What’s up with…? - Part 4: Douyin Local Services

An update on ‘the torturous trench war’ with Meituan

Introduction

In March last year, we wrote an in-depth article (Food Fight! Douyin’s local services business) about the way Bytedance’s Douyin short video app (TikTok’s Chinese sibling) had started to offer local services to its enormous reach of approximately 800 million Chinese users. After first incorporating e-commerce in the app, in-store group buying deals and even takeaway meals were a new way to monetize the app. As such, it has encroached on the territory of Meituan, which reacted by adding livestreams to its local services platform.

This update will describe what happened since we last wrote about it in March. Not only is it a perfect case showing how Chinese internet companies never stay ‘in their own corner’; it also shows us a possible future of TikTok, which in many ways is following the exact roadmap of Douyin.

This post is part 4 of our series on updates about some of our 2023 topics. Since some of these updates are shorter in size compared to our regular reports, we have temporarily switched to a weekly publication schedule. This post is a paid subscriber-only post.

Freya Zhang and Ed Sander, Research Editors

Rui Ma, Consulting Editor

(click on the images above for information on the Tech Buzz China team)

Douyin local services (抖音生活服务)

A follow-up to Food Fight! Douyin’s local services business - March 17 2023

It’s not strange that Bytedance started showing an interest in the local services market as a new way to monetize Douyin. This market was RMB 19.5 trillion in 2020 and is expected to grow to RMB 35.3 trillion by 2025. According to iResearch, the penetration rate is only 12.7%, so there’s much room for growth. [1]

According to a former Meituan employee, the online share of the local services market is about RMB 2 trillion, of which the in-store business (online purchased coupons being redeemed in offline establishments) is RMB 1.4 to 1.5 trillion. Meituan once held more than 60% market share in this online in-store segment.

In late April 2023, Douyin shared that its local services GMV 2022 had grown sevenfold compared to 2021. It had exceeded RMB 77 billion, while advertising revenue reached RMB 8.3 billion, meeting its 2022 goals. [3] Local services contributed 30% to Douyin’s total revenue in 2022. [2]

In Q1 2023, the monthly GMV of Douyin’s local services was RMB 10 billion. Food delivery, however, remained just a small fraction of that; its GMV was only RMB 100 million in January and February 2023, which wasn’t substantially better than the pilot in 2022. [3]

2023 timeline

Since March, Douyin has been adding many new store categories, trying to cover all aspects of life. Still, most of GMV is contributed by large chain merchants, accounting for a much bigger proportion than we see at Meituan, which has a strong position among small and medium businesses. Small businesses miss the marketing budget to promote themselves on Douyin and/or have no time or skills to make their own content or livestreams. [3]

At the end of March, a few weeks after we wrote about Douyin’s ventures into local services and food delivery services, the app launched a dedicated ‘Mall’ (商场 Shāng chǎng) section in the app. In this ‘Mall’, users can purchase group-buying discounts they need to redeem at offline businesses, comparable to Meituan’s in-store business. Merchants include amusement parks, fitness schools, photography services, laundry services, supermarkets and convenience stores. [1]

From January to May, the number of merchants on Douyin’s local services increased by 54%, livestream orders increased by 61%, the number of livestreamers by 134%, and the number of service providers (see below) by 39%. [4]

In May, food delivery became a stand-alone division within the Douyin organisation, on the same level as travel and in-store catering, with the vice president of local services overseeing the unit. [5]

In May, Douyin Local Services also launched an app called ‘Douyin Sales Help’ (抖音销帮 Dǒuyīn xiāo bāng). It mainly provides leads and performance-tracking tools to Bytedance employees and service providers. [6]

After rapid GMV growth in 2022, local services saw a slowdown in growth rate in 2023. During the pandemic, merchants had chosen to advertise on Douyin to survive and were willing to give up some of their profits through group-buying discounts. When the pandemic ended, some became more reluctant to continue their spending on the app. In Q1 2023, GMV did not meet Douyin’s internal expectations. In April, there was a short uptick when users bought coupons for the upcoming May 1st holiday, but sales dropped again in May. [8]

