Tencent’s e-Commerce Revival. Part 3: Challenges & Outlook

WeChat e-commerce faces many challenges. What are the expectations?

Contents

Things that caught our attention

A collection of posts by Ed Sander and Rui Ma on Substack Notes, Twitter and LinkedIn.

Introduction

In June, we took a deep dive into WeChat’s new gifting function, an example of how Tencent sees e-commerce evolving in the ecosystem of its popular chat app. Last week, we took a closer look at the parts of WeChat’s ecosystem that facilitate the e-commerce that Tencent wants to revive to monetise the app further. Mini programs, WeChat Channels videos, public accounts, and search are all connected to WeChat Stores, where transactions will take place.

In this third and final part of this series, we will look at the various challenges Tencent faces in growing the GMV of e-commerce in WeChat. We also share the outlook and expectations for its initiatives.

As a continuation of the previous part in this series and because it requires the background knowledge shared last week, this article is only available to paid members.

Become a paying subscriber to unlock the full report and support our in-depth research into key China tech trends.

Ed Sander, Tech Research Analyst

Challenges for WeChat e-commerce

WeChat Stores faces some significant challenges in market competition. First, compared with major competitors, WeChat Stores are at a disadvantage in attracting traffic and marketing because of WeChat’s social network ecosystem. Second, consumers are less aware of WeChat Stores than of traditional e-commerce platforms. Another critical issue is the high return rate of WeChat Channels, primarily due to consumers' purchasing methods, insufficient marketing efforts, and issues with after-sales service. Finally, the trust in the platform is not high, which has negatively impacted its overall performance.

The long-term market share of WeChat Stores in the e-commerce industry remains uncertain, and a clear gap persists compared to major competitors such as Douyin and Kuaishou.

Below, we have grouped some other challenges into different categories.

Consumers

Customer acquisition & retention

User growth of WeChat Channels is one of the key indicators of the growth of WeChat Mall. Tencent needs to pay close attention to the retention rate of daily and monthly active users to ensure that they continue to grow. If the user growth rate turns negative, it may indicate that the platform development has hit a bottleneck and needs to find new breakthroughs. Although the reward function has achieved some results, progress in the content field still needs further breakthroughs. The gift function has also achieved some success, but there is still room for improvement in content.

The user groups of WeChat Channels and private domain communities have an inevitable overlap. In the user composition of WeChat Channels, private domain users account for a relatively high proportion, between 80% and 90%, while the proportion of public domain traffic is relatively low, between 10% and 20%. The expansion of WeChat Channels, therefore, depends mainly on the scale of private domain users and additional promotion efforts.

Consumer Habits

Tencent's core goal is not only to expand traffic, but more importantly, to change users' consumption habits. WeChat Stores need to reach a certain user scale before they can truly compete with other e-commerce platforms.

Although WeChat Stores can achieve short-term revenue peaks through the gift function during the holiday season, other strategies are needed to achieve long-term growth. WeChat aims to cultivate users' shopping habits on social media while continuing to attract traffic. At present, the average order value of WeChat Stores is between RMB 100 and RMB 300, and there is still room for improvement in user activity.

A significant problem is that most orders come from livestreams or recommendations from influencers. Still, consumers' shopping habits and stickiness on social media in general and WeChat in particular have not yet been fully formed.

In response to these challenges, WeChat plans to gradually cultivate users' awareness and consumption habits of WeChat Mall in 2025. In the future, WeChat may consider establishing an independent e-commerce platform and a dedicated entrance to meet user needs better and address these challenges.

