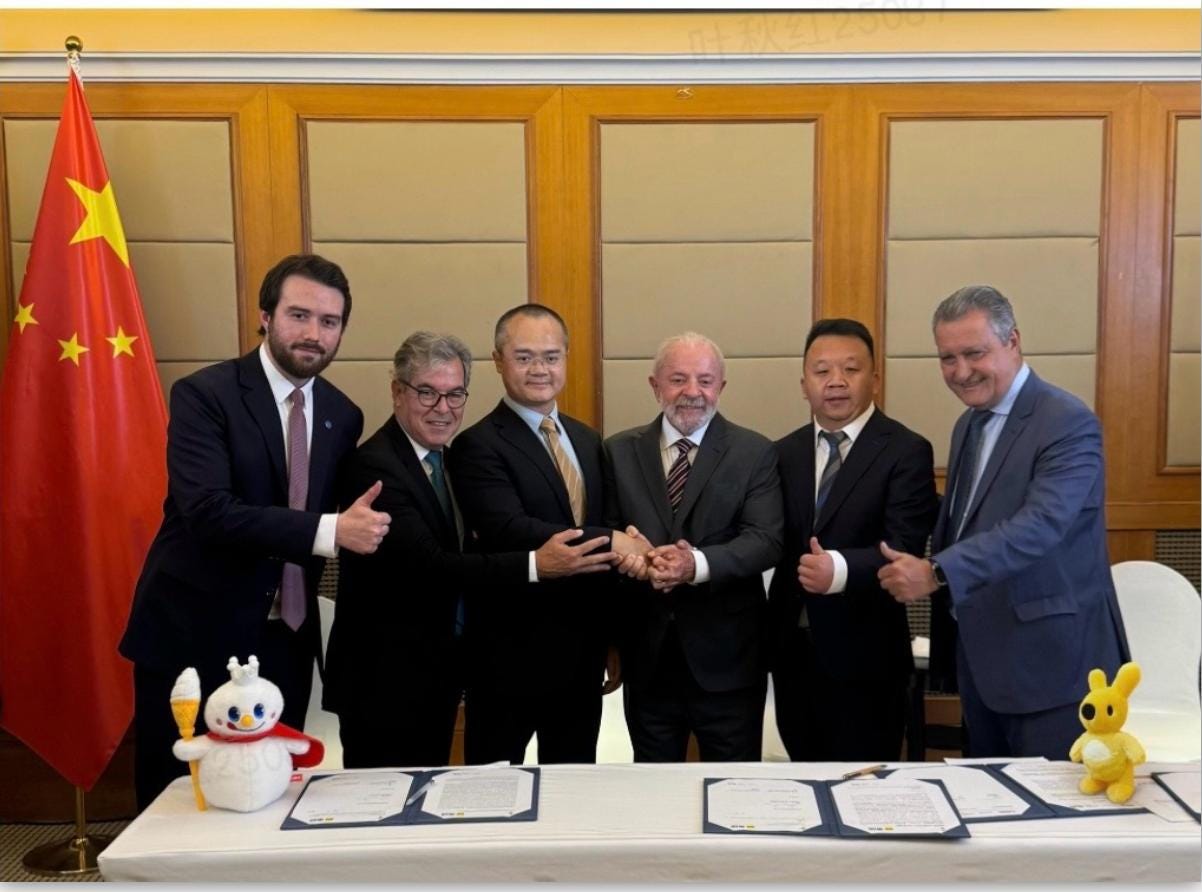

In May, Brazilian President Lula signed several deals during a visit to China, including a five-year $1 billion commercial agreement with Wang Xing, the co-founder and chief executive of Meituan. [2] This investment would help Keeta develop digital tools (Keeta would offer local food merchants a variety of marketing tools and digital operation solutions to support their business growth), allocate marketing resources, build a logistics network with over 100,000 riders, open a customer service centre, and hire more than 1,000 local employees, CEO Chou Guangyu said. Keeta will focus on food delivery for now and may consider entering fresh grocery and pharmaceutical e-commerce in the future. Still, it will not enter the ride-hailing business, Chou noted, adding that it is expected to be available in 15 metropolitan areas by June next year and to cover 1,000 major cities within five years. [3] [4]

Wang Xing and Brazil’s president Lula (centre). Also, second from the right: Sun Zexu, a key Mixue executive. [5]

In mid-2025, Keeta primarily conducted market research and executed signing activities in major cities, including São Paulo. Meituan’s strategy is to first partner with global chain merchants to break market leader iFood‘s exclusive agreements (see ‘Competition’) and then gradually expand its business to surrounding cities. Meituan conducted trial operations in Brazil at the end of August 2025. During the trial phase, it planned to sign contracts with approximately 1,000 merchants and recruit at least 500 delivery riders.

On October 30th, Keeta officially launched its operations in Brazil, starting in Santos and São Vicente, São Paulo. Initially, things didn’t go smoothly. In the first week, local delivery drivers collectively demanded that the platform increase delivery fees, and restaurants also accused the platform of unfair competition. [6] Edgar da Silva, president for AMABR, a union group for delivery workers in Brazil, told Rest of World: “In the beginning, they will be paying well, so they can gain [the trust of] delivery workers. But as the market stabilises, Meituan will become just like the others. There will be no difference but in who exploits us more.”

During its first year of operations in Brazil, Meituan expects to hire 1,000 workers, up to 4,000 call centre operators, and 100,000 delivery personnel. [2]

As of November 20, Keeta had 4,700 registered delivery riders and 1,600 partner restaurants in the São Paulo area. On November 26 2025, Keeta held a launch event in Brazil, releasing data from its initial pilot program and announcing that it would launch its food delivery service in São Paulo, Brazil’s largest city, and eight surrounding cities starting December 1. Of the originally planned investment of 5.6 billion Reais ($1 billion), 1 billion Reais will be used for business expansion in the region. [6]

On December 1st, Keeta officially launched in São Paulo, Brazil’s largest city, with billboards ubiquitous across the city. Keeta offered attractive incentives: a 200 Reais ($27) discount coupon for new users, a promise of free delivery from 90% of partner restaurants, and real-time tracking of delivery progress for 90% of orders. [6] Keeta also stated that it plans to enter the Rio de Janeiro metropolitan area within weeks, marking its official entry into Brazil's competitive instant commerce market. [7]

By the end of 2025, Keeta’s service in the Brazilian market would cover 39 cities in the São Paulo metropolitan area and their surrounding satellite cities. Following this, the plan for 2026 is to expand to 15 major metropolitan areas, including important cities such as São Paulo, Rio de Janeiro, and Belo Horizonte, with a target of covering 100 cities. These key cities account for over 55% of the Brazilian food delivery market, and are thus considered strategic core areas.

However, iFood dominates the Brazilian food delivery market. Leveraging its first-mover advantage, it has built competitive barriers in several areas, including 400,000 merchants, 4 million daily orders (80% of the industry’s 5 million orders), 50 million active users, and 300,000 delivery personnel. Looking further, ifood’s service network covers 1,500 cities, and despite charging a high 27% fee, delivery times are long, typically 35 to 40 minutes.

Notably, Meituan’s strategy in Brazil mirrors its approach in Hong Kong and Saudi Arabia, including attracting new users through large coupons. To counter iFood's competition, Keeta entered the market through a price-war strategy. In the short term, they will attract merchants with zero commissions, rapidly accumulate supply-side resources, and use subsidies to compete for users, aiming for a 10% market share. Its medium-term goal is to optimise delivery times to approximately 25 minutes and help merchants manage their businesses through a SaaS system, thereby establishing a long-term competitive advantage.

In the long term, the strategic focus is on improving delivery efficiency, refining the algorithmic scheduling system, and helping merchants manage their businesses through a SaaS platform, building a competitive advantage from a technological perspective. Furthermore, Keeta also intends to improve delivery rider efficiency through instant retail, utilising their downtime to further enhance its market competitiveness.

Keeta plans to achieve a 30% market share within three years, jointly dominating the market with iFood and forming a duopoly. Meanwhile, Brazilian authorities are implementing antitrust policies to create a level playing field and attract more companies to invest in infrastructure. These policies will influence the investment decisions of Meituan and other companies in Brazil, prompting them to be more cautious and compliant in formulating their investment strategies.

Source: Keeta LinkedIn

Brazil is the most attractive large market in Latin America. Still, Meituan has to compete with the local iFood and the Chinese company Didi, which had announced its entry in April 2025. [8] iFood has been nearly unchallenged since 2023, when both Uber Eats and 99Food halted operations in Brazil after struggling against iFood’s dominance. [2]

In addition to intense competition, Keeta (and Didi, see below) faces several challenges in Brazil. [1]

Delivery costs for takeaway orders in Brazil can account for up to 30% of the order amount, higher than the global average.