By June, two years after launching its first food delivery experiments, Douyin started offering food delivery as an independent section in the app under the ‘Same city’ menu instead of only lumping it in with the group-buying offers. Clicking on the link will take users to a mall page with information on merchants. Besides offering keyword search, merchants can be sorted and filtered by delivery speed, delivery costs and distance. This upgrade made the service easier to find for users and reflected the growing importance of food delivery for Douyin. [4]

From June 16th to 18th, Douyin Local Services organised its first large-scale celebrity livestreams to promote the 618 shopping festival. GMV reached RMB 226 million. [7]

The hotel & travel GMV in June could be broken down as follows:

A Douyin Local Services Operations Manager shared that GMV reached RMB 21 billion in May, RMB 26 billion in June (of which RMB 7 billion in the hotel & travel segment) and RMB 31 billion in July, and they were expecting similar figures for August and September and a seasonal slowdown in Q4.

By mid-2023, Douyin had 400,000 merchants in the hotel & travel business and expected to grow this to 600,000 by the end of 2023.

Still, the travel business's development speed was slow compared to (in-store) catering and fell short of expectations. Compared to catering, the supply of merchants in the travel segment is more concentrated in Meituan and Ctrip. Douyin upgraded the travel business to the same level as in-store to help it grow. [9]

Douyin’s in-store and travel business equalled 40% of Meituan’s transaction volume, down from 45% six months earlier. [9]

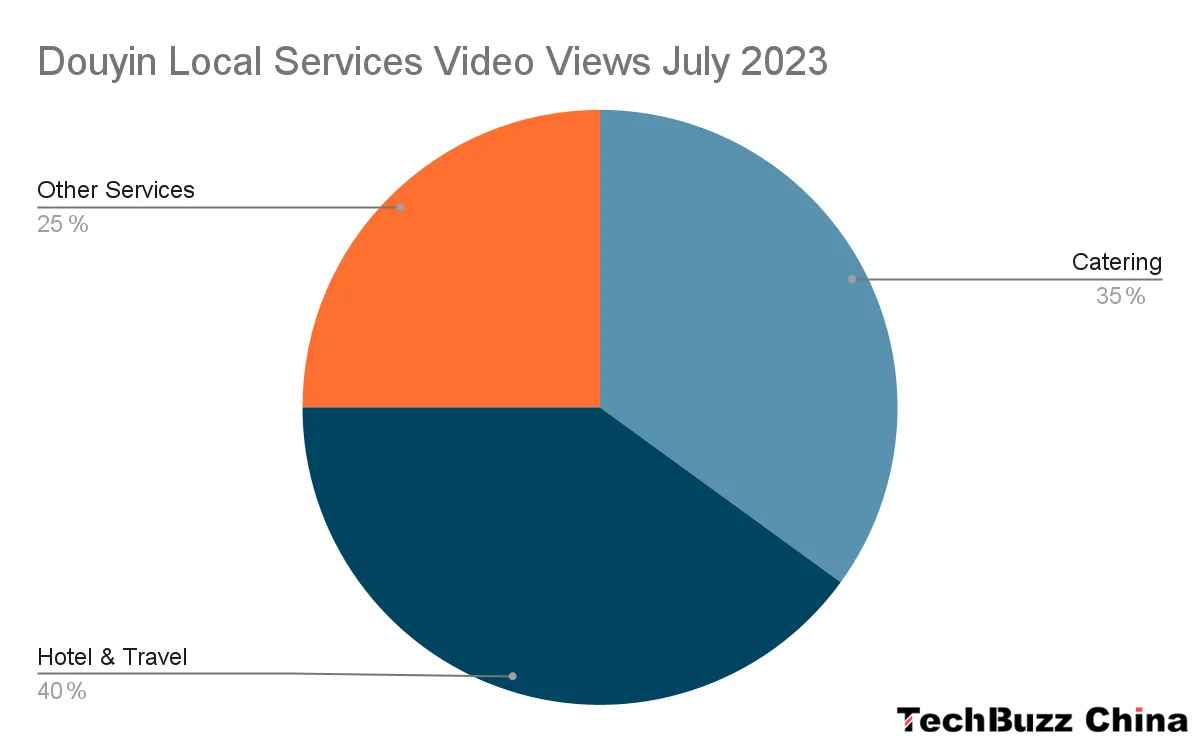

In July, Douyin saw 8 to 9 billion local services-related video views. These broke down as follows:

While it might not grow as fast as 2022’s sevenfold increase anymore, the GMV of Douyin’s total local services exceeded RMB 100 billion in the first half of 2023. This was mainly driven by in-store business and travel business. Douyin’s 2023 target for these two businesses was said to be RMB 290 billion. [8] It was hoping to grow them to RMB 400 billion in 2024.

