Need for Speed: Instant Retail

How the pandemic accelerated a new growth market for e-commerce

Table of contents

Things that caught our attention

Things that caught our attention

Chinese Premier Li Qiang met representatives from China's biggest internet companies. The meeting came after the National Development and Reform Commission praised several Big Tech firms for their investments. The closing of the investigation into Ant Group is seen as a softening of the government’s stance against Big Tech. (Source)

Earlier this year, we wrote about Douyin's moves into the local services market and how Meituan had started defensive tactics. Meituan has now started internal tests for an in-app livestream function called Meituan Live. (Source)

Meanwhile, Douyin has reorganised its local services business and elevated its hotel and travel business division to a first-level department under its lifestyle services business, on par with its in-store services. (Source)

And as if the local services market wasn’t heating up enough yet, Pinduoduo launched a local services portal on its main app. Currently, it mainly includes the sale of food and beverage coupons and self-pickup. The products sold are mainly concentrated in chain catering brands such as Wal-Mart, KFC, McDonald's, Starbucks, Luckin Coffee, Burger King, Pizza Hut, DQ, Heytea, and Haagen-Dazs. (Source, link in Chinese)

This month, both Alipay and WeChat Pay have opened up their apps to foreign credit cards. Read more about this and the instructions how to link them, so you can use them on your next trip to China in the Pekingnology newsletter.

Introduction

Recently, we published an article about Alibaba's Hema (Freshippo) supermarkets. Hema is one of the most successful examples of ‘new retail’, the merger of online and offline retail. But Hema is also an example of ‘instant retail'.

In this new article, our most elaborate report to date, and a future follow-up, we will dive deeper into this fascinating sector that exploded during the Covid years and has many different business models and players.

Free subscribers can read the first chapter defining instant retail and its three main categories. Paying subscribers can read the full article, including an extensive analysis of some of the main players in one of the main business models.

Freya Zhang, Ed Sander & Rui Ma

(click on the images above for information on the Tech Buzz China team)

Key Takeaways

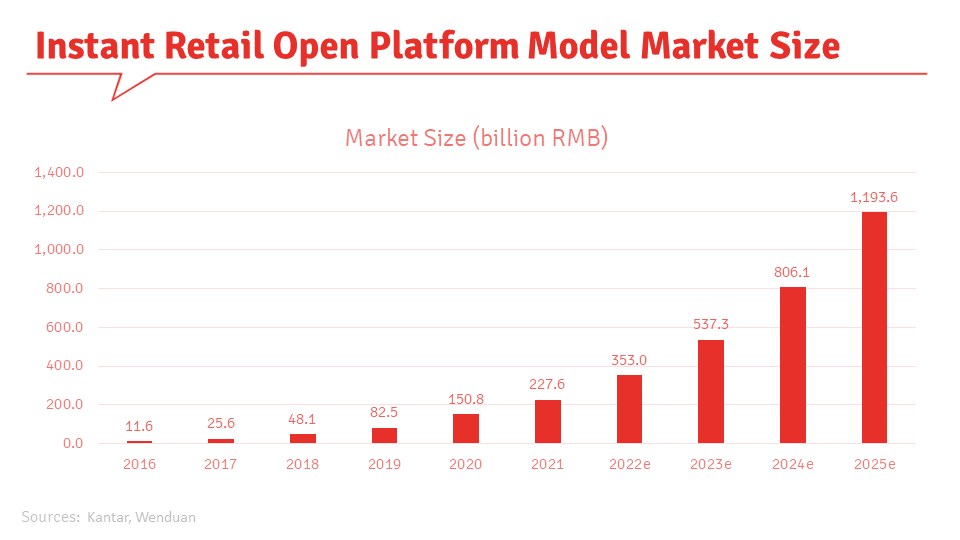

Under the influence of the pandemic, growth of Instant Retail has accelerated. The market is expected to further grow to RMB 1.2 trillion in 2025.

Two meal delivery companies, Meituan (#1) and Ele.me (#3) have diversified into delivering any product. However, despite similarities in bringing products from A to B, several factors make goods delivery more complex.

Number 2 in the market, Dada Nexus, is a cooperation between courier platform Dada Kuaisong and Jingdong spin-off JD Daojia. JD Daojia has recently been integrated into the main JD app and is one of JD’s main growth engines.

JD Daojia is strong in the large supermarket and hypermarket sector, while Meituan sees more prominent business with small and medium sized store.

Instant retail can increase the customer base of offline stores substantially. However, it’s hard for smaller merchants to make money through instant retail. Delivery costs and service fees to platforms eat into their margins and often forces them to charge higher prices on the platforms than in their shops. Merchants have to participate or potentially lose business to their competitors.

Meituan offers merchants an alternative to ensure higher profit margins: lightning warehouses.

It is uncertain if there is as much demand for instant retail in the ‘sinking market’ as in 1st and 2nd tier cities. Still, Meituan and JD Daojia are making strong inroads.

None of the marketplace platforms discussed in this article was profitable yet in 2022. But they claim to be close to break-even.

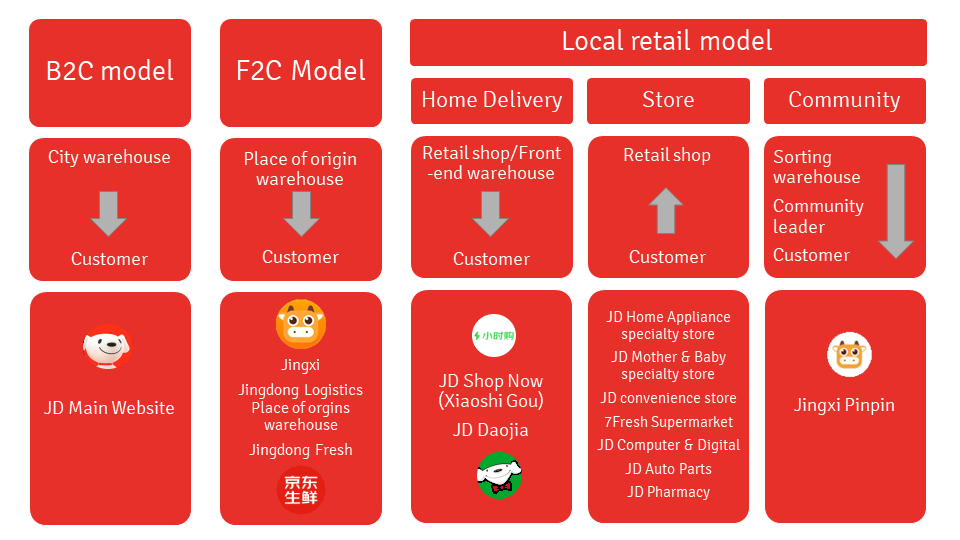

What is ‘instant retail’?