Although there are self-built financial tools, the online payment ecosystem in Latin America is relatively complex. There are three types of payment: cash, instalment, and instant. Among them, instalment payments, which carry financial risks, account for 58% and pose challenges for the company’s overseas financial operations.

Brazil’s macroeconomic situation, where inflation is still considerable (4.46% in November 2025). Relevant data show that commodity price pressures primarily come from food and beverage prices and transportation costs. Price increases for these everyday consumer goods are likely to affect users’ purchasing decisions, which in turn introduces uncertainty for online shopping.

In recent years, Brazil’s social environment has generally been stable, but there remain risks in some local areas. For example, during sensitive periods such as elections, conflicts and contradictions may break out between different political camps.

Competition: Didi (99Food)

Before we look at market leader iFood, let’s first look at Meituan’s compatriot, Didi, which has recently made its second food delivery entry into Brazil.

Didi started its global expansion in 2017. As of 2024, Didi’s international business operates in 14 countries across Latin America, Asia-Pacific, and Africa, including 10 Latin American countries such as Brazil, Mexico, Chile, and Colombia. Among them, Didi has opened a food delivery business in 4 countries, including Mexico, Colombia, Costa Rica and Peru. [1] In Q3 2024, Didi’s international business exceeded the milestone of 10 million orders daily, amongst which 95% came from ride-hailing, and 90% came from Latin America. That is equivalent to about 1/3 of Didi’s order volume in China. [9]

Specifically in Latin America, Didi acquired Brazil’s 99 in January 2018, launched ride‑hailing in Mexico in 2018, Chile, Colombia and Costa Rica in 2019. [5] Since Didi officially entered the Mexican market in 2018, it has covered the top three cities in Mexico and surrounding areas by early 2025, serving a population of more than 30 million. Mexico has been a success, contributing more than 300,000 orders a day by the end of 2024. Currently, Didi’s food delivery business in Mexico boasts 500,000 active riders, 90,000 active restaurants and more than 1.6 million active users. [1] [9]

According to a report released by Measurable AI, in the first quarter of 2023, Didi’s share of Mexico’s online car-hailing market was 56%, while Uber’s was 44%, surpassing Didi to become the number one player in Mexico. Since 2021, Didi’s international payment fintech business has made significant progress in Mexico, and its personal credit business has become the industry leader in Mexico and Latin America. Didi Food, a food delivery business launched in 2019, has expanded to more than 60 major cities in Mexico over the past five years, with a market share exceeding 50%. It is currently the largest food delivery platform in the local area. [1]

Didi’s diversified business model in Mexico has not only increased its market share but also provided valuable experience for its expansion into other Latin American countries, such as Brazil. By integrating online car-hailing, food delivery, and financial services, Didi has built a comprehensive service platform that meets the diverse needs of local users. [1]

In 2019, Didi entered Brazil's food delivery market with 99Food but failed to break iFood’s dominance. According to Paidai, iFood required local merchants to “choose one of two.” This unfair clause directly led to Didi’s 99Food and UberEats suspending their restaurant delivery services, one after another; 99Food ceased operations in April 2023. [1]

However, in April 2025, amid (and probably triggered by) rumours of Meituan’s arrival in Brazil, Didi announced the return of 99Food delivery services, along with $180 million in investment. The following month, iFood and Uber announced a partnership, which allows users to book Uber rides through iFood’s app and access food, grocery, and pharmacy items through the Uber app. The alliance was not timed to coincide with the entry of Chinese firms, a spokesperson for iFood told Rest of World. [2]

According to Momentum Works, there were three reasons Didi had not been ready during its first attempt with 99Food: [9]

It did not manage to build a fulfilment network in time to be prepared for the pandemic surge.

It did not have the organisational capabilities (including key executives) ready;

and it did not know how much investment to commit to this venture.

Source: 99Food

Things were different with its second attempt.

When Didi relaunched its food delivery service, it could leverage its existing 50 million passengers and 700,000 riders on the 99 platform, covering approximately 3,300 cities. According to data released by Didi, cumulative two-wheeler mobility orders in Brazil have surpassed 1 billion. This fulfilment network has also been used for grocery delivery and could be easily adapted for food delivery. [9] The 99 platform has amassed extensive resources and strong brand awareness. Although it stopped the restaurant takeaway business in 2023, it retained some supermarket delivery businesses. [1]

Didi has also built a large digital financial services business, starting with 99Card, a Mastercard debit card that enables drivers and riders to receive payments. Payment and other services targeting merchants and consumers are layered on top. When Didi first entered the Latin American market, local drivers still had to carry cash. The emergence of financial wallets changed the service process for online car-hailing in Brazil. Today, 99 Pay can not only top up cash and pay for taxi fares, but also add services such as paying utility bills and recharging phone bills. This can be a good lever in high-volume, low-margin local services such as food delivery. [9] [1]

As far as its team and organisation are concerned, Didi has come a long way in adapting to the Brazilian market. Most senior managers in Brazil are local rather than expat. [9]

Interestingly, Keeta is led by the same Tony Qiu (Qiu Guangyu) who previously led Didi’s expansion in Latin America. Qiu joined Meituan in 2022, after working at Didi and Kuaishou – both companies with strong footholds in Brazil. “He will not enter Brazil when he is not ready,” a former executive of Didi told Momentum Works. “But once he does decide to enter, it means he is ready”. Some investors they spoke to were a bit worried about Didi’s increased spending by launching food delivery in Brazil. However, they all agree that Didi was much more ready to deliver food than Meituan and needed to act soon before that time window closed. [9]

Didi’s years of operational experience in Brazil give it an advantage in capacity management and rider network, which could help reduce delivery costs. The delivery service can operate on a part-time model similar to ride-hailing, with riders handling various delivery tasks such as food, cakes, or flowers. In the initial stages, performance evaluation standards for part-time riders are relatively lenient, but generally sufficient to meet demand. However, Didi is weighing full-time versus part-time riders, as the latter may lead to capacity shortages as orders increase.

Notably, a quarter of Brazil’s 210 million population has used Didi‘s transportation services, providing a solid customer base for its food delivery business. Didi’s success in Mexico with ride-hailing (Didi Conductor) and food delivery (Didi Food) has instilled confidence in its expansion into Brazil. In Mexico, Didi's food delivery business already holds nearly half the market, demonstrating the viability of combining ride-hailing services with food delivery. Didi’s extensive operational experience in Mexico gave it a deeper understanding of the Latin American market, enabling it to identify and respond to industry leaders' strategic moves quickly.

Didi’s development strategy in the Brazilian food delivery market primarily focuses on food categories popular with local consumers, such as barbecue, burgers, and coffee. To attract more users, Didi has increased its marketing efforts, continuously optimised its rider system, and cleverly utilised rider resources to reduce operating costs. On the merchant side, Didi has adopted commission and rebate policies to attract more merchants to join the platform.

99Food is providing newly registered restaurants with zero-fee operations for the next two years, and offering a minimum of $45.85 per day for delivery workers who complete at least 15 orders or rides. In August 2025, iFood paid between $1.19 to $1.37 per delivery. [2] Didi also plans to implement a zero-commission policy for large merchants such as Starbucks by the end of the year, which will undoubtedly further enhance the platform’s attractiveness. In addition, Didi leverages its strengths by subsidising delivery fees to maintain its competitive advantage amid intense market competition. In mid-2025, due to substantial subsidies, Didi lost approximately $1.40 per food delivery order.

Chronologically, Didi entered the Rio de Janeiro market on October 30, 2025, having already conducted test operations in São Paulo earlier, employing an expansion strategy that combined major cities with surrounding areas. More importantly, Didi’s market expansion outpaced that of industry leaders due to its established logistics and delivery network. Particularly in securing key merchant resources, Didi successfully established close relationships with numerous large partners at the key account (KA) and small merchant (SKA) levels through significant investment. In the competitive landscape of the Rio de Janeiro market, Didi has taken the lead in establishing a presence and partnerships with numerous merchants, resulting in rapid expansion, but also significant operating losses.

Regarding differentiation in delivery models, Didi treats food delivery as a secondary business, and its operating model has some limitations. In most areas, it relies on part-time drivers for delivery, leading to insufficient capacity during peak hours. In terms of human resources, Didi had about 700,000 delivery riders, only tens of thousands of whom are full-time, providing on-demand delivery services by utilising drivers’ spare time. About 8% (about 60,000) of Didi’s drivers are motorcycle and car drivers. In the first half of 2025, Didi added about 10,000 full-time food delivery riders, bringing its total outside ride-hailing to about 80,000. Full-time riders complete an average of about 10 orders per day, while motorcycle riders complete an average of 2 to 3 orders per day.