Douyin wants to become a go-to place for shopping, travel and eating to increase the number of times users open the app. Food delivery, therefore, remains an important initiative. Douyin found some merchants reluctant to offer in-store group-buying deals on the app because of fear it might hurt their takeaway business on Meituan. If Douyin can also offer food delivery options, these merchants would be easier to convince. [9]

But food delivery had continued to disappoint. The full-year GMV target for food delivery at the beginning of 2023 had been RMB 100 billion, but was later adjusted to RMB 5 billion. [16] In 2022, Meituan’s food delivery GMV had been RMB 94 billion.

In September, there were rumours that Douyin would give up its food delivery business, which Douyin denied. It stated that since July, the food delivery business had been fully launched in Beijing, Shanghai, Chengdu, Guangzhou, Changsha, and Linyi. Douyin is said to have introduced a regional agency model that it planned to expand to other cities. [10] Sure enough, on September 11th, Douyin announced expanding food delivery to 24 new cities, bringing the total to 30. The new cities included first-tier cities, directly-governed cities and provincial capital cities. [11]

At a conference in September, Douyin shared that local services search traffic has increased by 254% in the past two years. [12] Douyin's local services were available in 370 cities with 2 million partner stores. [13] Note, though, that those figures were identical to those the company shared at an April conference.

In December, Douyin released a ‘fine dining’ guide for 14 first- and new first-tier cities. New first-tier cities make up a selection of 15 larger cities (often provincial capitals) that have grown to resemble first-tier cities in recent decades. Douyin’s guide lists 170 outlets that offer ‘quality catering services’ and seems a response to Meituan’s comparable ‘Black Pearl Guide’. Most of the outlets in Douyin’s guide operate short videos on its platform. [14]

In 2024, Douyin reported that the GMV for its local life services had grown 256% in 2023 and hosted 4.5 million merchants in 370 cities (note, still the same number of cities as in April, but more than double the number of merchants). Transactions from livestreams had grown 570%, while those from short videos grew 83%. [15]

If companies start stating growth in percentages, it often points toward an attempt to hide the absolute figures because they are disappointing. This could well be the case here too. If the previously stated GMV of RMB 77 billion for 2022 is correct, then Douyin reached a GMV of close to RMB 200 billion in 2023. Impressive, but well short of the RMB 290 billion that Douyin had set for itself. Considering that the GMV for the first half of the year had been RMB 100-110 billion, this would also mean there was no incremental growth in the second half of the year.