Since the arrival of e-commerce, the speed of delivery has been continuously improving, first from 10 days to 3 days and later to next-day and even same-day delivery, like when JD.com started shipping from city warehouses. People’s need for speed has evolved together with this trend, or maybe it is the other way around.

Research by Accenture showed that more than 50% of post-95 consumers expect to receive their online orders the same day or even within half a day. But they have also become more rational and pay more attention to prices. Research by Beijing Normal University shows that 70% of young people take costs as their first consideration. Frequent promotions have also taught consumers not to stock up on too many consumable products as they used to do in earlier days when such price discounts were much less frequent.

With the myriad delivery options available to the Chinese consumer, the concept of ‘instant retail’ (即时零售 jishi lingshou) can be somewhat confusing. It refers to offline stores (supermarkets, convenience stores, department stores, etc.) and warehouses that are home-delivering orders that nearby consumers place online. In other words, instant retail combines local brick-and-mortar stores with instant delivery. Instant retail has upgraded the consumption motivation of traditional e-commerce from ‘product’ to ‘product + time + space'.

The app that consumers order on can either be a physical store (chain)’s own app (e.g. RT-Mart’s or Walmart’s app), a large self-operated webshop or a third-party marketplace platform (e.g. JD Daojia). Delivery to consumers in a radius of 3-5 kilometres is normally done within 30-60 minutes.

Instant Retail is sometimes called ‘On-Demand Retail’ or ‘Near-Field Retail’. ‘Near-field’ refers to fast delivery within an hour from a shop nearby, as opposed to ‘Middle-Field’, which is same or next day delivery from a warehouse in or near the city and ‘Far-Field’, which refers to delivery in 1-3 days from a warehouse further away (e.g. purchases on Taobao and Tmall).

Indeed, the e-commerce market can be categorised into multi-day delivery (Tmall, Taobao, Pinduoduo, etc.), next-day delivery (JD.com, community group-buying, Tmall Supermarket, etc.) and same-day delivery (Meituan, JD Daojia, Ele.me, Hema, etc.). Same-day delivery models that take longer than an hour are, strictly speaking, not instant retail, and neither are models that deliver goods the next day or where consumers have to go pick up the products somewhere (e.g. community group buying).

Alibaba, for instance, has, over the years, built several different solutions that cater to different target groups with different needs, often prioritising either speed or inexpensive goods. For instant retail, it has Hema and Ele.me, while Taoxianda and Alibaba-owned RT-Mart (part of Sun Art, which is largely owned by Alibaba) can deliver within the same day, normally within half a day (but sometimes faster). RT-Mart has hundreds of stores, warehouses, regional food processing centres, and suppliers. These also support other parts of the Alibaba ecosystem like Taoxianda, Tmall Supermarket and Taocaicai.

Image from Alibaba 2021 Investor Day

The idea behind instant retail is that it brings the busy (or lazy?), mostly young consumers, more convenience while the store or retail chain expands its service radius from 500 m - 1 km to several kilometres, thereby increasing its potential number of customers exponentially (an increase from 1 to 5 kilometres can lead to a 24-fold increase in potential customers). Through instant retail, a store can also compete with pure online players. What's more, merchants that can offer instant delivery can improve the brand image of their stores.

Instant retail can deliver faster product turnover (owing to higher conversion rates and higher consumption frequency) and higher regional marketing efficiency. Conversion rates are high because most instant retail users have a strong purpose for purchasing. Traditional e-commerce has a conversion rate of 5-10%, while instant retail sees 15-20% conversion. Regarding frequency, Kantar research found that customers that have tried O2O (online-to-offline) will show a 17% increase in FMCG purchases, mostly through higher purchase frequency. Considering these advantages, instant retail is considered a more efficient brand sales channel than traditional e-commerce.

Instant retail is basically quick home delivery for anything but meals. While takeaway food delivery by the likes of Ele.me and Meituan Waimai has been popular for many years, instant retail expands the same principle to any physical product from any store. Although one might think that instant retail doesn’t differ much from food delivery, they are actually worlds apart. Unlike food delivery, instant retail concerns products with a high degree of standardisation. On the other hand, the number of SKUs is much larger (for many stores, around 10,000) than the dozens of menu options that can be ordered from restaurants. These all need to be digitised for the online platforms. Furthermore, instant retail also comes with challenges in warehousing, order picking and keeping products undamaged, synchronising online and offline stock levels, returns, etc.

Instant retail used to be a solution in case of emergencies, but now it has become another shopping option. Linkshop mentioned several advantages that physical stores have compared to online ones and which they can capitalise on through instant retail:

Consumers have a higher degree of trust in the authenticity of products with offline stores than with online stores, especially those in their own neighbourhoods.

When a few years ago, pre-sales periods were introduced for Double 11 consumers had to wait a long time for online purchases to arrive. Buying deals through instant retail enables consumers to almost immediately enjoy their purchases.

For merchants, the traffic costs on the instant retail platforms are lower than on traditional e-commerce due to location variables (less competition in a limited area).

Products

Research by Meituan showed that instant retail is often used for goods with high immediacy (e.g. need for freshness like with fruit or impulse buying like with snacks) and low portability (think heavy bags or bottles of rice and cooking oil). Because of their high frequency, repeat purchases and fast consumption, instant retail fits FMCG quite well. According to Kantar Consulting, instant retail has brought 15% pure incremental growth to FMCG, and its growth rate of 65% is faster than other omni-channels.

Instant retail can be a more efficient model for certain products, like perishable food or products that need cold chain logistics when delivery takes longer than an hour.

High-frequency, low-value, and immediacy-based standard products are the main products. The main product categories of instant retail include fresh food, snacks and beverages, flour, oil, rice noodles, daily fast-moving consumer goods, etc. Most of the categories that are dominated by instant retail have low (traditional) e-commerce penetration rates, like groceries and fresh food.

Instant retail doesn't only provide fast delivery; it can also handle those products that traditional e-commerce isn't good at. Traditional e-commerce is particularly suitable for three types of products: those with high unit prices (allowing space for saving money through discounts), long consumption cycles and, therefore, low purchase frequency (durable goods) and non-standardized products (resulting in many different SKUs). Offline retail categories, and thereby instant retail, show the opposite characteristics: low unit price, standardised demand (products might not be standardised - think of different sizes of fruit - but the needs they fulfil are) and high consumption frequency.