In contrast, leading companies in the food delivery industry have built efficient, stable delivery networks using a mix of full-time and part-time crowdsourced riders, typically completing deliveries within 25 to 30 minutes. Keeta also employs a full-time delivery rider system, with a focus on delivery efficiency and service quality. While this model expands more slowly in the short term, it offers greater stability and efficiency in the long run. Keeta plans to leverage the efficiency and reliability of its full-time delivery system to stand in sharp contrast to Didi’s reliance on part-time drivers and expects to gradually gain dominance in the core food delivery market within the next two years, eliminating Didi as a major competitor.

In terms of market strategy, Didi has adopted a unique approach, primarily promoting its service in smaller cities while using larger cities as pilot areas. This strategy appears to be showing results. At the same time, Didi’s current market expansion strategy entails significant investment costs, raising concerns about its sustainability. In the Brazilian market, the food delivery industry's main strategies are concentrated in the two major cities, Rio de Janeiro and São Paulo, with Rio de Janeiro considered the primary competitive area. Notably, leading companies in the food delivery industry have chosen to focus on specific regions to avoid direct competition with Didi in the most competitive markets, thereby optimising resource allocation.

In second- and third-tier cities, Didi and Meituan can collaborate with leading brands in their respective market segments, such as Mixue Ice Cream, which is launching in Brazil. In first-tier cities, they can gradually break down barriers to partnerships with local chains through brand promotion and market expansion. Furthermore, the lower-tier markets that iFood has not yet penetrated present opportunities for Didi and Meituan to expand. The combined application of these strategies will help reshape the competitive landscape among them and iFood, creating more opportunities for Didi and Meituan to develop in the Brazilian market.

Regarding order volume, Didi processes between 200,000 and 250,000 food delivery orders daily. In July 2025, 99Food’s daily order volume reached 260,000 to 270,000, with orders from the two major cities of São Paulo and Rio accounting for half. In mid-2025, the platform had between 60,000 and 70,000 partner merchants, indicating that Didi had established a substantial merchant network in a short period. These figures demonstrate Didi‘s rapid growth and potential in the Brazilian food delivery market.

While Didi's food delivery business in Brazil has performed well since its launch, it remains in the exploratory phase. Notably, Didi’s 99Food has already invested approximately $150 million (about 1 billion Reais) in infrastructure development. Looking ahead, Didi and Meituan can leverage their brand recognition in first-tier cities and their market coverage in lower-tier cities to gradually increase their market share.

Didi adopts a high-investment expansion strategy in the Brazilian market (especially Rio de Janeiro and São Paulo), while competitors choose to avoid direct competition and focus on fulfilment stability. Didi must develop an effective long-term competitive strategy amid challenges to customer loyalty and cost sustainability. In the long run, the key to success in the food delivery industry lies in the stability of fulfilment, not short-term price wars or subsidy strategies. Therefore, Didi may face challenges in maintaining customer loyalty.

In September 2025, Didi announced it would increase its investment in Brazil. 99 would invest 2 billion Reais ($188.1 million) in its food delivery platform 99Food by June 2025. It would also launch a 6 billion Reais support program to provide delivery drivers with funds to buy and lease electric motorcycles and bicycles. Furthermore, Didi’s founder and Chief Executive Officer, Cheng Wei, was reported to have met with Brazilian President Luiz Inácio Lula, along with other 99 executives. [3]

In the long term, Didi plans to develop 99Food into a multi-functional platform, similar to Grab, encompassing services such as payments, transportation, finance, food delivery, and retail. However, the company has not yet decided whether to include group-buying services.

Unlike Didi, Meituan is starting from scratch in the Brazilian market, not relying on its ride-hailing business as a foundation. When signing merchants, Meituan’s main objective is to challenge iFood’s market position, rather than deliberately avoiding competition with Didi. Although there are multiple competitors in the Brazilian market, Meituan’s main rival remains iFood.

Beyond their services, Didi and Meituan also bring the cutthroat competition of the Chinese market to Brazil. Ironically, Didi has tried food delivery and instant retail services in China both before and during COVID, but they were never very successful. Now it finds itself in the same battle abroad.

In August 2025, even before Keeta’s launch in Brazil, 99Food sued Keeta for trademark infringement related to its yellow colour scheme and fonts, as well as for unfair competition. Less than a week earlier, Meituan accused 99Food of subsidising merchants to stop them from working with Keeta. Meituan also sued 99Food for attempting to divert traffic from Google to Keeta by purchasing search terms related to the app. It won a small victory as a São Paulo court ordered 99Food to stop the practice within three days or face a daily fine. Failure to comply will incur a daily fine of 20,000 Reais ($3,640). [3] [10]

Source: Caixin [11]

Competition: iFood

Similar to Hong Kong and the Middle East, Brazil’s food delivery market also has its own “giant”: iFood holds an absolute advantage in market share, even exceeding Meituan’s former 70% share in China’s food delivery market. [6] In 2024, Brazil’s food delivery market reached approximately $18 billion, with iFood holding nearly 90% market share and generating roughly $16 billion in revenue. iFood’s net profit in 2024 was roughly $90 million. In contrast, competitor 99Food’s situation is less optimistic. 99Food incurs approximately $1.50 in losses per order and has a market share of around 10%. To break even, 99Food needs to increase its market share to approximately 30%, otherwise it will continue to lose $0.70 - $0.85 per order. This contrast highlights iFood’s strong market position.

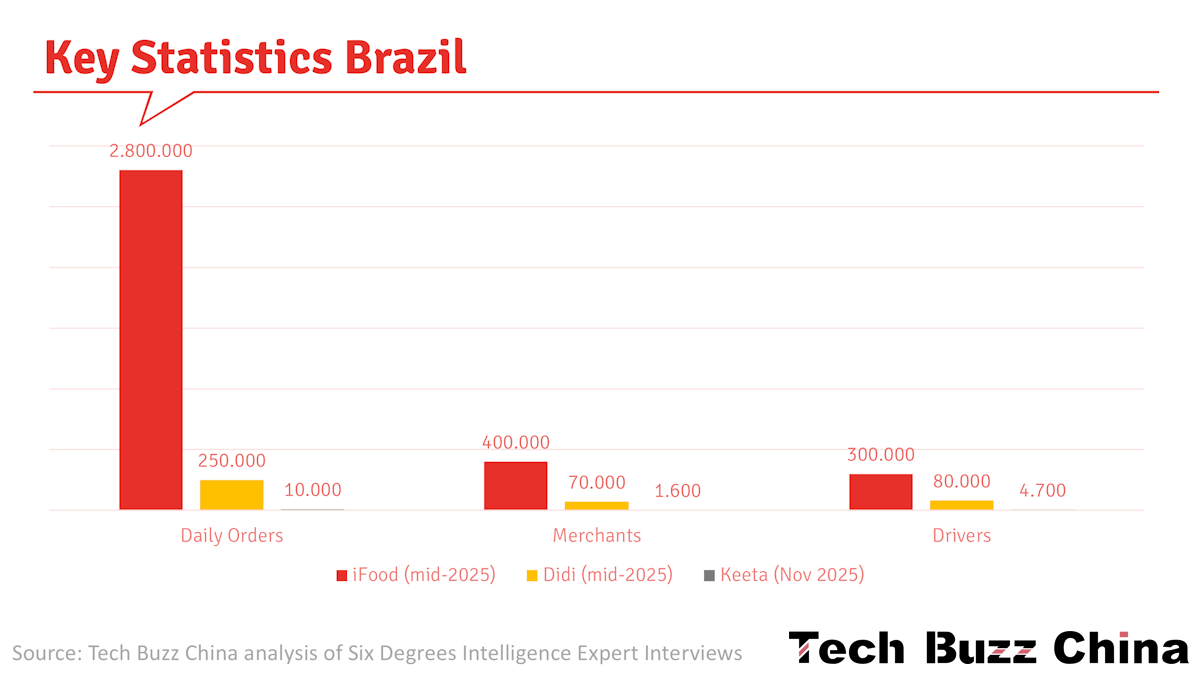

iFood handles approximately 2.8 million orders daily, while Didi’s only handles about one-tenth as many, and Meituan has only just launched. This gap reflects a significant difference in market share between the companies. Furthermore, iFood has established exclusive partnerships with many merchants, posing a considerable challenge for Didi and Meituan. iFood’s monetisation rate is between 25% and 26%, with an average order value of $10.

iFood’s primary revenue source is merchant commissions, with delivery services also contributing to its income. Delivery services may have higher profit margins due to lower subsidies. iFood, as an online food delivery platform, takes a 7% cut from each transaction, with 5% as commission and 2% for advertising. Delivery costs approximately 18% of the transaction amount. Assuming an average order value of $10, delivery revenue would be approximately $1.80-$2.30.

iFood handles 20% of iFood orders, while restaurants handle 80% of deliveries themselves. Due to iFood’s dominant market position, its delivery fees are relatively low. Riders earn about $1 per order, while the platform receives $2. However, this low delivery fee has caused dissatisfaction among some riders, even leading to strikes. iFood’s market dominance and subsidy-reduction strategy have created opportunities for competitors such as 99Food and Keeta.