Creators

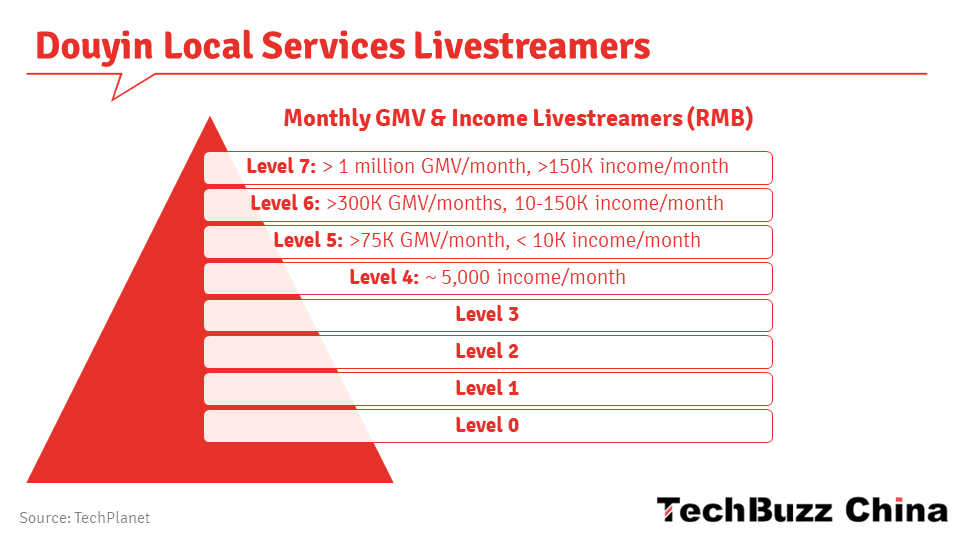

The number of local services content creators (influencers making short videos/livestreams to promote merchants) on Douyin has also grown. It reached 12.35 million in 2022, a year in which they created 1.1 billion videos. 72% of merchants on Douyin local services have searched for matchmaking with such creators. [17]

As in any livestream business, some creators make enormous amounts of money, from RMB 50,000 to RMB 300,000 per month. Some creators get paid for ‘store visits’, which range from unpaid (well … a free meal …) to RMB 5,000. Besides the business they make from merchants, creators often take on apprentices for training, charging thousands of yuan for their services. Others, with few fans, only make a few thousand yuan monthly. Creators who have signed contracts with MCNs (Multi-Channel Networks) must share part of their commission with the company. [17]

Douyin talents are divided into seven levels:

Level 5 experts charge only RMB 200-300 for a store visit. [17]

As the number of shop explorers on Douyin increases, the traffic per creator gets less, and it becomes increasingly harder to get to the next level of the pyramid above. In 2021, getting to level 5 or 6 was still easy as there were relatively few group-buying creators. Nowadays, the support from Douyin is not as strong. Commissions given to creators by merchants have also decreased from 15-20% to 10-15%, while some top merchants have moved from short videos of store explorations to livestreaming. [17]

Creators sharing store visit videos at fast food chain Wallace, linking to group-buying deals.

But finding a creator to cooperate with is often not sufficient for a merchant…

Service providers

Douyin doesn’t have as strong a business development team on the ground as Meituan does. Therefore, it uses local third-party service providers who take the role of ‘business assistants’, creating short videos and operating livestreams for local businesses that don’t have the necessary skills. They also provide product selection and content planning. Meituan and Ele.me also depend on such external parties to help their merchants. [18]

Douyin has been using service providers since it launched local services in May 2021. At the end of 2022, it already had more than 100,000 service providers supporting its merchants. Merchants can use so-called ‘special service’ service providers for short-term needs like short video creation, store decoration or livestreams. Another option is to hire a ‘whole case operation’ agent for more long-term, all-around needs. Especially in lower-tier cities or small counties, service providers become ‘digital guides’ or ‘online business partners’, helping local businesses create online channels for promotion and sales. [18]

Douyin emphasizes content creation and user interaction, which require creativity and resource investment. While service providers do help unskilled merchants, all of this also adds to their costs. An MCN (livestream agency) revealed that if one includes the service provider fee, expert store visit fee, investment costs, etc., the overall costs of Douyin are now higher than with Meituan. [19]

The number of service providers and creators is expected to increase, which should lower costs because of stronger competition among them. Douyin expects merchants’ costs to drop by approximately 20%. Still, some merchants have started bypassing service providers and doing local service group-buying business alone. [17]

With the growing number of service providers, monitoring their quality and effectiveness has become crucial. For instance, Douyin screened its service providers in June and July, reducing the number for its hotel and travel business from 20,000 to 10,000 to improve service quality. Douyin also rates service providers with a star system. The higher the rating, the more resources are available to them in the Douyin ecosystem. [18]

Douyin also does not want to depend entirely on service providers. By mid-2023, it had 1,300 people working in its business development teams and wanted to expand this to 3,000 by the end of the year.