A few statistics:

Instant retail for casual snacks had a penetration rate of 4.6% in 2021 and is expected to grow to 13-14% in 2025.

The penetration rate for fresh food in 2025 is estimated to be 15%.

The penetration rate for FMCG goods will also be relatively high.

Meituan Flash Shopping sales data from October 2022 showed that non-food products had a higher growth rate (90%) than food products (44%). Still, the penetration rate is expected to be only 8% in 2025.

The penetration rate for high-priced products like 3C is expected to be 5% in 2025.

Shoes and clothing are less compatible with instant retail.

Due to the low motivation to stock up, products with small quantities, small packages, and low unit prices are more compatible with instant retail, and such specifications often have higher gross profit margins.

Customers

According to data from iResearch, the post-85s and post-90s account for about 65% of instant retail users. The core instant retail users are 26-40 years old (accounting for 79% in 2020) and mainly live in high-tier cities (taking snacks as an example, users in first-tier and second-tier cities accounted for 76% in August 2022).

The number of instant retail users was estimated to be 300 million in 2021. As with meal delivery, changes in economic and demographic structure have driven the development of instant retail demand. But instant retail isn't simply an extension of meal delivery, and while meal delivery users have a higher probability of using instant retail, it's expected that instant retail will eventually have a bigger potential target audience. The ceiling is estimated to be 550-640 million users, which is higher than the number of meal delivery users (544 million in 2021) but lower than those of traditional e-commerce (842 in 2021). Some consumers do not or seldomly order takeaway meals because of health and safety concerns, but instant retail provides standardised products for home cooking. Moreover, instant retail meets more diverse consumption scenarios than planned meals (breakfast, lunch, dinner).

Still, the usage frequency of a single consumer and, thereby, the total number of orders could be significantly lower than that of meal delivery. The average order value is, however, expected to be significantly higher.

Three instant retail models

Three main models for instant retail deliver in one hour or less.

Self-operated ship-from-store model

Self-operated front-end warehouse model

Marketplace for offline retailers model

Let’s look at what sets these three apart.

Self-operated ship-from-store model

In this model, orders are picked in a store and the warehouse of the store (for fast-movers) and delivered by the store's own delivery service. Supermarkets already have the necessary logistical 'cold chain' in their own stores to keep products fresh. They only need to add couriers with styrofoam boxes to get the products to the consumer.

This model includes Alibaba’s Freshippo (Hema Xiansheng) and JD’s equivalent 7Fresh. Hema designed its stores so that store staff assigned to different parts of the store can use handheld devices to collect online orders. Bags containing these goods are placed in a transport system under the ceiling and transported to the warehouse at the back of the store. There, bags belonging to one order are consolidated, and the full order is handed over to the Hema couriers who are waiting behind the store. A Hema store is both a supermarket and a fulfilment centre. You can see for yourself in this video ChinaTalk.nl made several years ago.

Hema couriers receive deliveries at the back of a store.

The couriers deliver the orders to the customer within half an hour and within a radius of 3 kilometres (in China, regular supermarkets have a service area of 500 metres to 1 kilometre). Instead of opening more stores in cities it is already active in - which would require significant investments - Hema has recently decided to expand the delivery radius of certain stores to reach more potential customers.

Since we discussed Hema extensively last month, we won’t discuss this model at length in this article.

JD.com uses the same principle in its 7Fresh supermarket (Hema's CEO Hou Yi used to work for JD but moved to Alibaba when his idea for Hema was rejected at JD).

Some RT-Mart hypermarkets have been refurbished and use the same order-picking and fulfilment system as Hema. Consumers place their orders for the nearest Sun Art branches through Alibaba's Taoxianda or Ele.me platforms or through Sun Art's own platforms RT-Mart Fresh (Da Run Fa You Xian). When 50% of sales come from online orders, it makes sense to integrate stores and warehouses in the way Hema, RT-mart and 7 Fresh have done.

The self-operated front-end warehouse model

In this model, a platform runs its own front-end warehouses (small distribution centres close to the consumer) and delivers within an hour in a 3-kilometre radius. Examples include Meituan Maicai, Dingdong Maicai and the defunct MissFresh. These platforms self-operate purchasing, storage and delivery and are, therefore, basically retailers. Tech Buzz China first discussed this model in podcast episode 58: China Grocery E-Commerce: Bloodbath or Gold Mine? in 2020.

The front-end warehouse model has proven difficult to operate without enough scale because of the high investments in fixed assets like warehouses and self-operated logistics. Spreading resources too thinly can lead to disaster. Two major players in this market, Dingdong and Missfresh, both had their IPO in 2021. Missfresh had to scale back and faced problems paying loans, salaries and suppliers. It lost so much of its value that it has been asked to delist. Meanwhile, Dingdong had to scale back by leaving many provinces and focusing on those that showed (potential) profitability. Meanwhile, another player, Pupu Supermarket, continues to expand and is rumoured to seek its own IPO.

There’s a lot to learn from these cases. We will go back to the front-end warehouse model in a future article. For now, the rest of this article will focus on …

The marketplace for offline retailers model

This business model involves marketplaces that do not stock goods themselves but facilitate trade between consumers and retailers through their apps. The assortment of offline retailers is made available in the platform's app, and the platform normally also arranges for orders to be collected from the store and delivered to the consumer. Companies using this model are Dada Nexus/JD Daojia, Meituan (Shangou) and Ele.me. The latter two have expanded their services from food delivery to delivery of any products.

During the pandemic, even ride-hailing market leader Didi Chuxing provided similar services. For Meituan, Didi and Ele.me, the business model has similarities to their original business of meal delivery and ride-hailing. It's all about facilitating moving someone or something from A to B.

With the marketplace platforms, stores normally charge for delivery (examples we've seen were 4-5 RMB or 50 to 65 cents) and sometimes for packaging as well. Some merchants do not charge any delivery fee but will have around 10% higher prices than in the stores. Others charge RMB 5-10 for delivery and have minimum order values of around 100 yuan.

Getting enough merchants on the platform is essential. The more merchants in an area, the more orders, the lower the average delivery time and costs, the better the user experience.

In the early years of instant retail, many large supermarket chains built their own platforms and delivery logistics (the aforementioned ship-from-store model). Very few were successful. Nowadays, most choose to hand these tasks over to professionals and work with one or more of these marketplaces.

The advantages of the marketplace model lie in the fact that it does not feature self-operated retail and is a non-competitive cooperation with retailers.

(Note: the section below is only available to paid Tech Buzz China subscribers)

The Market

In 2022, instant retail became ‘the new darling’.