In contrast, Didi’s average order value is $8, indicating a disadvantage in transaction value. In mid-2025, Didi was losing around $1.50 per order, primarily due to initial subsidies of over $2. Although Didi generated approximately $9.30 in revenue per order, it still could not achieve profitability after deducting subsidies. Didi, a leading ride-hailing company, charges a 6% fee in its food delivery business, comprising a 4% commission and a 2% advertising fee. For delivery, Didi uses a combination of motorcycles and cars, with delivery fees accounting for 16%-17% of the order value, or about $1.40 per order. Didi’s overall monetisation rate is between 23% and 24%, slightly lower than iFood's, but with lower revenue per order.

In comparison, Meituan’s profit per order is approximately $0.20, with a net profit margin of about 3%. iFood’s profitability exceeds Meituan’s, with a net profit margin of 3.5-4%, close to the industry’s highest level of 5%. To further improve its net profit margin, iFood may consider introducing a membership program and adjusting delivery fees to optimise its revenue structure. These measures are expected to help iFood maintain strong profitability in the highly competitive food delivery market.

iFood’s competitive advantages in Brazil include: its core leadership, who previously led Didi Brazil and possess extensive experience and resources; support from the local government, including flight support and a significant five-year investment commitment; and unmet user needs in the market.

Still, Keeta and 99Food pose a competitive threat to iFood, which could significantly alter the future market landscape. In this situation, if iFood cannot maintain its market leadership, it may need to increase discounts for merchants to counter competition. Furthermore, iFood may need to increase user subsidies to address market competition. The 99 platform cited Didi’s experience in the Mexican market in developing 99Food, which could pose even greater challenges for iFood.

Facing competitive pressure from Chinese companies entering Brazil's food delivery market, iFood has implemented a series of targeted measures to maintain its market position. First, it lowered its membership fee threshold, increased user subsidies, and raised rider subsidies in the short term. Specifically, by mid-2025, iFood provided riders with a subsidy of 2 to 3 Brazilian Reais (approximately $0.37 - $0.55) per order, a significant increase from the previous 1 Brazilian Reais. For customers, iFood increased subsidies from 1.5% (approximately $0.15) of the order amount (around $10) to approximately 3% (roughly $0.30). It’s worth noting that 99Food offers even greater subsidies. Didi offers new users a 12%-15% subsidy, while existing users receive 10%-12%.

Source: iFood

To further consolidate its market position, iFood partnered with its former competitor, Uber Eats, in 2025, gaining access to map services and ride-hailing data support, and launched promotional activities to attract users. The partnership between UberEats and iFood will likely trigger market volatility, primarily because UberEats, as Uber Group’s global platform, boasts a massive user base and strong market resilience. In developed cities, iFood’s partnership model appears more like a protective strategy, but its future development still hinges on supply chain expansion.

iFood’s current market situation is similar to Ele.me's in 2015-2016, including order composition and proportions. iFood is weighing whether to expand into second- and third-tier cities or continue focusing on first-tier cities. If the latter strategy is chosen, its primary target customers will be high-spending families dining together, hoping for high profits and quick returns. The collaboration between iFood and UberEats primarily manifests in their interaction, and its effectiveness depends on Uber and Didi’s coverage and market share in Brazil's ride-hailing market.

However, iFood’s primary task is to compete for market share with rivals, not to expand immediately. With limited resources, 99Food and Meituan are iFood's main competitors, so expansion should be approached with caution. It’s worth noting that iFood’s profitability relies heavily on its market size, market share, and management strategy, rather than on technology or delivery optimisation alone.

These measures will undoubtedly increase iFood’s operating costs, but are expected to help the company maintain or expand its market share. An industry expert recommended that Chinese companies planning to enter the Brazilian market begin in non-first-tier cities, gradually expand into the Brazilian food delivery market, and partner with international chain brands.

iFood could pose a threat to Didi and Meituan's expansion plans by securing exclusive restaurant partnerships. However, Brazil’s antitrust authority, CADE, reached an agreement with iFood prohibiting it from signing exclusive contracts with large restaurant chains, a move that benefits Didi and Meituan. Meanwhile, international chains like Starbucks and McDonald’s are generally not bound by iFood’s exclusive agreements and may therefore partner with Didi or Meituan. Didi and Meituan can circumvent iFood’s exclusive strategy by establishing partnerships with these global chains. Simultaneously, they can prioritise partnerships with local restaurant chains without exclusive restrictions.

Meituan and 99Food expect to gain market share from iFood by expanding their app offerings, including ride-hailing. They are likely to focus on recruiting small businesses that iFood has historically neglected because they cannot afford its high commissions. [2] Some Chinese companies that have operated in Brazil have found that iFood, now in a leading position, primarily serves high-income areas. Its coverage of small and medium-sized cities is insufficient. If Didi’s 99Food or Meituan’s Keeta want to overtake iFood, they must conduct differentiated operations, such as bypassing high-income areas and deepening their fresh food or night scenes. [1]

Leonel Paim, vice president of Abrasel, a trade organisation for bars and restaurants in Brazil, told Rest of World that Chinese companies see that “there’s still opportunity for growth in Brazil, which iFood cannot grasp.” While iFood is likely to maintain its lead in the short term, Chinese delivery companies, through massive investments, can transform the food delivery landscape over the next decade. Meituan “will develop and bring delivery services to a whole new level.” Competition from Chinese companies may prompt established players to offer better products and lower fees for restaurants, ultimately reducing delivery costs. [2]

Grocery delivery in Brazil?

While Brazil’s food delivery market totals around $20 billion, grocery and instant delivery services remain in their early stages, and the market is relatively small.

However, the Latin American on-demand FMCG delivery market is expanding rapidly, growing at approximately 15%-16% annually. Looking ahead, the industry is projected to grow 18%-20%, continuing its double-digit growth trend. This growth is driven by the region’s favourable demographics, large market size, and improving infrastructure. Notably, Latin American consumers are highly accepting of delivery fees, typically willing to pay between $1 to $2. This supports the industry’s profitability.

However, there is still significant room for improvement in fresh produce delivery and overall operational efficiency. Despite potentially large transaction amounts, the industry’s fundamental growth drivers remain strong. The long-term outlook for the Latin American on-demand delivery market for FMCG remains very promising. The sector faces significant opportunities but also challenges in achieving sustained growth. When assessing the Latin American FMCG on-demand delivery market, retailers need to carefully consider whether to enter the fresh produce business, given spoilage risks.

Zooming in, Brazil’s on-demand grocery retail industry is still in its developmental stage, with online transactions accounting for only 20%. Compared to the food delivery market, the on-demand retail market is relatively small, about one-fifth the size, about $4 billion. If online shopping platforms are included, the total value of the on-demand retail market could reach $7-8 billion.

In Brazil's grocery retail market, iFood is a major player, holding approximately 30% market share. iFood provides convenient services through partnerships with offline supermarkets and convenience stores, including GPA Group and Carrefour, resulting in significant sales volume. The fresh food industry requires considerable investment to build supply chains and warehousing facilities. To ensure profitability in the fresh food business, the gross profit margin on overseas goods must exceed 35%. These factors constitute challenges facing the on-demand grocery retail industry.