Consumer profile

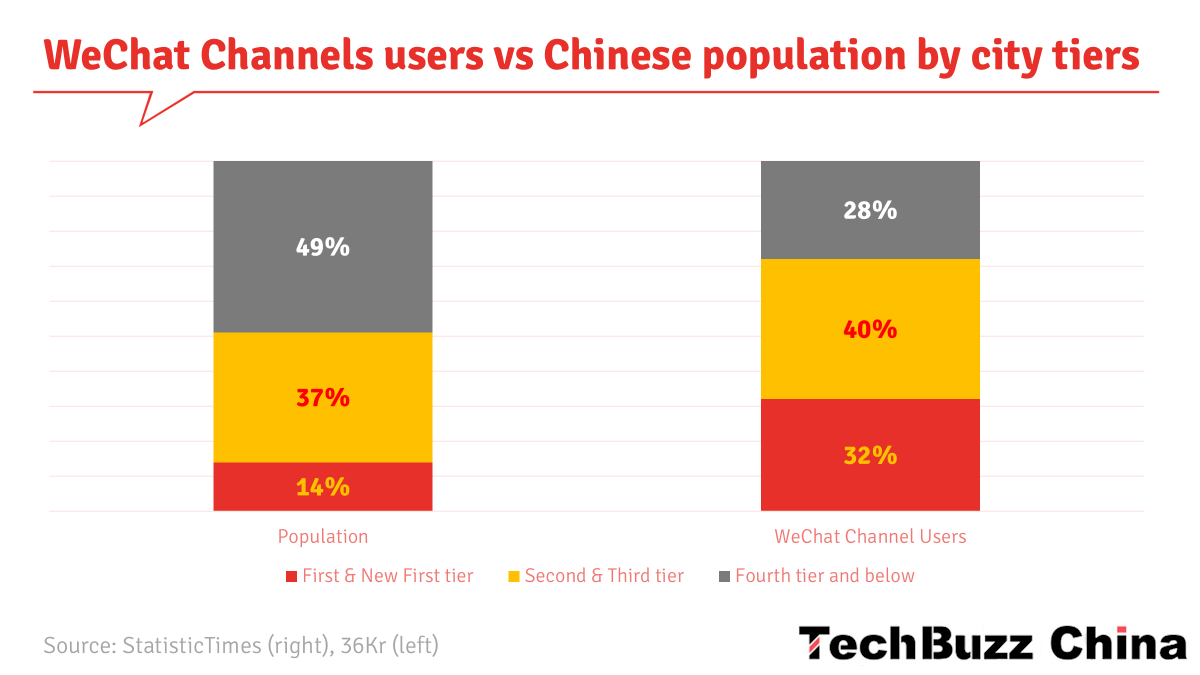

The total number of WeChat users has exceeded 1.3 billion, while the number of WeChat Channels users is only 600 million. The primary user group of WeChat Mall is still the post-80s generation. At present, the early users of WeChat Channels are mainly people between the ages of 35 and 60. The average age of WeChat Channels users is about 10 years older than that of Douyin users. This phenomenon may have a significant impact on the content and business strategies of the two platforms.

97.7% of the users of WeChat Channels are over 25 years old, and 63% are women. 32% of the users are from first-tier and new first-tier cities, 40% are from second-tier and third-tier cities, and 28% are from fourth-tier, fifth-tier and sixth-tier cities and overseas. It can be concluded that the core user group of WeChat Channels is adult women from second-tier and third-tier cities. [1] WeChat Channels also seems to be underrepresented in the ‘sinking market’ of lower-tier cities, where Kuaishuo is very popular.

Faced with this situation, if Tencent wants to attract more young users, it needs to develop a breakthrough strategy to attract young groups from the Douyin platform, where, at present, young users are mainly concentrated. In the future, WeChat Stores may attract young people around 20 years old through the gift function, primarily by leveraging the exposure they receive when older generations give gifts to younger generations. Nevertheless, the primary user group of WeChat Channels in the short term will still be people over 35 years old.

UX & Visibility

WeChat Channels and WeChat Stores require increased exposure and more traffic entrances. The current e-commerce entrances are relatively hidden and may be gradually moved forward in the future to increase visibility. WeChat Mall currently does not have a separate entrance within the WeChat platform, unlike Douyin, which has Douyin Mall. To avoid impacting existing products, such as mini-programs and official accounts, promotions will be handled through other functionalities, including search, gifting, and WeChat Channels, for the time being.

Despite this, WeChat Channels and private domains are expected to become the primary sources of growth, with WeChat Channels potentially contributing RMB 400 billion to RMB 500 billion, and private domain communities contributing RMB 300 billion to RMB 400 billion.

Merchants & brands

In the process of expanding the number of merchants, WeChat Stores needs to maintain the current activity and increase the total transaction volume (GMV) at the same time. Specifically, WeChat Stores aims to increase GMV from RMB 150 billion to RMB 300 billion or more. To achieve this goal, the platform must attract 20 million merchants and cover a diverse range of categories to meet the needs of all consumer types. This strategy will not only help expand market share but also promote a shift in user consumption habits, thereby gaining a foothold in the highly competitive e-commerce industry.

For brand merchants, the WeChat ecosystem provides a unique opportunity. Compared with other platforms, the WeChat ecosystem is a platform with relatively little competition and greater growth potential. This means that brands can find more development opportunities here without having to face fierce competition on other platforms.

However, WeChat faces challenges in attracting merchants, mainly because its investment promotion team is relatively small, which is significantly different from its competitors. For example, there are only 4 people in the field of personal care and home cleaning, while Douyin's team in the same field has more than 150 people. To address this issue, WeChat has implemented a strategy of introducing preferential policies to attract high-quality merchants, thereby compensating for its shortcomings in investment promotion.