In July 2022, the Ministry of Commerce released the Report on the Development of China’s Online Retail Marketing in the First Half of 2022. The report, which mentioned the concept of ‘instant retail’ for the first time, said that with the integration of online and offline, new consumption models like instant retail were developing fast. In August 2022, CCTV broadcasted a 10-minute report about instant retail (if you understand Mandarin, you can watch it here online).

In its prospectus, Dingdong Maicai estimated the instant e-commerce market size of the fresh food category to be RMB 79 billion in 2021. But instant retail covers more categories than just fresh food. According to Meituan's estimates, the scale of the instant retail-related market was about RMB 150 billion in 2020 and RMB 350 billion in 2021. This corresponds to 0.6% and 1.2% of the offline retail sales of commodities. In 2025, Meituan expects the market size to be around RMB 1,018.2 billion, with a penetration rate of about 3.3%.

In 2022 Dada Group, China Chain Store & Franchise Association and JD Research Institute for Consumption and Industrial Development published the White Paper on the Open Platform Model of Instant Retail. It pointed out that the O2O home delivery business model had been a driving force in retail in the previous years, with a compound annual growth rate of 64% from 2016 to 2021. The platform model of instant retail was growing even faster, with 81% in the same period. The report estimated the 2025 market for instant retail to be RMB 1.2 trillion large, with 100 billion annual orders. Another report expects instant retail to grow at an annual compound growth rate of 36% up to 2025.

Growth of instant retail (and other forms of grocery delivery) has been partially stimulated by the covid restrictions in which people in some cities could not go to stores during certain periods (because of lockdowns) or preferred not to go out because of worries about infections. As long as platforms could increase their supply (merchants and products), their order volume and GMV would certainly increase. Still, the pandemic also caused problems on the supply side and some stores were ordered to close by the government. Platforms had to work with the government to arrange guaranteed supply.

Instant retail also played a more prominent role during the Double 11 (Singles Day) shopping festival in 2022. According to Meituan, the number of 3C stores participating in last year's Double 11 festival doubled compared to 2021. JD Daojia’s Shop Now sales increased by 80% YoY. Many product categories like digital products, baby care, home appliances, home improvement and alcohol saw even higher growth rates.

The following trends are taking place in the instant retail market:

Products bought through instant retail have expanded from supermarket categories to all product categories. For instance, JD Daojia has expanded to 3C digital, furniture & home furnishing, baby & children's clothing and other sub-categories. This has improved average order values and margins.

User profiles have expanded from young females to all types of consumers.

The platforms become more involved in the retailers’ operations. They transition from supplying online traffic, fulfilment and delivery to systematic solution providers, offering user research, supply chain construction, marketing, after-sales and more.

Upgrading of technological infrastructure.

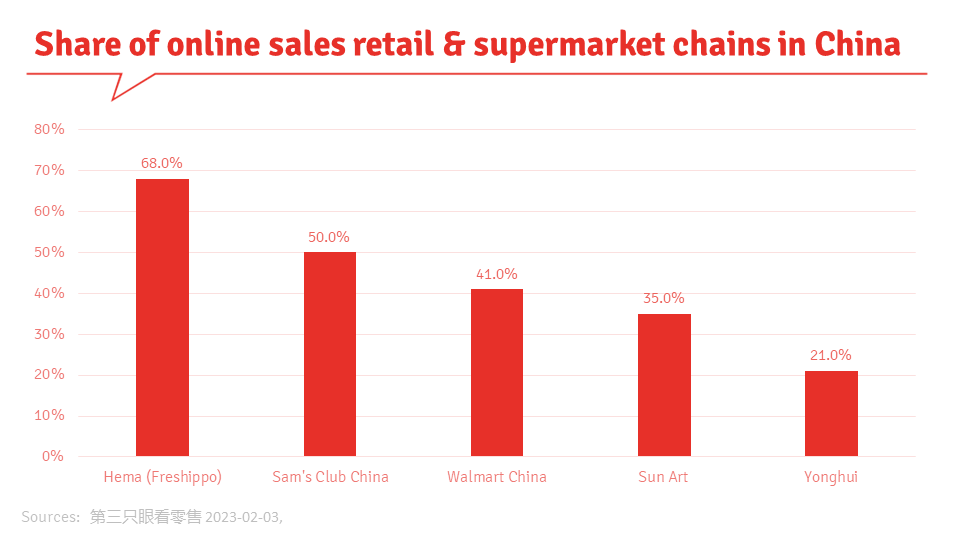

For retailers that have used instant retail, it can account for 20-30% of their total sales. For corporate stores, it can even account for up to 50%. Walmart Sam's Club's online sales accounted for more than 50%; Sun Art Retail's online business accounted for 35%.

Convenience Stores

During the pandemic, convenience stores saw 40% of their orders coming in online. While the share of online shopping has declined after the zero-covid policies were abolished, the behaviour of consumers has changed, and they have gotten used to the convenience of buying through instant retail.

With their high outlet density in large cities, high level of standardisation of products, strong localisation and good warehouse-store integration, convenience stores are among the first retailers that can enjoy the advantages of instant retail. Convenience stores normally have a service radius of 500 metres, with local office buildings and communities making up most of their customers. With instant retail, they can expand this to 3 km.

While some convenience stores build their own delivery system, most team up with JD Daojia, Meituan and Ele.me and find this a more cost-effective win-win. Acquiring more customers through instant retail also provides convenience stores with opportunities to launch membership programs and improve retention. At the same time, they need to keep an eye on their margins since additional costs (e.g. for staffing and platform and delivery fees) could evaporate the higher revenue and lead to losses.

There is also a clear need for convenience stores to join instant retail. According to the China Chain Store and Franchise Association, 67% of convenience stores saw a decline in number of visitors between 2021 and 2022. Remarkably enough, 64% of convenience stores saw their total sales increase in 2022. Despite the pandemic, sales of convenience stores have maintained a growth rate of more than 10% in the past three years.

For local convenience stores outside the 1st and 2nd-tier cities, it is also necessary to build a better defence against foreign-owned convenience store chains that are moving into the ‘sinking market’ (third-tier cities and below). They need to capitalise on their knowledge about the local area and its consumption preferences. Instant retail will also force local convenience stores, which often lack knowledge about doing business online, to think more about the digitization of their business. For instance, instant retail requires very accurate data on stock levels.

Instant retail in the sinking market?

Various convenience store chains, including JD Convenience Store and Lawson, and stores like Miniso and Watson have rapidly grown in the sinking market in Q1 2022. Meituan data also shows that from January to July 2022, instant retail orders in convenience stores in Guangxi province increased by 42% year-on-year. The increase was 119% at large supermarkets and at mom-and-pop grocery stores 317%.