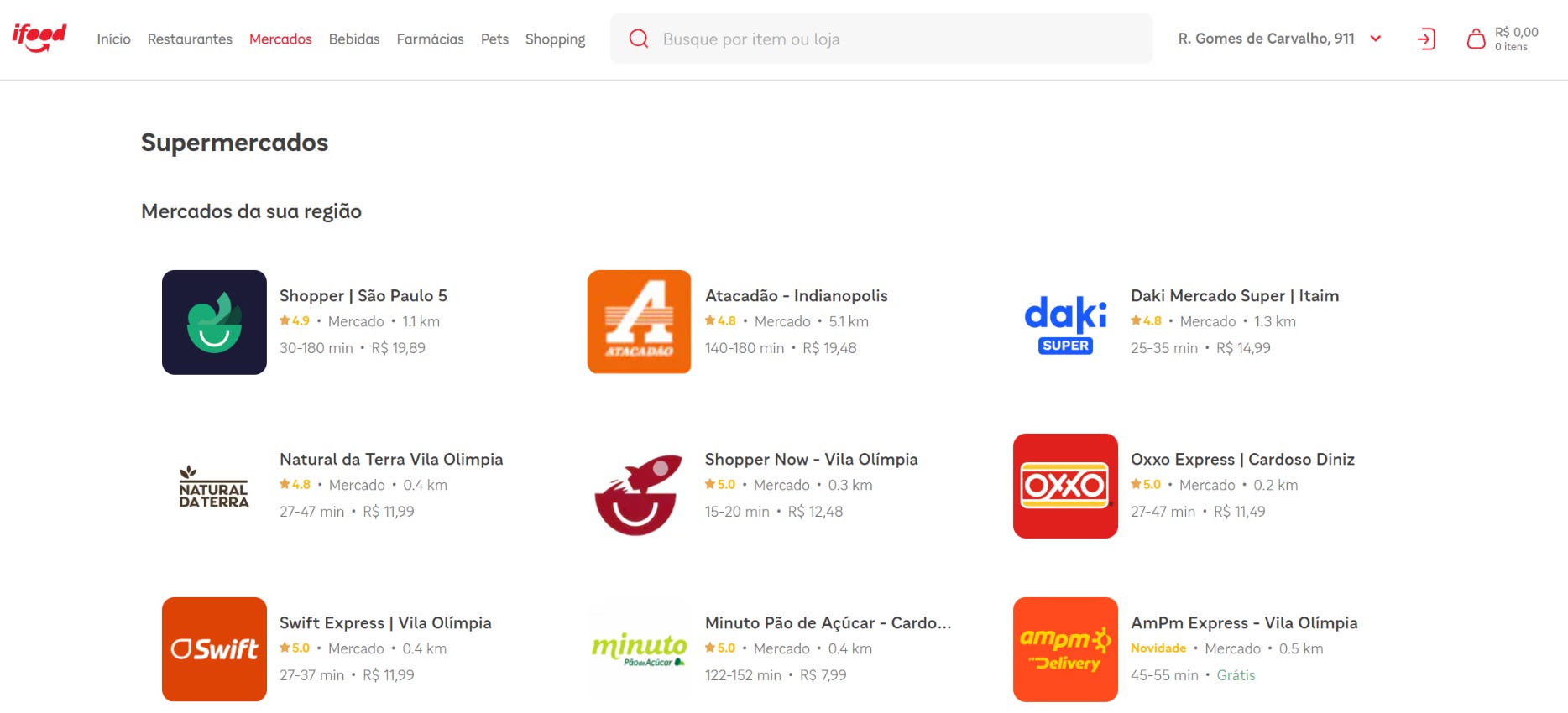

iFood grocery delivery. Source: ifood.com.br

When Didi ceased its food delivery business in Brazil, it continued to offer grocery delivery services. Didi holds a 25% market share in Brazil’s on-demand retail market, with annual revenue of approximately $2 billion. Its grocery delivery business generates roughly $5.5 million in daily revenue, making it highly profitable. At an average order price of $14, Didi completes approximately 400,000 grocery deliveries daily. Notably, 99Food's expansion has had a positive impact on grocery delivery, particularly through cross-selling of groceries and beverages. However, Brazil’s hot climate has increased demand for beverages but also poses challenges for delivery, especially given the perishable nature of fresh food.

Didi’s former decision to continue offering grocery delivery while discontinuing food delivery is primarily driven by high demand for local and online shopping in the region. Shopping malls are widespread, and users are not particularly demanding about delivery times; 45-60 minutes is acceptable. High-value items have a greater advantage in delivery due to their larger order values, more flexible delivery times, and stable fixed costs. Didi's grocery delivery service primarily partners with its own platform and select large supermarkets. Notably, iFood and Didi essentially share the same grocery delivery partners, mainly fast-moving consumer goods retailers and convenience stores, covering products such as dairy.

Brazil’s instant retail market is expanding rapidly, but has not yet fully taken off. Current operations are mainly concentrated in major cities, where large supermarkets are also primarily located. Consumers purchase less frequently; for example, grocery delivery might only be ordered once a month, but the order size is typically large. Instant retail delivery in these areas mirrors JD.com’s delivery model in China. In contrast, Meituan users in China prefer to buy small, fast, and affordable items, while JD.com users tend to make bulk purchases. These characteristics make grocery delivery more attractive and profitable in this region.

iFood has adopted an open strategy in the grocery delivery sector, allowing merchants to operate on multiple platforms without requiring exclusive partnerships. On food delivery platforms, we often see national chains like Starbucks and McDonald’s, while large supermarkets primarily handle grocery retail. Notably, GPA and Carrefour Brazil have annual revenues of $15.7 billion and $14 billion, respectively, demonstrating the substantial sales volume of large supermarkets. Given these large retailers' ample funds, they might choose to operate independently if platforms required exclusive partnerships.

While instant retail typically originated in supermarkets and convenience stores, this phenomenon varies across regions due to cultural differences. For example, the Southeast Asian market is relatively small, while other countries tend to favour bulk purchasing. In some countries, consumers prefer ordering meals for the family rather than individually, reflecting local cultural and consumption habits. iFood's open strategy enables it to better adapt to the characteristics and needs of these diverse markets, thereby promoting business growth.

When Meituan entered the Brazilian market, it prioritised developing its food delivery and self-pickup services rather than immediately entering the fresh food sector. This is because Brazil’s on-demand grocery retail industry is not yet fully mature: online transactions account for only 20%, and its market size is approximately one-fifth that of the food delivery market. Meituan may wait until the Keeta model matures in the Middle East before considering entering Brazil’s fresh food sector. The market considerations behind this strategy are primarily based on the maturity and potential value of various market segments.

Source: Keeta LinkedIn

Having now examined Keeta’s developments in Hong Kong, the Middle East, and Brazil, let’s zoom out again and look at Meituan’s overseas user and merchant recruitment, localisation strategies, funding methods, profitability, and outlook.

User and merchant recruitment

Meituan employs a series of strategies to enhance competitiveness and customer satisfaction as it enters new markets. It promises delivery within 30 minutes for orders covering a 2-3 kilometre radius, and offers compensation for late deliveries. To adapt to local market conditions, Meituan attracted customers early by offering incentives such as free delivery and by improving its delivery system. These strategies gave Meituan a significant competitive advantage in local markets.

In the Hong Kong market, Meituan launched promotions such as half-price or free delivery for the first order, offering coupon packages worth approximately HK$100 (~$13), saving HK$20 to 30 (~$2.50-$4) per meal, and providing free delivery.

In the Saudi market, Meituan launched a promotion for new users offering a 50% discount and free delivery on their first order. The price per order is approximately $13 to $15, with a delivery fee of about $3. In addition, it distributes 2-3 delivery-fee coupon packages, totalling roughly $17-$21. Notably, Meituan’s discounts are even greater in emerging markets. For example, purchasing a $15 item might save $6-$7.

While these measures increase the company’s costs, they also improve user stickiness and market share, both of which benefit the company’s long-term growth. These measures not only attract new users but also help maintain customer loyalty.

Most companies in the industry target high-spending families as their primary customer base for food delivery services, with average order amounts typically between $14 and $21. It’s widely believed that orders under $14 have low demand and are difficult to profit from, especially after deducting platform commissions and delivery costs; small orders often result in losses. Therefore, these companies tend to avoid partnering with small businesses.

However, due to challenges in securing relationships with large merchants, leading food delivery companies have had to shift their focus to small and medium-sized enterprises (SMEs). In some smaller cities, 70%-80% of partner merchants are SMEs. Meanwhile, the food delivery industry's core business is increasingly focused on errand services. Still, the low revenue from these services has delayed overall development by 6 to 12 months. Meituan has adopted a different market strategy, focusing on the small-order market and building a competitive advantage by integrating a large number of small and medium-sized merchants.

Ironically, in Saudi Arabia, the first restaurant Keeta signed was a Chinese restaurant specialising in Hunan cuisine. According to the restaurant staff, Keeta’s employees had been dining at the restaurant for more than a month, and, because the restaurant wanted to test takeaway, the two sides reached a quick agreement. By mid-2024, most of the restaurants Meituan signed in Saudi Arabia were Chinese restaurants, but Meituan still aimed to be a full-category food delivery platform. [12]

Meituan uses a crowdsourcing model with external partners and leverages advanced algorithms to optimise the scheduling system, thereby improving overall operational efficiency. Meituan believes that although the value of a single order is low, significant market potential can still be tapped through precise operations and an efficient delivery system.

To counter Hunger Station’s exclusive partnerships with well-known chain restaurants in Saudi Arabia, Meituan adopted a “benchmarking effect” strategy. Meituan focuses its resources on deep cooperation with a single well-known brand, creating success stories by providing traffic support, resource allocation, and operational assistance to attract other brands to join the partnership and gradually erode competitors’ monopolies.

Meituan’s goal is to secure 2 to 3 partnership opportunities among its competitors' 10 exclusive brands. Given that market leaders like Hunger Station have already achieved profitability and solidified their market position, they may respond to Meituan’s challenge by lowering commission rates or delivery fees, which will trigger long-term competition centred around refined operations and strategic planning.