Regarding food delivery, in the 30 cities where Douyin is active, it uses 150 regional agents to give onboarding and operational support to merchants. On top of this, delivery services are provided by other third parties like Dada and SF Express. [11] One Douyin service provider revealed that Douyin has asked its service providers to build their own delivery capacity, but this has not been implemented yet. [2]

Meituan fights back

According to a former strategic planning manager of Meituan, Douyin was able to quickly gain market share because it could provide better marketing services for short-term explosive growth to new merchants. Traditional platforms of Meituan and Alibaba (Ele.me) are less equipped for this.

It took a while for Meituan to wake up to the reality of Douyin’s local services business. Only when some of its key accounts started turning to Douyin and had remarkable results through livestreams did Maituan become worried. It also started showing in Meituan’s results: normally, the difference in the growth rate of commission and advertising income is about 5%, but in Q4 2022, Meituan’s advertising income was actually 18 points behind its commission growth (13.6%). [19]

In an internal meeting in April, Meituan announced it would also launch delivery of group-buying deals in more than 20 cities as a defensive strategy against Douyin. [3]

After some testing in 2022, Meituan officially started livestreams (‘Meituan Live’ 美团直播) on its app in April 2023. But the real turning point came in June, when Meituan found that - although the playback rate was lower than on short video apps - the average conversion rate of livestreams was 30-40%, higher than the industry average. [21]

In July, livestream content was promoted to first-level access on the Meituan app and saw RMB 500-600 million GMV that month. It quickly rose to RMB 1 - 1.2 billion in August and RMB 2 billion monthly GMV in October. [21]

While growing strongly, Meituan Live’s GMV only makes up a small share of its total GMV: at the end of June 2023, Meituan’s rolling 12-month transaction volume was around RMB 1.8 trillion. [21] It’s also limited compared to Douyin, who saw a GMV of RMB 31 billion for local services in July.

In 2022, many Meituan employees were still pessimistic about a fight with a short video app that has 800 million users. Now, they think the arrival of Douyin was a good thing since it pushed them to invest heavily in new initiatives like livestreaming. The Meituan group now has a livestream centre that all businesses can use. [9]

The approach of Douyin and Meituan differs though. Meituan prefers to build its own livestreams to attract traffic. Douyin, on the other hand, earns commissions and advertising fees from livestreams. Traditional search-based platforms like Meituan cannot easily copy Douyin’s content-based e-commerce systems.

Meituan’s takeaway business has two livestreams, the monthly Shenquanjie (神券节) and the daily Shenqiangshou (神抢手). Livestreams for in-store business are divided by product categories (travel, beauty, etc). The main focus is on official livestreams and a selection of large nationwide chains. Coupons bought in these in-store streams must be redeemed offline at the concerned stores, while coupons for takeaway can be deducted from an online order. The coupons help conversion but require merchants to give large discounts and the platform to provide traffic subsidies. [21]

Meituan has not set an annual target and is focussing on improving basic livestream capabilities and formats and on increasing merchant participation. 3-5% of stores are now taking orders through livestreams. Based on the active number of merchants by the end of 2022 (9.3 million) the number of participating merchants is at least 300,000. [21]

Merchants can have one livestream and open it to all cities with stores. Users will be directed to the nearest store when a coupon is bought. To attract merchants, Meituan’s official livestream currently does not charge slot fees, while it charges almost no commission to merchants that do their own livestreams. When the scale of merchants and GMV grows, Meituan will implement paid livestreams and commercialize them. [21] Until then, the new livestream initiatives come with significant costs for Meituan. In Q3 2023, the company’s sales & marketing expenses grew by more than 56%, far exceeding revenue growth. Meituan Live accounted for at least part of this increase. [19]

When a merchant’s sales reach a certain level, Meituan will refund part of the commission to encourage them to sell better-priced products. Meituan sales staff also try to convince merchants who are also active on Douyin that they also need to offer the same deals on the Meituan app. Sales staff must also provide the sales of both Douyin and Meituan by individual merchants for their performance evaluation. [9]

Regarding prices, in mid-2023, about one-third of Meituan’s offerings were cheaper than Douyin’s, with the remaining two-thirds being only slightly more expensive than Douyin. Products on Meituan Live, especially in catering, were usually cheaper. Hotel and travel deal prices were generally comparable, while Douyin’s prices for scenic spots and five-star hotels were slightly lower.