But despite the impressive growth figures, there is no consensus on whether instant retail is a niche market for high-income consumers in high-tier cities or if it will reach a broader market. It is believed that if meal delivery can gain a foothold in the sinking market, instant retail will follow. The penetration rate in third-tier cities is expected to have an upper limit of 25-35%.

While in first- and second-tier cities, the average (large) supermarket sees 25% of its business arriving online, it remains in the single digits in the sinking market. Seeing the trends in bigger cities, many enterprises have started launching supermarket home delivery. But after the abolishment of zero-covid policies, home-delivery orders showed a sharp decline. Examples show the proportion of online orders dropping from 5% to 2%.

Even larger supermarkets in the sinking market often have limited staff working on the online business. What's more, generous subsidies that online platforms were giving merchants during the early stages of home delivery have largely disappeared as competition between platforms heated up and internet companies started focussing on profitability. With discounts disappearing, online goods have lost their price competitiveness for consumers.

Meanwhile, the costs of online business are about 10% of the sales price, of which platforms take 6-8%. Platforms also refuse to deliver large orders of rice and cooking oil, and the supermarkets have no control over the quality of the third-party delivery couriers, leading to untimely delivery and inadequate service.

Consumer demand for instant retail is not as high in the sinking market as in bigger cities. Population size and consumption habits restrict consumer power. In bigger cities, nightlife is an important driver of instant retail, but the sinking market does not have such a lively nightlife. Demographics in old urban areas, where mostly elderly consumers live, make the online performance of supermarkets even worse. Shopping in physical stores and picking up goods at community group buying leaders serve the needs of most consumers.

Finally, in-store business works better in the sinking market, where acquaintances are a stronger driver of local business, and shopping is a way for middle-aged and elderly to socialize. Shopping on an app can be considered just ‘cold transactions'.

Still, even with a smaller proportion of instant retail consumers, supermarkets in the sinking market must follow or lose part of their customers. Supermarkets need to focus on those consumer groups that use instant retail and increase their repurchase rate.

The Players

As with other grocery delivery business models, instant retail interests China's internet companies because groceries have a high purchase frequency, meaning consumers will open an app frequently, leading to potentially more sales in other categories. As such, we find the usual suspects active in this sector.

Meituan Flash Shopping and JD Daojia are the market leaders in instant retail, having 37% and 19% market share in 2021, respectively. They are expected to remain the top 2 players for a long time.

Meituan’s 2021 scale was RMB 60-70 billion, JD Daojia’s market size in 2021-2022 was RMB 49.1 billion, Ele.me’s market size was RMB 20 billion, and Taoxianda was RMB 10+ billion.

In this chapter, we will elaborate on the main players following the marketplace model for instant retail.

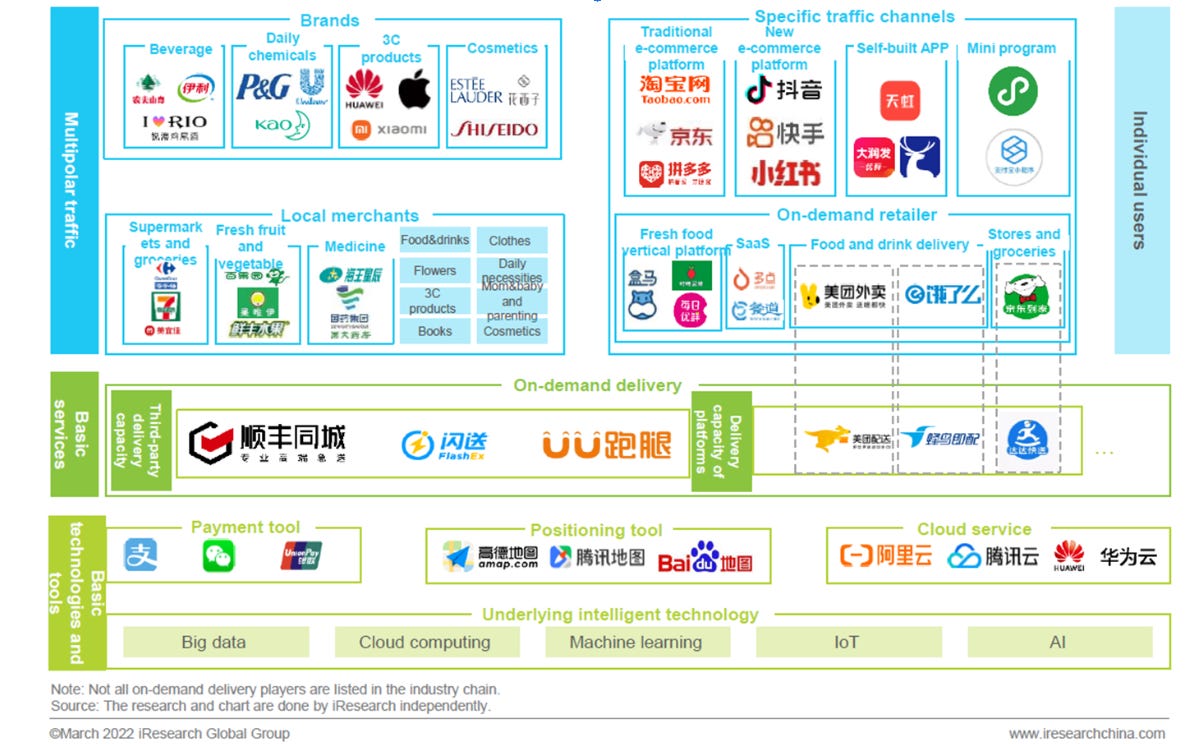

The Instant Retail industry chain. (Note: Pei Song, Fengniao and Dada Kuai Song are the local life delivery divisions of Meituan, Ele.me and JD Daojia respectively.) Source: iResearch Trends in China On-Demand Delivery Industry in 2022

Meituan Flash Shopping

Besides its food-delivery services, Meituan has three different business models for delivering groceries:

Meituan Grocery Shopping (美团买菜, Meituan Maicai). A self-operated front-end warehouse model launched in 2019, comparable to Dingdong Maicai and the faltering Missfresh. It promises 30-minute delivery and therefore is part of instant retail. We will cover Meitian Maicai in a future article on front-end warehouses.

Meituan Select (美团优选, Meituan Youxuan), a community group-buying model with next-day delivery and self-pickup, comparable to Duoduo Maicai (see our recent report on community group-buying for more information).