In Meituan’s overseas business, Agora’s Conversation 2.0 system is used to handle telemarketing tasks. In the Brazilian market, an AI assistant for Keeta makes 50,000 to 60,000 calls daily. This assistant’s role is to promote opportunities for cooperation with merchants and arrange meetings, thereby improving customer acquisition results.

Funding

Meituan employs an independent budgeting model, separating overseas expansion funds from domestic core business funds to ensure fluctuations in domestic performance do not affect the progress of overseas projects. In 2024, the company planned to invest 1.1 billion Saudi riyals (~$290 million) in the Middle East, and 200 million Reais (~$37 million) in its Brazilian project, with these funds managed through dedicated financial channels. Simultaneously, the company is exploring capital market operations to raise funds for Keeta.

However, the Middle East received the largest allocation of funds in the third quarter of 2025. Looking at annual statistics, actual expenditures in the Middle East far exceeded the initial budget of 1 billion Saudi riyals, amounting to approximately $267 million. Since commencing operations in Brazil in May, Meituan has invested $80 million. In contrast, the Hong Kong market’s total annual investment did not exceed $10 million, and it achieved a small profit between September and December. According to the financial plan for the fourth quarter of 2025, investment in both the Middle East and Brazil would continue to increase.

While a decision on whether to introduce equity investors has not yet been finalised, the company prefers to establish Keeta as an independent financing entity to alleviate cash-flow pressure on the parent company and attract investors who value the project’s long-term growth potential. In the food delivery industry, market share is crucial; only the top two platforms survive. If the 10% market share target for Brazil is not achieved by 2026, increased investment will be made to enhance the market position. This strategy draws on experience from expansion in the Middle East, prioritising market share even if it means exhausting nearly all initial budgets.

Meituan will prioritise the Keeta project as a key resource allocation task over the next 2-3 years. The project, a core component of the company’s strategic transformation, is expected to receive billions of dollars in investment. Funding for the Keeta project will primarily focus on unmanned delivery technology and artificial intelligence, two core pillars of Meituan’s strategic transformation. However, the domestic local life services and instant retail sectors are highly competitive, with Meituan facing subsidy challenges from platforms such as JD.com, Alibaba, and Douyin. This competitive landscape could cause its food delivery business to shift from profitability to losses. Simultaneously, Meituan’s primary local merchant services are experiencing reduced profit margins due to the food delivery price war, potentially shortening the tolerance period for losses in new businesses.

Staffing & Localisation

Meituan faces numerous localisation challenges in its international expansion, including cultural differences, varying consumer habits, and technological limitations. Because its mini-programs are unavailable overseas, Meituan can only promote its services through app downloads, which, to some extent, limits its market penetration.

To address the challenges of language and cultural adaptation, Meituan has taken several measures. First, the company employs staff fluent in local languages and actively seeks talent proficient in these languages (such as Arabic) to ensure smooth communication with customers and partners. Second, Meituan plans targeted marketing campaigns around local festivals, such as launching exclusive offers during Ramadan, to better integrate with local culture. Furthermore, Meituan collaborates with local translation agencies and trains its internal teams to better understand the cultural characteristics of target markets. These efforts aim to better align Meituan’s products and services with the needs and preferences of local users.

To enhance competitiveness in Hong Kong, Meituan implemented a series of localisation strategies. One key measure was its allocation of 2% of total transaction volume annually to brand promotion. Furthermore, it launched set meals adapted to local dietary habits in the Hong Kong market. When expanding into international markets such as the Middle East, Meituan places great emphasis on developing product and marketing strategies tailored to local food cultures. For instance, in the Middle Eastern market, it needs to develop strategies for both Western fast food and traditional cuisine that align with local taste preferences. These data-driven strategies and technological capabilities help it remain competitive in the international market.

Despite these measures, there are still areas for improvement. The company needs to continue to deeply understand the unique characteristics of each target market and continuously optimise its localisation strategies to maintain a foothold in the fiercely competitive international market.

Meituan took several concrete measures in talent recruitment and development to support its business growth and technological innovation. First, Meituan’s talent strategy focuses on attracting professionals with both local and international experience. For example, in Hong Kong, the company offers starting salaries of $43,000–$57,000 to recent graduates and interns, who are required to have local collaboration experience and an international perspective. Internally, Meituan has established “Meituan University,” an institution that assesses and enhances employee capabilities through various methods and provides employees with two career development paths: technical and sales management.

In addition, Meituan has launched the “Beidou Plan,” recruiting 5,000 to 6,000 highly qualified talents annually across multiple fields, including technology and operations, to ensure the company maintains its technological leadership. Meituan also promotes the expansion of its international business through various technological innovations. For instance, the company’s delivery system algorithm has undergone multiple improvements, evolving from initially providing only an approximate delivery time to now being accurate to the minute and comprehensively evaluating performance in all aspects. Meituan also utilises transaction data and large-scale data models to formulate localisation strategies.

In the fourth quarter of 2024, Meituan Waimai began organising internal presentations to encourage employees to switch to Keeta to support its overseas business. [13] However, during international expansion, Keeta and Keemart primarily recruited locally for entry-level positions, including delivery drivers, customer service staff, and marketing staff. However, approximately 90% of core technical positions are filled by the Chinese team, and management positions are also held primarily by Chinese employees. In the Middle East, about 10% of key positions are held by expatriates, primarily at Meituan’s L7 level and above. In Brazil, due to challenging business conditions and complex labour regulations, the proportion of local employees may be higher than in the Middle East.

By the fourth quarter of 2025, Meituan's operations teams in Brazil will be primarily composed of local employees, with dispatched workers from China accounting for less than one-fifth of the workforce. The total team size is expected to reach approximately 1,000. Meanwhile, it will continue to prioritise localisation as a key development strategy.

In the Middle East market, Meituan’s senior management directly handles communication with local governments, rather than relying on hiring highly skilled local talent. This operational model has proven effective in the Middle East. Furthermore, Meituan’s core positions are handled by the domestic team, with over half of its members having previously worked in Hong Kong. This team structure enhances collaboration and execution efficiency.

Meituan’s regional partnership system and outsourcing strategy in its expansion in the Middle East market have had a significant positive impact on its operating cost structure and profitability timeline. During the market promotion phase, Meituan typically assigns 1-2 local employees to assist, leveraging their resources to drive business development. Promotion efforts in Saudi cities such as Riyadh and Al-Aqji have progressed smoothly.

Keeta’s rapid expansion in the Middle East market is attributed to several key factors. First, it introduced a domestic regional partnership system to attract experienced local talent. Simultaneously, it outsourced basic operations such as fulfilment, marketing, and customer service, thereby rapidly driving business growth. This strategy significantly reduced initial investment costs compared to building its own team.

Meituan maintains good cooperative relationships with local governments in the Middle East, with the governments of Saudi Arabia and Dubai showing a friendly attitude towards Meituan. Meanwhile, in the Brazilian market, despite legal disputes and competition from 99Food and iFood, the local government has not demonstrated favouritism toward competitors. It has maintained a relatively friendly attitude towards Keeta.

Keeta’s expansion, based on a highly localised model, has significantly reduced geopolitical risks and created numerous jobs and tax revenues for local governments. [14]

Keeta São Paulo. Source: Keeta LinkedIn

Profitability

The challenges Meituan faces in its overseas expansion have significantly impacted its profitability and return on investment.

Regarding digitalisation, practical experience in Hong Kong revealed that, even in a highly developed economy, Hong Kong's level of digitalisation is only about half that of mainland China. China ranks among the world’s leaders in service industry digitalisation, with even small restaurants deeply integrated into digital platform ecosystems. The significantly lower digital penetration rate in overseas markets undoubtedly increases operational complexity.

Furthermore, payment preferences vary across regions. For example, the Middle East has a high acceptance of electronic payments, whereas online payment capabilities are weaker in Brazil, posing challenges for the operations team. Regarding product localisation, Keemart needs to adjust its product structure overseas, such as reducing the proportion of fresh produce and increasing the variety of goods that meet local consumer preferences. On the other hand, Keemart needs to pay special attention to religious and cultural restrictions, particularly the taboos imposed on certain goods in Muslim countries. These factors combined pose multiple challenges to the profitability and return on investment of Meituan’s overseas business.

In the Hong Kong market, the takeaway business has seen a significant improvement in losses. Initially, the loss per order exceeded HK$2 (~$0.26), but by the end of 2024, it had decreased to just over HK$1 (~$0.13). In October 2025, Keeta achieved profitability in the Hong Kong market ahead of schedule, and its market share already exceeded 50%. It was still increasing its order volume and market share. [14]

Profitability in the Middle East hinges on specific markets, such as Saudi Arabia, where order density must reach a certain level for unit economics to become positive. Current losses are primarily due to low pricing and subsidy strategies used in the early stages of market expansion to gain market share. For example, subsidies for merchants or reduced delivery fees resulted in lower average order values compared to competitors.