WeChat Mini Programs and WeChat Channels e-commerce are still very attractive to merchants, mainly due to their large user base. WeChat's monthly active users have reached an astonishing 1 billion, and its daily active users are also between 700 million and 800 million.

ROI & Effectiveness

Before 2024, the transaction volume of many major customers on WeChat Channels would have been zero. Still, after a year of development, some customers have reached a transaction scale of RMB 50-80 million. In general, the transaction volume of goods on WeChat has grown rapidly, possibly reaching twice that of last year, but the current absolute value is still low.

Although the total GMV on WeChat Channels has grown rapidly, it is difficult to narrow the absolute gap with Douyin significantly within this year, and it may take until next year or longer for there to be significant changes. The GMV of a well-known beauty brand on WeChat Channels is about RMB 60 million, while on the Douyin platform, it is as high as RMB 1-1.2 billion. Despite this, the proportion of investment by major customers on WeChat Channels is rising rapidly.

The potential of top brands on WeChat Channels has not yet been fully demonstrated, and Tencent needs to pay close attention to its development trends. Attracting more well-known companies to participate is crucial to the overall development of WeChat Channels, which will help enhance the platform's influence.

Still, major beauty brands are cautious about advertising on WeChat Channels. Leading companies in the beauty industry, such as Estee Lauder, L'Oréal, and domestic brand Proya, have not yet placed large-scale advertisements on WeChat Channels. This is mainly because the WeChat Channels platform currently lacks an adequate return on investment mechanism, and its stability needs to be further improved.

Finally, due to the lack of reference to successful cases, large merchants are generally reluctant to advertise on WeChat Channels. Tencent expects the share of budget merchants allocated to WeChat Mall to increase from the current 10% to about 20%. However, there has been no successful case with a high return on investment so far. WeChat Channels has not yet proven to be very effective as a sales tool, and despite two years of testing, the results are still limited.

In terms of ROI, there are some differences between the performance of WeChat Channels and Douyin. In some areas, Tencent WeChat Channels' short-term ROI has exceeded Douyin’s, but this situation varies depending on the industry and specific application scenarios. The reward function of WeChat Channels performed exceptionally well during the Lunar New Year, which is closely related to the increase in users' emotional consumption during the holiday period. However, whether WeChat Channels can effectively combine the reward mechanism with commodity pricing and e-commerce consumption habits in the second to fourth quarters still needs further research and exploration.

WeChat Channels traffic is highly volatile. The ROI of advertising on Douyin is usually around 1:2 - 2.5, and the average is about 2.2 - 2.3. However, the ROI of WeChat Channels fluctuates wildly, ranging from 0.8 to 2.8. This instability leads advertisers to prefer stable delivery effects rather than relying on highly uncertain traffic.

Lack of profile data

While WeChat Channels' overall advertising ROI is volatile, the platform does not perform well at all in the field of e-commerce advertising, ranking at the bottom among major e-commerce platforms, with an average ROI of only 0.1%. The main reasons for this include transaction data that is not as accurate as Tmall and Douyin, inaccurate user tags, and unsatisfactory performance of algorithms based on social relationships, which limit transaction results. Currently, most brands struggle to achieve a positive return on investment on the Tencent platform. Although no effective operation method has been found yet, companies will continue to try WeChat Channels due to the lack of better media options.

Tencent entered the short video market late (in 2020) and still has a significant gap compared with its competitors. Due to the short time for user data accumulation on WeChat’s e-commerce platform and the lack of content diversity like that of Douyin, Xiaohongshu, Kuaishou, and Bilibili, the analysis of user preferences is not comprehensive enough, which impacts the effectiveness of advertising. Most merchants are still waiting or conducting small-scale tests.

The sales scenarios of WeChat Channels need to reach a mature stage, with transaction data that is rich enough and user tags that are accurate, to attract more brands to place advertisements in the livestreams and achieve breakthroughs. In the long run, if Tencent can enhance its transaction data accumulation, user tagging quality, and algorithmic capabilities, its advertising effectiveness may improve over the next few years. However, this requires a significant investment of time and resources.

Products

While cosmetics and skincare products performed well during the holiday season, other categories were lagging.

WeChat stores currently face the problem of limited product variety and high prices, and some merchants need to rely on the support of third-party service providers such as Weimeng and Youzan. These problems are complex to solve in the short term completely, and the characteristics of social network apps also limit the increase in natural transaction volume.

Content

Currently, the average daily usage time of WeChat Channels users is approximately 70 minutes, leaving a considerable gap from the target of 150 minutes, which may require sustained efforts to achieve. Meanwhile, the average daily usage time of users of Douyin and Kuaishou has exceeded 120 minutes.