Meituan Flash Shopping (美团闪购 Meituan Shangou) is an instant retail platform that offers 30-minute delivery. Like competitor JD Daojia, it is not limited to supermarkets and groceries but also delivers from other retail stores.

For Meituan, fresh grocery e-commerce is a natural extension of its fulfilment system, extending from meal delivery to other categories. But Meituan Maicai and Meituan Select are still in the exploratory phase: they need warehouses and their own supply chain capabilities.

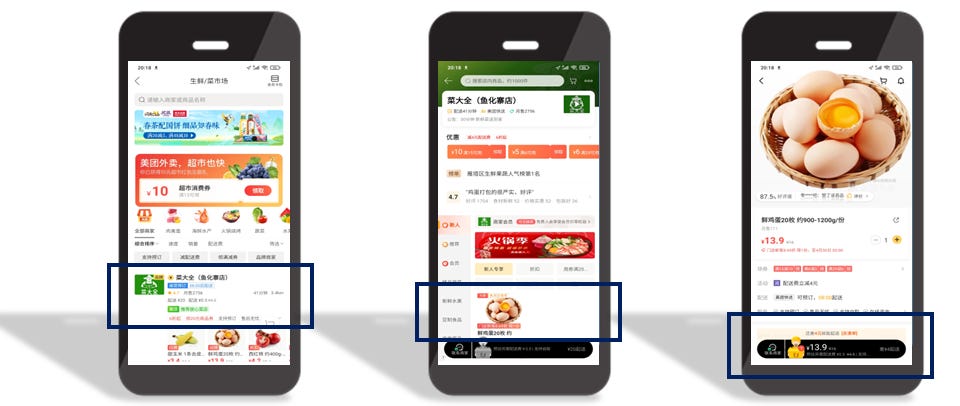

Meituan Flash Shopping (闪购 Shangou) was launched in 2018 as an independent spin-off from the food delivery business. Since 2016 retail brands have already been able to join the Meituan Waimai channel under the label "Quick Buy" (速购, sù gòu). Flash Shopping currently is Meituan’s fastest-growing business. Meituan’s takeaway customers highly overlap with the Flash Shopping customers. 41% of the users of Meituan are using Flash Shopping.

An early project of Flash Shopping was Cai Daquan (菜大全): setting up a franchisee counter in a vegetable market and selling goods purchased from market merchants on Flash Shopping. The project saw disappointing results because the franchisees added a 100%-200% margin. When Meituan limited it to 30%-40%, it got into conflicts with these franchisees. Moreover, results were limited by the opening hours of vegetable markets. Cai Daquan ended in failure.

At the end of 2020, it was split into three different units: Meituan Flash Shopping, Meituan Medicine and Tuanhaohuo (later renamed to “Meituan Haohuo” and later to “Meituan E-Commerce”). The latter is Meituan’s e-commerce platform.

As with other new business initiatives at Meituan, the development of Flash Shopping can be divided into three stages:

Brand establishment stage: establishing a project team or spinning off a new brand to explore the business model and run the business process, including WeChat connections. The number of merchants is still small. This stage took half a year, faster than normal, because Flash Shopping could use the existing meal delivery infrastructure.

Category expansion stage: scale up to reduce operating and distribution costs. Expand categories on the supply side. This was done between 2019 and 2021. Meituan expanded from supermarkets and convenience stores to verticals like mother & baby care, drinks, 3C, etc.

Refining operation stage: improving GMV and unit economics of consumers and merchants.

In the past, Flash Shopping did not have its own Business Development (BD) team and relied on support from the food delivery BD teams. But growth was weak since those did not have Flash Shopping included in their KPIs. Therefore Flash Shopping started piloting its own BD teams in cities like Changsha and Hefei.

In October 2022, Meituan reorganised its grocery delivery business. On the one hand, it offers "Tomorrow's Supermarket" (明日达超市, Míngrì dá chāoshì), which consisted of community group-buying business Meituan Select and Tuanhaohuo (团好货). As the name implies, Tomorrow's Supermarket offers next-day delivery. For faster delivery, there was the ‘Instant Supermarket’ consisting of Meituan Flash Shopping (Shangou) and Meituan Grocery (Maicai).

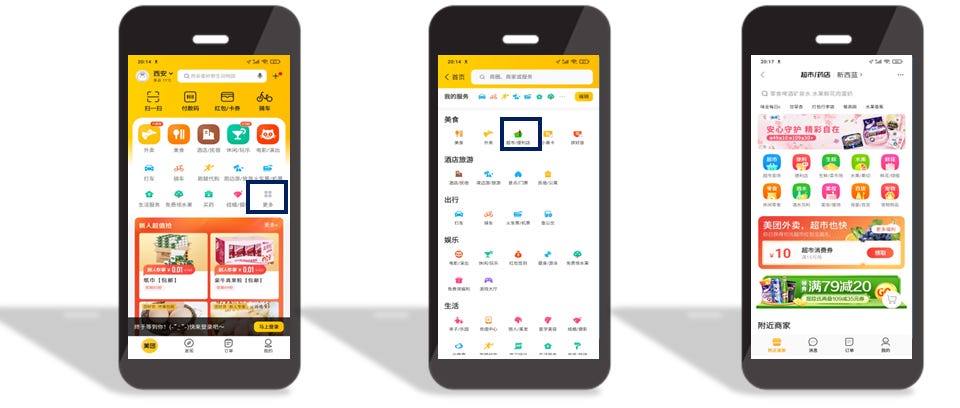

The main customer acquisition sources for Flash Shopping are the Meituan app, Meituan Waiman (meal delivery) app and offline promotions.

Entering Flash Shopping from the main Meituan app.

Selecting a story and ordering goods.

Medicine

Meituan Buy Medicine (美团买药, Meituan Mai Yao) has been independent of Flash Shopping since mid-2020, its separation partially driven by strict legislation on the category. When it split off from Flash Shopping, its 200,000 daily orders accounted for 1/5th of Flash Shopping’s total. It had 1 million daily orders in 2021, five times higher than 2019. Meituan set a target of 1.5-2 million orders by the end of 2022.

Drug marketing must be restrained, and it limits Meituan’s options to grow the category. In May 2020, it found a way: it sold RMB 1 medicine boxes in bright Meituan yellow with every order, reminding people to buy on Meituan’s platform whenever they picked it up. It sold 1.5 million such boxes in 4 months.

Emergency medicine is not an easy category for Meituan. The purchase frequency is low (the average annual reorder rate was less than 2 in 2020), the margins are often low, and, as mentioned, there’s a lot of legislation. Only chronic disease medicine, which has a high repurchase rate, and healthcare products can bring more business. Meituan plans to eventually upgrade Buy Medicine to Meituan Health, a more comprehensive health platform comparable to Ali Health and JD Health.