The situation in Saudi Arabia differs from that in Hong Kong. On the one hand, local leaders are larger and stronger; on the other, they have a greater need for localisation. From a specific market perspective, Meituan found that local food delivery platforms in the Middle East primarily target families, offering meals for two or more people. Therefore, Meituan adopted a differentiated competitive strategy focusing on single-person meals, which received a positive market response.

Many catering businesses in Hong Kong share the same brands as those in mainland China, where they have worked with Meituan. Therefore, expanding into the Hong Kong market is easier for Meituan on the supply side than in Saudi Arabia. However, in Saudi Arabia, the average order value is higher, the UE model is stronger, and, theoretically, it is easier to achieve break-even. One analyst said it should be possible for Keeta to break even in the fourth quarter of 2026, but there is still a long way to go to achieve the industry's number one market share. [14]

Regarding profitability in the Middle East, given Uber Eats’ take rate in the high-priced European market (around 3%), the average order value is expected to decrease from approximately $21.50 to between $14 and $17 to attract a broader user base. Meanwhile, in the Gulf region, the company faces intense competition from Deliveroo and Talabat, the region's market leader. Talabat has an extensive merchant network across key markets, including the UAE and Kuwait, and offers lower delivery costs. Keeta will achieve break-even in some cities starting in 2026 and gradually enter the profit-making stage.

In the medium to long term, Keeta has a high probability of achieving both market share and profit success in the Gulf market, but faces greater uncertainty in the Brazilian market. Profitability in Brazil is expected to be a long-term process, potentially reaching profitability as early as 2027 or 2028. If it can achieve both market share and profitability in the Brazilian market, then Keeta’s valuation can begin to be benchmarked against DoorDash (measured by comparable GTV), and Meituan’s valuation will undergo a significant revaluation. [14]

Meituan’s financial performance in international markets is primarily influenced by three factors: platform commissions, advertising revenue, and delivery fees. There are indeed significant differences in order value, labour costs, and customer acquisition costs across different regions of the food delivery market.

In Hong Kong, the average order value is between $13 and $14, which is 40% to 80% higher than in mainland China. This higher order value can positively impact profitability. However, overseas markets also face higher operating costs. In Hong Kong, delivery drivers can earn HK$30,000 to HK$40,000 (approximately $4,000- $5,000) per month. Specifically, delivery fees in Hong Kong are approximately HK$15-16 (~$2) per order, more than twice those in mainland China. Meanwhile, in Saudi Arabia, the delivery fee per order is approximately $3, two to three times that of mainland China. This difference in labour costs directly affects a company’s operational strategies and profitability. These cost differences force companies to adopt different pricing and operational strategies in different markets.

Customer acquisition costs also vary by region. In the Hong Kong market, customer acquisition costs are approximately 1.5 times those in mainland China. This means that companies need to be more cautious when formulating market expansion and customer retention strategies. Taken together, these regional differences have had a profound impact on the company’s profitability and operating strategies across markets, requiring it to develop tailored strategies for each market's characteristics.

In Hong Kong in 2024, Meituan charged approximately a 5% commission per transaction, advertising revenue accounted for 1-2%, and delivery fees accounted for about 15% of the total order value. In contrast, in Saudi Arabia, where Meituan had only operated a few months, it had lower commission rate, delivery fees accounting for about 20% of the total order value, and low advertising revenue, resulting in an overall loss of about 5%. In the long term, Meituan plans to optimise operating costs to bring the profit margins in these two markets to a level comparable to its domestic business.

Regarding its profit model, Keeta’s strategy focuses on four different customer spending ranges: $10, $15, $20, and $25, each corresponding to different order types and cost structures. The application scenarios for these pricing strategies are pretty complex. Monthly order frequency is a key indicator when assessing consumer behaviour, especially in overseas markets. For example, in the Middle East, a monthly order frequency of 8 times increases the likelihood of profitability; a frequency of 10 times further increases it. It is worth noting that, due to higher single-delivery costs in overseas markets, the share of delivery costs in total costs is a crucial indicator that requires close monitoring.

Keeta plans to achieve full profitability across all major regions, beginning in the Middle East, between 2028 and 2030.

Keeta driver station in Brazil. Source: Keeta LinkedIn.

Challenges and Outlook

Meituan has chosen two projects for its international expansion: Keeta and Keemart. These businesses were selected because they are highly replicable and fall within Meituan’s strengths. Keeta is an overseas extension of its core food delivery business (Meituan Waimai), while Keemart, based on Xiaoxiang (Little Elephant) supermarket, currently operates only in Riyadh, Saudi Arabia.

Keeta’s mission is to extend Meituan’s rich operational experience in domestic and international food delivery and instant retail to the international market, to drive new business growth. Keeta bears the heavy responsibility of transforming Meituan from a domestic platform economy company into a global enterprise, a transformation that should help improve the company’s valuation in the capital market. Meituan aims to emulate the valuation methods of multinational corporations like Google through Keeta’s global expansion, thereby gaining greater recognition in the capital markets. As a vital component of Meituan’s internationalisation strategy, the Keeta project has received the group’s highest level of investment attention, ranking first in resource allocation priority among new initiatives.

Keeta faces both challenges and opportunities during its global expansion. First, it must strictly comply with the laws and regulations of various countries while navigating economic and political uncertainties. Particularly in the European market, the platform would encounter fierce competition, high operating costs, and inefficiencies. Notably, many delivery riders in Europe choose to deliver food by bicycle, which has impacted delivery speed.

To address these challenges, the company adopts flexible strategies. It adjusts its operations according to the regulatory environment and cultural characteristics of different countries, for example, by employing workers from specific ethnic groups and optimising algorithms to improve service quality. In the Middle East, while language diversity poses a significant challenge, the region’s diverse population also presents considerable growth opportunities for the food delivery industry. Overall, the platform continuously adapts and innovates in its globalisation process to overcome various obstacles and seize new market opportunities.

Middle East

Meituan plans to solidify its second-place position in Saudi Arabia by order volume and transaction value, and to surpass the leader, HungerStation, in order volume when the time is right. The company plans to expand into the emerging markets of Bahrain (where it was launched on January 5 2026) and Oman, while also assessing the market potential of Iraq and Egypt, hoping to achieve economies of scale through language and cultural similarities.

Meituan plans to achieve a market dominance in the Middle East similar to its domestic 60% vs. 40% share within three to five years, but faces several challenges. It anticipates becoming the second-largest player in the market by transaction volume within three years, while achieving a comprehensive technological and operational advantage will take four to five years.

The total market size in the Gulf region is approximately $10 billion, with a projected CAGR of 22%-24%. The company’s near-term goal is to capture over 40% market share, ideally exceeding 45%, with the potential to reach over 50% in the long term. If operational capabilities are fully validated, the company expects to achieve a 40% market share by mid-2027. Given that perfecting the business model takes 2.5 years, the company anticipates covering all planned regions and achieving its goals by the end of 2027 or the first half of 2028. However, the implementation of the market strategy may be affected by key uncertainties, such as local legal disputes, which could hinder the establishment of exclusive partnerships. Furthermore, the difficulty of gaining localised market insights in highly competitive overseas markets is also a significant challenge.

The target for total merchandise transaction volume in the Middle East in 2026 is set at $5 billion, excluding fresh grocery retail. Strong performance in fresh grocery retail could add $1 billion, bringing the total target to $6 billion. However, to break even in the Middle East, total food-delivery transaction volume needs to reach $8 billion, or $9.3 billion if non-food services such as fresh grocery retail are included. By 2027, GMV in the Middle East is expected to exceed $8.6 billion, with Meituan potentially capturing about one-third of the market and ranking among the top two by order volume.

Latin America

In the Brazilian market, Keeta is still in its early stages of order volume, with a peak of approximately 10,000 orders per day, and losses are relatively manageable. Because order growth in Brazil is slow, the pressure of subsidising individual orders has not yet significantly impacted the overall business. Given this situation, future development in Brazil will focus on enhancing supply-side capabilities and prioritising partnerships with additional catering businesses to scale supply.

In addition to its expansion in the Middle East and Brazil, the food delivery giant plans to pursue new growth opportunities in Latin America, targeting countries such as Colombia and Argentina. It will undertake preparatory work, including recruiting delivery drivers, establishing merchant partnerships, and conducting market research, to pave the way for business expansion in 2027.

Other Markets and Services

Meituan may evaluate other emerging markets that have not yet been publicly disclosed, but separate budgets will be required to address the high market-entry costs. Of particular note is the expectation that significant investment will begin in the first quarter of 2026 if substantial progress is to be made in the Brazilian market.