While Meituan used short videos and livestreams to attract users, it implemented subsidy policies and mobilized local promotional teams to expand its market influence. This did, however, not prevent Douyin from claiming an incremental market. At the same time, Meituan lacks rich and high-quality content in the battle with Douyin. It will be a challenge for Meituan to find a successful way forward.

Still, Meituan’s launch of livestreaming has had a positive impact on its business model. For merchants, it provides free or low-cost promotion while attracting more consumers. For Meituan, it increases user stickiness. In the longer term, it could offer Meituan new advertising revenue. Currently, Meituan Live is mainly used by large chain merchants, partially because small merchants lack live stream resources.

Some Meituan employees believe that Douyin Local Services has reached a bottleneck but has not yet formed consumption habits. It might need to invest more for smaller profit increases. An optimistic judgement at Meituan is that Douyin might have taken some of Meituan’s merchants but that the impact on GMV has been limited, and Douyin is actually helping ‘educate the market’ in lower-tier cities. Meituan might be able to make up for lost users in this ‘sinking market’, a difficult market Meitian had previously abandoned around 2019. [22] According to Douyin, 80% of people that merchants attract on Douyin are new customers. [7]

While Meituan has lost some market share to Douyin, it remains above 55%. Meituan has approximately 3.5 million merchants in the catering sector and 1.4 million in the ‘comprehensive’ segment (other merchants like karaoke, beauty, fitness, etc). Including the merchants in the travel sector, Meituan had 9.3 billion merchants at the end of 2022. Douyin claims to have 4.5 million merchants at the end of 2023.

With an 83% redemption rate for coupons, Meituan also still does better than Douyin’s 62%. [20]

A ‘torturous trench war’

The battle for local services between Douyin and Meituan will not end any time soon, if Zhang Chuan, president of Meituan’s in-store business, is to be believed. In a New Year’s memo full of militant language, he stated that the company is now catering to people looking for low prices and fast delivery instead of just applying a search-based consumer approach (‘shelf commerce’) aiming for ‘comprehensive + high quality’, or in other words ‘more and better’. [19] As such, Meituan is also stressing the need for inexpensive products on its platform, as Alibaba and JD did last year.

Meituan has introduced ‘special price group buying’, which features highly favourable prices for a small number of SKUs. It targets Douyin’s low-price group purchase packages for the top 50 brands in a city and tries to achieve an even lower price for the same brand. It’s one of Meituan’s fastest-growing in-store businesses in the past half year. In Q3 2023, the daily order volume exceeded 3 million, and it's the main source of new users for Meituan. [19]

Meituan’s business development staff is asked to focus on proactive pricing with merchants instead of the old strategy of growing the number of merchants. In some 3rd and 4th-tier cities, Meituan has changed the agency model to a direct operation model to control merchants better. [19]

A former Meituan manager expects the profit margin of Meituan to decline due to a full-blown subsidy war among various players competing for a larger market share. Meanwhile, advertising revenue may drop to one-third of its original level because of competition with Douyin and Xiaohongshu. If Douyin decides to enter the food delivery market seriously, Meituan’s profit margins might decline further.

According to Zhang Chuan, the battle for local services will be a ‘torturous trench war’. He said the internet is entering a new stage of competition for existing users in which every platform must offer local services, and Meituan’s opponents are getting stronger. He seems to be right: Douyin is not the only newcomer…

New players

Seeing the strength of the combination of video and local services, other players have also gotten interested.

At the end of March, WeChat Channels was also testing functionality to sell coupons.[1] It formally launched them in May, with leading merchant brands like Burger King, KFC and McDonald's rolling out group-buying coupons on WeChat Channels livestreams. In the example of Burger King, customers can either buy in-store coupons or deals for home delivery (RMB 6-7 delivery fee, 30 30-minute delivery time). WeChat Channels promotes local services in two ways: through coupons in short videos and in livestreams. This is comparable to what you’ll find on Douyin. WeChat Channels only charged a 1% commission during the initial launch stage. [23]

Kuaishou and Xiaohongshu have also taken steps into local services. Xiaohongshu launched store visit cooperations in July. Kuaishou increased the group-buying subsidies. [17] Some of Kuaishou’s group purchases, including KFC and popular hotpot chain Haidilao, now offer home delivery if the merchant can arrange delivery. [24]