The online celebrity promotion strategy of WeChat Channels is similar to that of Kuaishou, focusing on the management of fan groups, the establishment of personal brands, and the cultivation of trust. In fact, the users of WeChat Channels exhibit a high similarity with those of Kuaishou, allowing for the reference to Kuaishou's growth strategy for development. The main characteristics of Kuaishou include community, focusing on intimacy between users, building personal image, and building trust. Although the content production of WeChat Channels needs to be more refined than Kuaishou, similar target audience characteristics should be maintained.

There are still some shortcomings in the content ecology of WeChat Channels, which directly affect its overall growth trend. Currently, most content on WeChat Channels is transferred from other platforms, lacking uniqueness and first-run advantages. Therefore, Tencent needs to pay attention to whether WeChat Channels can establish a unique content ecology or attract well-known creators to bring their fans to this platform.

WeChat should increase its support for content creators, because merchants alone cannot maintain the healthy development of the ecosystem. Although most merchants have products, they often lack the ability to produce high-quality and unique content. The prosperity of the community is inseparable from the active participation of influential creators and media accounts.

The progress of the platform should not only pay attention to corporate users, but also to the increase of individual users and their interaction with content creation. The increase in the number of KOLs (influencers) is closely related to the diversification of content, and the rich content ecology will further promote the development of the KOL economy. The content creators of WeChat Channels are mainly ordinary people or small family businesses with grassroots characteristics. Tencent is facing the complex challenge of striking a balance between content quality and the KOL effect, while promoting the common development of both. If Tencent decides to continue focusing on content related to daily life, it needs to ensure a continuous increase in the number of users.

Tencent is gradually improving its ecosystem through WeChat Channels, but progress is slow. In contrast, Douyin collects transaction data and tags consumers through Internet celebrities promoting products, thereby attracting brands to advertise. At the same time, WeChat Channels currently has only a few top KOLs and lacks a large number of middle-level KOL groups. To improve this situation, Tencent needs to cultivate more top KOLs and establish a middle-level Internet celebrity group to produce more content. This process may take 1 to 2 years.

Culture & Organisation

There is still room for improvement in service quality and customer support, especially in the field of key account management. As a non-traditional e-commerce company, Tencent still needs time to accumulate experience in areas such as infrastructure, warehousing, and distribution.

Tencent has decided that the internal team will be independently responsible for the function development of WeChat Stores in the future, and will no longer open related work to third parties (see part 2 of this report). The user activity and penetration rate of mini programs are very high, and most users are concentrated in the hands of third-party service providers. These third-party service providers need to guide users to jump from mini programs to WeChat Stores to increase transaction volume.

WeChat’s strength is also its weakness

WeChat and specifically its leader, Alan Zhang, have always put user experience above everything. That’s why the app feels completely different from, say, Facebook or even Douyin. But this can also lead to internal clashes of interest.

WeChat search ad revenue in 2024 is about 3 billion yuan, and is expected to grow rapidly at a rate of 70%-80% in the next two years. However, the WeChat team strictly manages the delivery of search ads, and the current exposure rate of ads is about 10%. If the exposure rate increases to 20%-30%, it may affect the user experience. Similarly, the current loading rate of WeChat Channels ads is 4%. Although increasing it to 10% can potentially grow revenue, it may negatively impact the user experience and product quality.

As such, there are differences of opinion between the product team and the commercialisation team on the advertising delivery strategy. The commercialisation team tends to increase the number of ads to demonstrate profitability, but user experience remains the primary consideration. An excessively high ad loading rate may lead to user churn and shortened usage time, which is an unacceptable outcome. Therefore, striking a balance between increasing advertising revenue, including ads that drive traffic to WeChat Stores, and maintaining a good user experience is an ongoing challenge.

When WeChat Channels had just launched, the WeChat Channels, WeChat Pay, and Tencent Advertising teams collaborated closely, meeting face to face every month, and WeChat Channels shared a wealth of data. Initially, they hoped to replicate Douyin’s e-commerce success. But the cooperation proved difficult to operate and did not last long. Tencent Advertising focuses on generating revenue and is therefore most motivated to introduce brand merchants and increase GMV quickly. In contrast, WeChat must consider the ecological health of WeChat Channels and usually does not set clear numerical expectations when promoting a business. At a meeting, when the advertising department proposed to set a clear sales target, the WeChat Channels team asked, "Why do we need to set a target?" [2]

Such differences in concepts exist everywhere, for example, the speed of attracting business is much faster than the speed of building infrastructure. When the first batch of local services merchants settled in, WeChat Channels had not yet built a POI (geographic-based Points of Interest) system, and the content published by the merchants could not be accurately pushed to nearby users. [2]