Merchant support

By September 2021, there were over 500,000 retail stores on Flash Shopping, with 70-80 million DAU. That’s relatively few per retailer, and some pop-and-mom shops had fewer than a dozen orders daily. The Flash Shopping platform currently services about 1 million merchants in 2,000 cities and can increase about 100,000 merchants per year. However, as on many other platforms, many merchants are not actually active but have not removed their stores from Meituan.

Convenience stores pay Meituan about 5% commission plus delivery costs. To cover the costs, they often raise the prices for online sales. Meanwhile, Meituan offered hypermarkets lower commissions (4.4%) and even subsidies to get them to join Flash Shopping. Large retailers brought traffic; small retailers brought profits.

The problem with Flash Shopping is that it is difficult to make money for a merchant. Since their main business is offline, their online abilities are often lacking. Except for some large supermarkets and verticals, the proportion of his online sales could be too small to cover the costs of necessary dedicated staff. Merchants, therefore, often need to use service providers and middlemen to help them, further increasing their costs. This may lead to poorer product quality (to reduce costs) and a bad consumer experience.

So, merchants need to be supported in increasing their order volume, conversion and improving their operating abilities. Besides offering training, Meituan thinks it has found a solution by helping merchants go ‘fully online’ through ‘lightning warehouses’ in residential areas. These warehouses have more SKUs than regular stores and better profitability for the merchant. The average order for Lightning Warehouses is higher than for other stores on Flash Shopping because they offer more SKUs. Marketing activities also help raise the AOV. Because of the similarities with front-end warehouses, we will return to this model in a future article.

Timeline Meituan's Instant Retail Business

(source: Latepost):

July 2018 - Meituan launched Flash Shopping as an independent brand and established the Flash Shopping Business Department.

September 2018 - Meituan goes public.

October 2018 - Home Delivery business group established.

August 2019 - New ‘Drug Management Law’ passed. Prescription drugs are allowed to be sold through the Internet under certain conditions.

August 2019 - Flash Shopping incubated vegetable market agent operation project “Cai Daquan”.

December 2019 - New ‘Drug Administration Law’ officially implemented. Flash Shopping for the medicine category becomes independent.

May 2020 - Meituan Pharmaceutical launched the ‘1-cent small medicine box’ campaign.

May 2020 - Flash Shopping piloted the front-end warehouse model, which later evolved into the ‘Meituan Lightning Warehouse’.

June 2020 - ‘Xiaomei Orchard’, the predecessor of Tuanhaohuo, was transferred from the Meituan platform to the Home Delivery business group.

October 2020 - Tuanhaohuo team was formally established.

December 2020 - Flash Shopping business department was split into three independent business departments: Flash Shopping, Medicine and Tuanhaohuo.

May 2021 - Flash Shopping ‘Crooked Horse Alcohol Delivery" was launched in Huizhou, Guangdong.

September 2021 - During the Qixi Festival (Chinese Valentine's Day), the daily volume of Flash Shopping exceeded 6.5 million.

November 2021 - Tuanhaohuo changes its name to ‘Meituan Haohuo’ and later to ‘Meituan E-Commerce’.

December 2021- Daily orders of Meituan Medicine exceed 1 million.

March 2022 - In the first quarter, the average daily order volume of Meituan Flash Shopping exceeds 3.9 million (including Medicine).

June 2022 - Meituan Flash Shopping pilots its own business development team in Changsha and Hefei.

Statistics

In 2019 Flash Shopping saw a GTV of RMB 20 billion.

In 2021 the number of active buyers on Meituan Flash Shopping was 230 million.

In 2021, 30% of all Flash Shopping orders were placed between 17:00 and 20:00 hours. Orders between 22:00 and 8:00 account for 16%.

In 2021, Flash Shopping reached RMB 84.2 billion, 12% of the GTV of Meituan's meal delivery.

At the time, the responsible Meituan director said that the instant retail market size would grow to RMB 1 trillion, and Meituan was aiming to have a 40% market share.

In March 2022, Flash Shopping reached 3 million daily orders.

In Q1 2022, the average daily order volume of Flash Shopping was 3.9 million (including medicine), one-tenth of Meituan's food delivery business.

In Q2 2022, the average daily order volume of Flash Shopping reached 4.3 million.

In March 2022, Wang Xing repeated the goal of RMB 400 billion in sales for Flash Shopping in 2026 (it was estimated to be at 1/4th of that goal at the time).

According to TechPlanet, the average order value of Flash Shopping in new first-tier cities was around RMB 50 in Q3 2021, while 36KR reported it having increased to RMB 70 by August 2022.

In Q3 2022, the number of Meituan instant retail orders increased by 15.2% year-on-year.

In Q4 2022, Meituan serviced 300,000 convenience stores and small supermarkets with instant retail, twice the number in 2019 and four times the GMV in that year. Besides supermarkets, it had significantly expanded in categories like electronics (e.g. Lenovo brand stores), alcohol and beverages.

In 2022, the number of retailers in Shenzhen using instant retail with Meituan increased 53% YoY, while orders grew 42%. Among these retailers, mom-and-pop stores grew the fastest, with 134%. Night-time consumption and delivery of electronic goods were two important drivers of growth.

In 2022 the annual transacting users and active merchants on Flash Shopping both increased by 30% YoY, and the single-day orders peaked at 11 million in December.

The daily order value of Flash Shopping currently sits at 400 million and should be able to reach 450 million. The average order value is RMB 90-100 RMB.

Flash Shopping is expected to be able to reach an average of 10 million orders per day.

In 2023 Flash Shopping covered more than 2,800 cities.

Note: the order volume does not seem to have increased much from 2020 to 2021, but this is caused by the separation of the medicine business. Medicine is currently estimated to have 1 million orders per day.

All of these are impressive figures. However, a Meituan employee told Latepost last year that the base of Flash Shopping is small, so high growth percentages don’t mean all that much. Basically, being a start-up, it is normal to grow this fast. The question is whether it can keep up this growth 2023 after the pandemic. Meituan thinks it will.

Challenges

Meituan charges merchants 3.5-5% in technical service and delivery fees. The platform’s spending mainly consists of subsidies for users and merchants.

Flash Shopping is still loss-making, but its loss rate is smaller than JD Daojia's, estimated to be 4-5%. Profitability could be improved by raising the fees for merchants, but this would lead to dissatisfaction among merchants and possible price increases of their goods and, thereby, a bad consumer experience. Another option is reducing costs, e.g. by paying less to delivery teams. This will also have adverse effects.