Even Pinduoduo is considering getting into the local services business. In mid-December, Pinduoduo’s community group buying division, Duoduo Maicai, launched promotional work for local services like in-store dining vouchers, in-store hotel vouchers, attraction ticket vouchers, movie tickets, etc. For its launch, Duoduo Maicai focussed on third-tier cities where Douyin and Meituan don’t have a strong position. [22]

Pinduoduo already mobilized staff for an R&D team that was to develop a system of apps and Mini Programs. It also planned to launch local services using Duoduo’s 3,000-strong business development team. Pinduoduo prioritised recruiting more merchants and convincing them to participate in activities. As it normally does when launching new initiatives, it asked for 0% commission and offered simple operations.[22]

A Duoduo Maicai employee interpreted the launch as confirmation that the community group buying battle between Duoduo and Meituan Select had ended, and the Duoduo staff needed a new battle to maintain their (in)famous fighting spirit and efficiency. [22] (We’ll get back to the state of community-group buying in a future Tech Buzz China post.)

Meituan is on its guard about the possible arrival of Pinduoduo since Duoduo Maicai’s structure and products are relatively similar, and both are based on search-based logic, compared to Douyin’s content-based logic. Pinduoduo’s field staff is also stronger than Douyin’s. Still, successful experience in e-commerce, based on the overcapacity of manufacturers and low-price goods, does not automatically mean potential success in local services. [22]

The original plan was to launch local services nationwide after Spring Festival in February. But plans obviously changed. In the last week of 2023, recruiters were ordered to halt the project until further notice. At the start of 2024, Pinduoduo announced that the local services project, which was supposed to become Duoduo Maicai’s second growth curve, was completely halted. [22]

A former Meituan manager said that the arrival of platforms like Douyin, WeChat Channels and Xiaohongshu on the local services market has had several impacts:

They bring incremental market share, often without much influence on the existing customer base. In other words, their arrival results in more new online users and a higher penetration of online local services.

Merchants need to spend more on marketing, raising questions about business sustainability.

Platforms often favour large merchants in traffic distribution, making it difficult for small merchants to obtain enough traffic, thereby reducing their market efficiency.

Into 2024: Douyin + Ele.me?

In 2024, increasing user penetration is Douyin’s main goal for local services. Its monetization rate is expected to rise from 3-4% to 4.5%.

Douyin’s income in local services comes from commissions, advertising fees and cooperation with MCNs and experts. However, because of Meituan’s strong position, Douyin is facing continued losses in local services. A former Bytedance senior operations expert claimed that Douyin’s local services achieved positive net profits in Q3 2023 but were expected to generate losses again in the following period due to increased business expansion costs and market competition.

Still, leadership has set a goal for Douyin local services to become profitable in 2024. If that fails, local services might go the same way as Douyin’s game, PICO and education divisions…

Douyin is still in the verification stage for local services, especially for the food delivery business, which faces low retention rates and low brand awareness. It has no obvious advantages compared to other market players. Douyin may consider acquisitions to develop its food delivery business. This brings us to the recently rumoured attempt by Bytedance to acquire Alibaba’s Ele.me.

The rumours, which started surfacing in December [25], became a bit more believable on the 14th of January when respected financial media outlet Caijing reported, based on multiple sources, that Alibaba and Bytedance had been discussing a sale of Ele.me Alledegly, Alibaba wanted to sell its food delivery service at a price of $7.5-8 billion for the full Ele.me business (and all its staff), but Bytedance only offered $7 billion for the food delivery unit. Ele.me denied the news. [16]

Alibaba bought Ele.me for $9.5 billion in 2018, and former chairman Daniel Zhang once said that the local services market was a ‘must-win battle’ (with Meituan). Not only did Ele.me fail to win the battle, it has also remained unprofitable, although losses have been narrowing as the number of orders grew by 20% last year.

Some Alibaba sources now think that AMap (a.k.a. Autonavi or Gaode) is doing better than Ele.me and is now their main local services business. [16] A sale of Ele.me would decrease the financial burden on Alibaba.