In May 2024, Tencent Group adjusted the cooperation mechanism for live commerce, and the Tencent advertising team no longer engaged in live commerce operations and governance. All e-commerce-related businesses were handed over to WeChat and were managed by Zeng Ming, former head of the WeChat Open Platform. [2]

In May 2025, Tencent’s business group responsible for WeChat set up a new e-commerce department to explore transaction models within the app. Zeng Ming now leads the new department, reporting directly to WeChat Group’s President Allen Zhang. [3]

Staffing

Every e-commerce platform in the world that has achieved a GMV of over one trillion yuan currently relies on a large number of people to do the hard work. Douyin e-commerce built a team of more than a thousand people in the second year of its establishment. At its peak, Douyin e-commerce had more than 12,000 employees, and more than 6,000 of them were e-commerce ‘shop assistants’ who connected with merchants. [2]

Tencent has not yet proven its ability to develop an organisation with thousands of people to handle a large volume of basic tasks. The largest team in the gaming business has only a few hundred people. WeChat Channels has only a little over 300 regular employees. Even WeChat Pay and WeChat for Business rely mainly on a large number of service providers and partners when expanding and connecting with customers. [2]

Outlook

All in all, Tencent is facing lots of challenges with WeChat e-commerce. However, it is also actively seizing opportunities. WeChat has implemented several targeted strategies to address the slowdown in user growth and boost transaction volume.

The WeChat ecosystem launched a gift purchase function to stimulate transactions (see part 1 of this report).

WeChat transformed the WeChat Stores platform into a comprehensive e-commerce system that integrates multiple marketing strategies (see part 2 of this report).

WeChat has focused on promoting WeChat Channels and e-commerce businesses, integrating social media and shopping experiences to enhance user engagement. To improve its competitiveness, WeChat has helped merchants increase their influence on social platforms with the support of various tools and service providers (see part 2 of this report). WeChat also utilises the traffic from mini programs and WeChat Channels to direct users to WeChat Stores, thereby encouraging more merchants to settle in. This strategy not only attracts a large number of users to visit WeChat Stores, but also requires merchants to open stores here, further expanding the scale of the platform.

Compared with other major e-commerce platforms, the market share of the WeChat ecosystem needs to be improved. To meet these challenges, WeChat plans to increase the attractiveness of social media shopping by improving the user experience. It will continue to improve the mall system and enhance its social functions. WeChat will continue to explore various social e-commerce models, such as ‘Send Gift’. These measures will jointly influence user behaviour and are expected to improve WeChat Mall's market position, thereby driving the long-term growth of WeChat Stores and increasing market share and user activity.

Leveraging WeChat Channels

WeChat's commercialisation strategy for WeChat Channels is unique. They pay more attention to the development and survival of brands in their ecosystem, rather than simply pursuing traffic or advertising fill rate. WeChat's e-commerce model is not limited to live broadcasting, and it is expected to evolve into a diversified and comprehensive e-commerce ecosystem in the future.

By 2025, WeChat Channels live broadcasts are expected to become the primary source of WeChat e-commerce revenue, potentially accounting for over 80%. This is mainly because the infrastructure of WeChat e-commerce has not yet fully matured, and most of the transaction volume still depends on WeChat Channels live broadcast.

Tencent estimates that the average daily usage time of WeChat Channels users may increase to about 2 hours in the next 3 to 5 years. This estimate is based on several key factors: the content format is gradually moving closer to the Kuaishou model, there are multiple channels for traffic diversion within the WeChat ecosystem, and the platform is constantly optimising its algorithms and content strategies. Although the current user experience has not yet achieved complete immersion, it is likely to reach a usage time of 2 hours as the functions and ecosystem are gradually improved.

The total number of WeChat users is about 1.4 billion, with an annual growth rate of between 1% and 2%. Drawing on the experience of the rapid development of Moments from 2012 to 2015, Tencent believes that WeChat Channels will reach the target of 900 million to 1 billion daily active users between 2025 and 2028.

Improving traffic to WeChat Stores

Tencent views WeChat Stores as the cornerstone of its e-commerce strategy, leveraging social media resources to enhance the e-commerce ecosystem. Tencent's 2025 plan focuses on optimising its ecosystem and improving the overall level of WeChat e-commerce. By 2025, the target scale of mini-program e-commerce is expected to reach nearly RMB 2 trillion, with the gift function anticipated to generate RMB 15 billion in new revenue.