The company is researching the Japanese, South Korean, and European markets, but has no concrete plans to enter them in the short term. The current strategy is to concentrate resources on validating the feasibility of the culture and business model within a single region. For example, after demonstrating profitability in the Middle East, they will consider expanding into other cultural markets. This approach aims to avoid overextending themselves. In the long run, it will expand into additional overseas markets, including Southeast Asia, Central Asia, and Europe. [12]

As far as services are concerned, Meituan plans to gradually promote its successful local life services in China, such as flash sales, ride-hailing, and coupons, to overseas markets. However, due to the significant investment required, there are currently no specific overseas expansion plans for its payment and ride-hailing businesses.

However, Meituan has also launched its power bank rental business under the Keeta brand in London, with many convenience stores across the city displaying Meituan’s yellow charging stations. [15] This could be a first step toward gaining users who Keeta can later cross-sell other services to.

Source: Momentum Works [15]

One final point worth noting is that our friends at Momentum Works recently reported that Meituan has launched a US business. But it was not related to self-operated meal or grocery delivery, and Keeta. Instead, it launched a POS/restaurant SaaS system in the U.S., Peppr, which focuses on family-owned mom-and-pop restaurants. By October 2025, Peppr had over 200 employees, with a fairly diverse and international team profile. [15]

Source: Peppr.com

According to Momentum Works, Meituan has already been planning the launch of Peppr since 2023. The system is based on Meituan’s restaurant management system (RMS) in China, which is used by a significant proportion of its 15 million active merchants. Peppr was, however, rebuilt almost from scratch rather than simply localising Meituan’s domestic RMS in China to serve the US market. Another difference is that Peppr is offered as a model-based solution, including POS, Ordering & Delivery, and Kitchen Display System (KDS). [15]

As with the power bank business for UK users, Peppr could serve as an entry strategy for other Meituan services in the US.

Strengths and Overall Targets

Wang Xing, CEO of Meituan: “Meituan is destined to become a global company. We are not in a hurry and will evaluate every opportunity very carefully.” [8]

Meituan’s operational efficiency and data analytics capabilities, demonstrated through Keeta and Keemart in the Middle East market, have the potential to become key drivers of long-term market leadership. First, in terms of delivery efficiency, Meituan’s Keeta and Keemart perform exceptionally well, with over 90% of orders completed within half an hour and approaching 95%. In contrast, local Middle Eastern platforms achieve only 60-65% on similar metrics.

Furthermore, in terms of product matching accuracy and coverage, Keemart’s data performance significantly outperforms HungerStation’s, with related metrics 2 to 3 times higher. More importantly, Meituan excels in data analytics and delivery services, particularly the significant synergy between Keeta and Keemart, leveraging data insights to improve operational efficiency. In its B2B business, Meituan has significantly boosted merchants’ sales performance by helping B2B partners develop best-selling products. Finally, Meituan’s experience developing popular products and providing merchant services in the domestic market enabled it to achieve rapid success in the B2B sector, making it a core competitive advantage.

Meituan’s differentiated competitive strategy across overseas markets stems primarily from its in-depth analysis of the local competitive environment and the strategic utilisation of its financial strength. Meituan’s substantial financial resources allow it to invest heavily in market subsidies, a strategy that successfully attracted a large number of consumers, helping Keeta and Keemart rapidly capture market share.

In the Middle East, Meituan adopted a relatively aggressive expansion strategy, driven by a favourable competitive environment. Local Middle Eastern companies such as Nana, Rabbit, H Market (launched by HungerStation), and the local delivery service Jahez still lag significantly behind Meituan in financial and technological strength. This disparity gave Meituan an opportunity to quickly gain market share through its capital advantage.

However, Meituan adopted a more cautious strategy in the Brazilian market, primarily because competitors in this region have stronger financial backing and significantly outperform those in the Middle East, such as HungerStation and Jahez. Therefore, Meituan’s financial investment decisions are directly influenced by the capital strength of its local competitors. It adopts an aggressive strategy in markets where competitors are relatively weak, while choosing a more prudent investment approach when facing competitors with substantial capital.

Qiu Guangyu shared his experiences in Saudi Arabia in an internal interview and discussed “what we rely on to win”. He gave three directions: product technical capabilities, more efficient order dispatching, more accurate calculation of delivery time; operation and sales management methods, “start early, summarise late”, quickly improve user experience; focus on customers, when overseas is still in the stage from 0 to 1, to be more agile in discovering user problems and live like locals. [13]

Keeta aims to achieve a transaction volume of over $14 billion in its food delivery business within the next 3 to 5 years. If other services, such as groceries (Keemart), are included, the total transaction volume is expected to reach $21 billion.

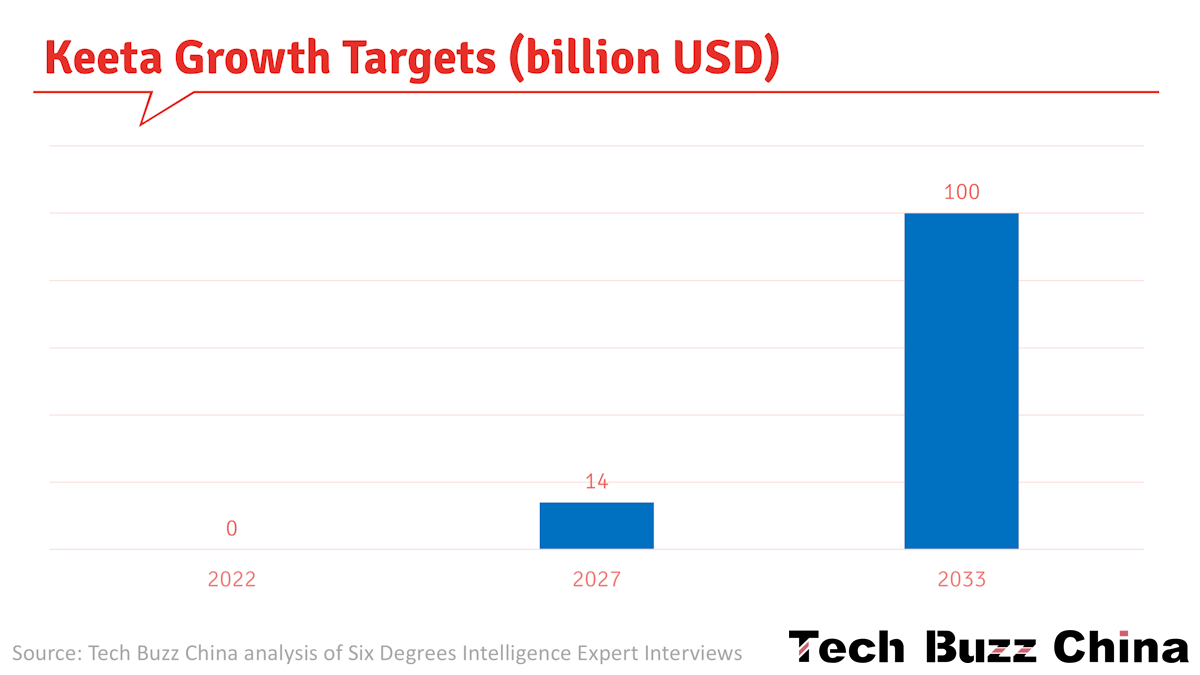

For Keeta, Meituan plans to reach an annualised gross merchandise volume of $100 billion within 10 years, starting with its launch in Hong Kong in May 2023, with this target set for May 2033. [16]

Key Takeaways and summary video

The key takeaways and the summary video below were created using Google Notebook.

Global Valuation Ambitions: Meituan views its international brand, Keeta, as a vehicle to transform from a domestic platform into a global enterprise, aiming for a massive $100 billion annualised gross merchandise volume (GMV) by 2033.

Strategic Focus on Brazil: Brazil is a high-priority market due to its large population (200 million) and high internet penetration (90%), yet it remains under-penetrated in food delivery compared to China, offering significant growth potential.

Massive Financial Commitment: Meituan CEO Wang Xing signed a $1 billion commercial agreement with the Brazilian President to fund Keeta’s expansion, including the construction of a logistics network with over 100,000 riders.

Challenging a Dominant Incumbent: The primary obstacle in Brazil is iFood, which holds a near-monopoly with an 80–90% market share and has built strong barriers through exclusive merchant agreements.

Inter-Chinese Rivalry: Meituan is engaged in “cutthroat competition” with fellow Chinese giant Didi (99Food) in Brazil; this rivalry has already escalated into legal disputes over trademarks, colour schemes, and search-term diversions.

Aggressive Market Entry Strategy: To break into the market, Keeta is using heavy subsidies and zero-commission periods for merchants, with a medium-term goal of capturing a 30% market share to form a duopoly with iFood.

Efficiency Through Full-Time Riders: Unlike Didi, which relies heavily on part-time drivers, Keeta employs a full-time delivery rider system to ensure long-term stability and superior delivery efficiency.