Within Alibaba, some people consider Ele.me ‘baggage’ in the company's split-up and transformation. Others consider its instant retail capabilities (see our article Need for Speed: Instant Retail) very important and think that a sale of Ele.me would damage Alibaba’s local services business. [16]

As described in last year’s article, Douyin has been partnering with Ele.me for operations in food delivery since August 2022.

It remains to be seen if this deal comes through. It would be a big win for Douyin in its attempt to make food delivery work. It now depends on third parties or a merchant’s delivery, which tends to be inferior to those specialised services of Meituan and Ele.me. At the same time, while some Alibaba staff and shareholders might applaud the sale of Ele.me, it also is another loss of face for the Hangzhou conglomerate in a series of retracted spin-offs and IPOs of the 1+6+N split-up.

For Meituan, food delivery is the high-frequency service that drives exposure to other services with lower frequency on its app. If Meituan loses food delivery business to Douyin, hurting its in-store and travel business. [9] The combination of a possible acquisition of Ele.me by Bytedance and the threat of Duoduo Maicai’s market entry probably keep a few Meituan people awake at night.

2024 should be an interesting year…

Key Takeaways (no pun intended)

During 2023, Douyin Local Services showed impressive growth, although it does not seem to have reached internal targets. The results of food delivery, however, have been disappointing. While the GMV of Douyin’s in-store and travel business has equalled more than 40% of Meituan’s, food delivery goals for 2023 got stuck at single digits per cent of Meituan’s.

Food delivery growth is hampered by the lack of delivery services that Douyin can offer to merchants. This explains its interest in buying Ele.me from Alibaba.

Douyin’s local services are built around content. To help merchants create short video and livestream content Douyin has set up a network of content creators and service providers.

The arrival of Douyin local services meant merchants had to start providing short videos or livestream content, something that hadn’t been necessary on Meituan. This has driven up the business costs for merchants, who often need to hire content creators and service providers because they lack the necessary skills.

Meituan has started Meituan Live, a channel with livestreams and short videos, as a defensive strategy against Douyin. While the share of total GMV remains limited, it has shown significant growth since it was officially launched in April 2023.

WeChat, Kuaishou and Xiaohongshu have taken steps into local services too. According to a Meituan manager, all platforms will eventually need to offer local services, so competition will only increase.

Especially larger chains promote local services through video on the platforms, making it more difficult for smaller merchants to stand out.

Pinduoduo’s Duoduo Maicai platform launched local services in December but quickly halted this new initiative. If PDD decides to roll out local services, it would be a formidable new competitor to Meituan because their business models are very similar.

In Q3 2023, the business units showed profitability but fell into losses again in Q4. Douyin management has set a goal for local services to become profitable in 2024.

Sources

Six Degrees Intelligence, a leading global expert network/quantitative research firm that operates in China. Augmented with information from the articles below:

[1] Tech星球 2023-03-29 [2] 36氪未来消费 2023-10-12 [3] 36氪未来消费 2023-04-28 [4] Tech星球 2023-06-13 [5] Pandaily 2023-12-27 [6] Tech星球 2023-05-31 [7] 36Kr 2023-06-29 [8] 晚点LatePost 2023-08-07 [9] Latepost 2023-07-11 [10] Pandaily 2023-09-04 [11] Tech星球 2023-09-12 [12] Fung Business Intelligence 2023-09-14 [13] Fung Business Intelligence 2023-09-21 [14] Technode 2023-12-21 [15] Technode 2024-01-04 [16] 财经十一人 2024-01-14 [17] Tech星球 2023-08-21 [18] Tech星球 2023-09-14 [19] 36氪未来消费 2024-01-08 [20] Equal Ocean 2023-03-30 [21] 36氪未来消费 2023-12-04 [22] 晚点LatePost 2024-01-03 [23] Tech星球 2023-05-25 [24] Tech星球 2023-11-10 [25] Reuters 2023-12-19 [26] China Money Network 2024-01-16

Images from by Tech Buzz China’s Ed Sander unless stated otherwise. These images may not be reproduced without prior consent by Tech Buzz China.