Tencent is actively promoting the diversified development of WeChat e-commerce, as described in part 2 of this report. It aims to guide users to make purchases in WeChat Stores by optimising the traffic distribution mechanism, including enhancing advertising, search functions, social recommendations, and gift functions, to build a healthier e-commerce ecosystem.

Tencent's e-commerce strategy will focus on WeChat Stores and enhance its functions. This includes integrating resources such as WeChat Channels, search engines, content platforms (such as "Little Green Book"/”Take a Look”, WeChat’s answer to Xiaohongshu), advertising systems and private domain traffic to enhance the strength of WeChat Stores. The design concept of WeChat Stores will be more concise, with a primary focus on facilitating transactions. Tencent has introduced functions such as membership management, providing more opportunities for small stores to grow and develop.

Tencent has very high expectations for WeChat Stores. In two earnings conference calls in the second half of 2024, Tencent President Martin Lau repeatedly emphasised that Tencent ‘repositioned the live e-commerce business to make it closer to WeChat e-commerce.’ In other words, Tencent aims to build an ecosystem that goes beyond WeChat Channels and livestreams, creating an e-commerce platform within WeChat and connecting it to the entire WeChat ecosystem. [4]

At present, the transaction volume of WeChat Stores is still small compared with the existing mini programs. WeChat Stores has a clear development plan for the next few years. By 2025, it will focus on improving infrastructure, such as increasing the merchant settlement rate. 2026 is a key year, with plans to cultivate Internet celebrities in the first half of the year and attract brands to settle in the second half of the year.

WeChat Stores is expected to take more than two years to make significant progress, and it is expected to take about five years for WeChat Stores to reach the transaction scale of the current mini programs. This process takes time and continuous efforts, but WeChat Store is moving steadily towards this goal. In the future, the ecosystem may prioritise allocating traffic to WeChat Stores over third-party mini program stores.

Targets

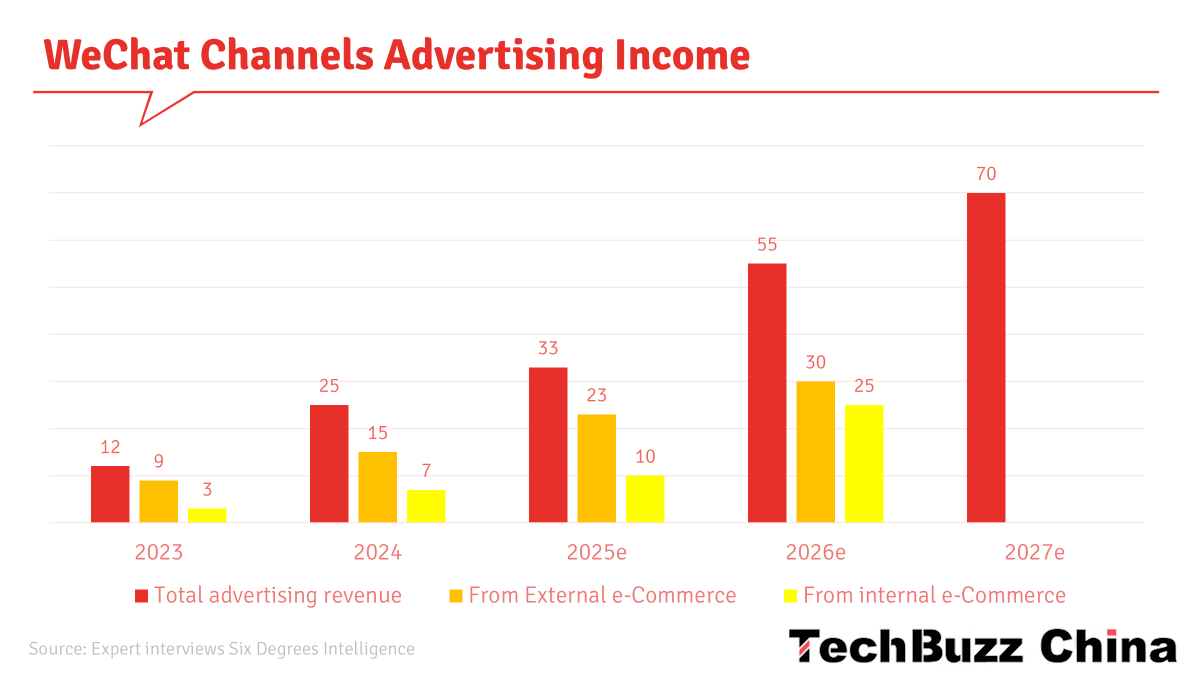

The advertising revenue on WeChat Channels will continue to grow strongly in the coming years. The ad load rate of WeChat Channels (currently 3-4%) is expected to gradually increase in the next few years, and it may take 3-4 years to reach the target level of 8%-10%.

Part of this advertising revenue concerns closed-loop e-commerce, which refers to merchants directly opening stores on the WeChat platform and promoting them through various WeChat Channels. It should be clear that this does not include third-party platforms such as Pinduoduo and JD.com. Looking ahead, the closed-loop commercial advertising revenue for WeChat Stores is expected to almost double from RMB 11 billion to RMB 20 billion in 2025.

The RMB 2 trillion GMV mentioned in Tencent's 2024 financial report covers the transaction volume of third-party mini programs, micro-businesses, and instant retail mini programs. These transactions incur a commission from Tencent, typically 0.6% of the transaction amount.

WeChat Stores aims to increase GMV from RMB 150 billion to RMB 300 billion or more. The gift-giving function has already made a significant contribution to the growth of WeChat Stores' GMV, bringing a 5%-10% increase. The gifting function is particularly prominent during holidays, with GMV accounting for up to 10%, while it usually fluctuates between 5% and 10% during regular days. However, the actual effect of the gift-giving function is not as revolutionary as the outside world imagines. WeChat does not regard it as a disruptive product internally. The primary objective of launching this function is to cater to users' needs for quick gift-giving on special days, rather than competing with other platforms like Douyin.

The development prospects of WeChat Channels are optimistic. At present, many brands have not yet joined the WeChat Channels ecosystem, and WeChat's focus this year is to build the business model of WeChat Channels gradually. The industry expects that its total GMV may reach RMB 1 trillion by the fourth quarter of 2026.

In the next one to two years, if the total e-commerce transaction volume of WeChat Channels exceeds 50% of Tencent's total e-commerce transaction volume, this may be inconsistent with Tencent's overall strategic goals. Tencent's vision is to build a comprehensive and diversified e-commerce platform through social, traffic, WeChat Channels and private domain capabilities, rather than relying solely on live broadcast or advertising revenue.

New marketing strategies

WeChat is strengthening its marketing efforts, and the gift-giving activities during the Spring Festival are just the beginning. Tencent plans to increase revenue and customer loyalty by launching a paid membership program. Members will enjoy a number of exclusive benefits, including discounts, priority purchase opportunities, free shipping services, and more. It will categorise membership levels based on the amount and frequency of customer consumption and provide corresponding graded services for members at different levels. Additionally, it will provide data analysis and precision marketing services to paying business customers. This includes detailed operational reports and big data marketing tools to help customers optimise product selection and marketing strategies.

Merchant migration

Tencent is implementing a phased strategy to introduce external e-commerce customers into the WeChat Stores system gradually. First, they will migrate lower-tier merchants, because the non-brand characteristics of these customers make the migration process relatively simple. The second group of migrated customers may be leaders in the domestic market. Starting from the third batch, Tencent may begin to handle the migration of international brand customers. Tencent's ultimate goal is to guide most of its customers into the system with WeChat Stores as the core, with only a few exceptions. Top luxury brands and some large enterprises can still choose to use mini programs as their e-commerce platform. This strategy allows Tencent to gradually optimise the migration process while also providing appropriate solutions for different types of customers.

Migration work on lower-tier merchants started in March and is expected to last until the end of the year. The second phase is expected to be carried out in the third and fourth quarters. Other batches will continue after completion, and the progress may be accelerated in the future. This phased migration may have a short-term impact on advertising revenue growth, but the outlook remains positive in the long run. The conversion rate of WeChat Stores may not be higher, but the cost of mini programs (including costs of service providers, see part 2) is higher, and Tencent thinks the overall effect may be better after the migration is completed.

In WeChat's e-commerce system, the mini-program store business may gradually lose its importance and even face elimination. In addition, the industry has a negative attitude towards the future development of mini programs in integrating online sales functions.

AI & Deepseek integration

WeChat is developing a project called AIAgent, which aims to build it into a personal AI assistant and a large AI platform. An essential feature of this project is that the search function is used as the main entrance. The unique advantage of WeChat search lies in its rich ecosystem of mini-programs, which can directly provide users with comprehensive services.

Traditional search results usually include public accounts, WeChat Channels accounts and related articles, while today's AI systems can directly generate answers. For example, when searching for ‘lipstick’, AI can provide usage guides and suitable skin types. This AI-generated content brings new advertising opportunities. When a user searches for ‘10-day tour guide to Europe’, AI will not only provide daily itinerary suggestions but also recommend air ticket discounts. In this process, platforms like Tongcheng and Ctrip are likely to engage in commercial cooperation and recommend ticket booking services. This business change, driven by AI, provides new ways to make advertising profitable, especially in the field of search engines. Although other industries may also adopt similar advertising push methods in the future, the effect is not very significant at present.

Another key function of WeChat AIAgent is the ability to use users' personal information for AI training, including Moments, chat records, favourites, and other private data within the WeChat ecosystem. Based on this data about users' interests and hobbies, AIAgent can provide personalised recommendations. For example, if a user is travelling and likes Impressionist art, AIAgent may recommend related exhibitions to them. WeChat's data ecosystem is diverse, accurate, and privacy-protected, which gives WeChat a unique advantage in providing personalised services. In this way, the WeChat AIAgent project leverages WeChat's ecosystem and user data to deliver highly personalised intelligent services to users.

The release of DeepSeek may bring new tools to merchants, including AI-powered voice customer service. Although DeepSeek's customer service system relies on WeChat for Business, it may not be deeply integrated with WeChat Stores. Merchants can use DeepSeek for free to generate various marketing copy, but they need to learn how to use it by themselves. Tencent may combine DeepSeek with the Hunyuan model to enhance the search function and redesign the logic of user tags and product matching.

With the help of optimised algorithm models, Tencent is expected to improve the accuracy of product recommendations and the efficiency of traffic distribution, thereby increasing advertising opportunities. In addition, DeepSeek may introduce features similar to Baidu, which generates content to answer users' questions, thereby extending users' usage time and increasing user stickiness. Looking ahead, by 2025, DeepSeek is less likely to be deeply applied on the merchant side, but will be committed to optimising traffic distribution and user matching.

And what does the competition think?

The information in the three parts of this report has largely been taken from more than 10 people close to Tencent and service providers. We would like to close with the opinion of a competitor.

A (former) Alibaba Operations Expert shared: “Tencent's WeChat Channels platform has great development potential in the e-commerce field. If it receives sufficient attention, it could expand to more than half the size of Douyin. However, in the next two to three years, Tencent's commercialisation strategy for WeChat Channels may be cautious, and its growth rate is expected to be relatively slow.”

“Compared with its competitors, Tencent has not introduced influencers on a large scale in the fields of social and shelf (search-based) e-commerce, which may become a disadvantage. In addition, WeChat Channels is currently not as good as Douyin in marketing and traffic conversion. However, in the long run, if Tencent continues to invest in WeChat Channels, it has the potential to become a strong opponent of Alibaba and Pinduoduo.”

Key Takeaways & Summary Video

Here are 10 concise key takeaways from the report:

Tencent's e-commerce revival through WeChat aims to monetise the app by integrating its ecosystem (mini programs, Channels, public accounts, search) with WeChat Stores, where transactions will take place.

WeChat Stores face significant challenges in market competition, including attracting traffic, marketing, and consumer awareness, as well as a clear video viewership market share gap compared to major competitors like Douyin and Kuaishou.

Tencent's core objective is to change user consumption habits on social media, as shopping stickiness on WeChat is not yet fully formed, with most orders currently driven by livestreams or influencers.

The user profile for WeChat Channels is primarily comprised of adult women aged 35-60 from second-tier and third-tier cities, indicating an older demographic than Douyin users and highlighting a need to attract younger groups.

User experience (UX) and visibility are compromised by the lack of a dedicated entrance for WeChat Mall, unlike Douyin Mall, which affects traffic flow.

Despite rapid GMV growth on WeChat Channels, its absolute value is still significantly lower than that of its competitors, and major brands are cautious about advertising due to a lack of proven ROI mechanisms and platform instability.

The platform struggles with a lack of accurate user profile data and content diversity, leading to ineffective advertising and a very low average e-commerce advertising ROI of 0.1%.

Internal organisational conflicts exist between product teams (prioritising user experience) and commercialisation teams (focused on revenue), which slows down the adoption of aggressive monetisation strategies.

Staffing is a significant constraint; WeChat Channels operates with only around 300 regular employees, a stark contrast to competitors like Douyin, which had over 12,000 e-commerce employees at its peak.

Tencent is strategically leveraging WeChat Channels to be the primary source of e-commerce revenue (expected to account for over 80% by 2025) and plans to migrate merchants to WeChat Stores, while integrating AI (AIAgent, DeepSeek) to enhance search, recommendations, and marketing.

The following summary video was created using Google Notebook.

Sources

This article has been compiled from an analysis of exclusive expert interviews within the Six Degrees Intelligence network, supplemented by insights from the articles listed below.

Images by Tech Buzz China’s Ed Sander, unless stated otherwise. These images may not be reproduced without Tech Buzz China's prior consent.

[1] 36Kr 2025-01-10 [2] Latepost 2024-12-03 [3] Yicai 2025-05-15 [4] 36Kr 2024-12-19