The whole industry of instant retail basically agrees that when the proportion of supermarket and standard products is high, it is difficult to reach positive unit economics. The only other option when it's impossible to improve unit economics is to commercialise the platform and offer advertising or financial services. This is what Meituan Waimai has done. The question is if Flash Shopping should also do this.

Flash Shopping's current scale, model and technology offer competitive advantages as a separate business. The biggest question for Flash Shopping, however, is what will happen to the foundation of Meituan. The profitable foundation of the company is its meal delivery and travel business. Both have come under pressure from the initiatives of Douyin (as discussed in our recent article on Douyin's local services business) and Kuaishou. Considering Douyin's enormous user traffic, its initiatives could have a serious impact on meal delivery as they already have on in-store business. This could shake Meituan's foundation and threaten the Flash Shopping business.

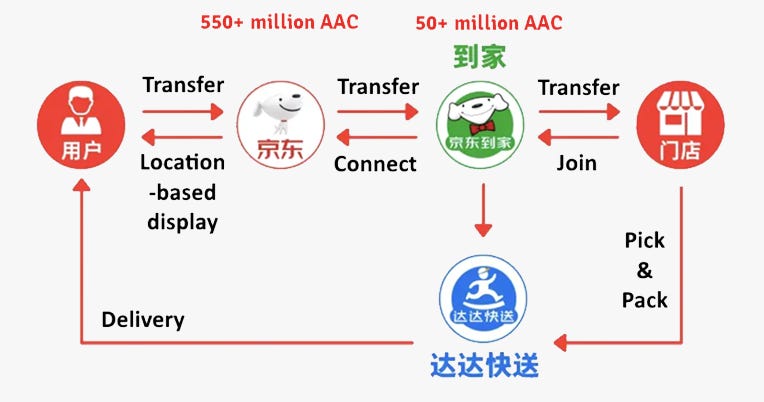

Dada Nexus: JD Daojia & Dada Kuaisong

JD.com was one of the first companies to question why a product needed to be shipped from a central warehouse while it was also available in a store just a few kilometres away. This thinking drove its development into one of the leading players in instant retail.

In 2014, JD.com launched a life services platform called Pai Daojia (拍到家), offering 2-hour delivery within 3 kilometres. The platform was renamed JD Daojia in 2015 and became an independent wholly-owned subsidiary. It’s director was Hou Yi. In the early days of JD Daojia there had been many problems with slow order picking, out-of-stocks and missing orders. Hou Yi was therefore convinced that he needed to control the product inventory and quality himself. He pitched the idea with JD’s management, who rejected it, resulting in him leaving JD to implement his idea as Hema (Freshippo) at Alibaba.

JD Daojia currently offers 1-hour delivery within a 5-kilometre radius for a wide range of products, including fresh produce, packaged groceries and pharmaceuticals sold by its participating stores.

In the JD Daojia app, users can search for a store and browse its assortment or search for a specific product.

For some time, JD.com has been using a model in which products that are not available at JD’s own warehouses and webshop but are in demand among consumers are routed to offline stores. JD has also been using a model they call ‘Jingchao’ (京超) in which offline partners deliver some product categories. Nearby supermarkets and hypermarkets would, for instance, deliver ‘fresh and urgent’ goods. This led to improved supply chain efficiency, lower costs and better consumer experience.

The Jingchao model mainly handles commodity categories, including flour, cooking oil, rice noodles and fresh products. Since delivery of these goods is difficult to achieve through Jingdong's traditional B2C logistics, the project adopts the principle of proximity and uses the offline store in the city where the customer is located as the front-end warehouse. Another type of front-end warehouse under the Jingtao project is similar to Meituan’s lightning warehouse. The difference between JD’s front-end warehouse and Meituan’s lightning warehouse is that Jingdong’s front warehouse only needs to deliver goods without operating them.

As with the aforementioned example of Alibaba, JD.com has developed different solutions for different consumer needs. Its solution for instant retail, JD Daojia, is offered as one of the divisions of Dada Nexus (or Dada Group, 达达集团).

Dada was founded in 2014 as a local instant retail and delivery platform Dada Now (达达快送, Dada Kuaisong). Dada Now provides merchants and consumers with (intra-city) omnichannel fulfilment solutions integrating warehousing, picking and distribution. In 2021, Dada Now covered 2,300 counties, districts and cities in China, servicing 1.4 million merchants and 70 million users.

Dada Nexus was created in 2016 after a merger between Dada Now and JD Daojia. While JD Daojia provides an online platform for retailers, Dada Now takes care of the actual delivery via a crowdsourced pool of couriers. Dada Now does not work exclusively for JD Daojia.

According to Dada Nexus, both JD Daojia and Dada Now are market leaders with 25% market share in the Supermarket Local On-demand Retail Platform and Open On-demand Delivery Platform segments, respectively.

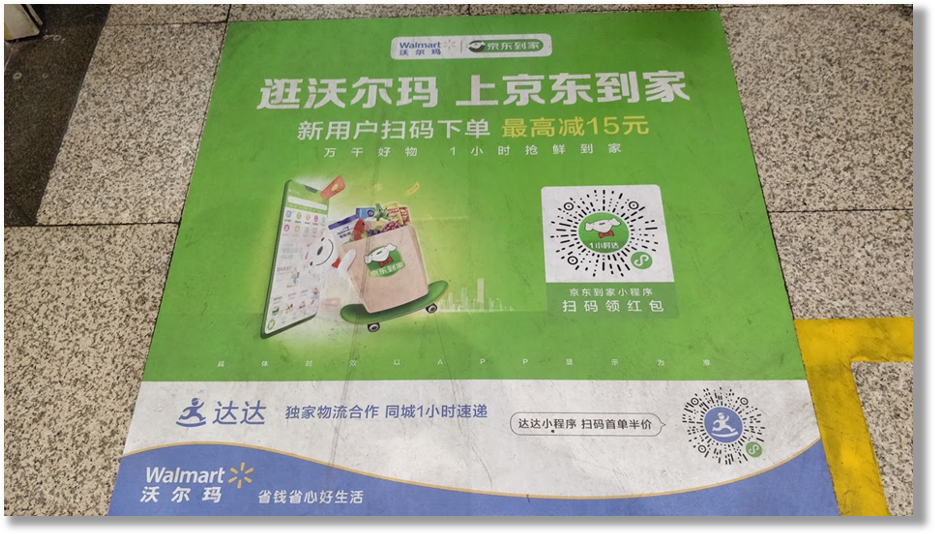

To remain competitive with online platforms, many offline chains use JD Daojia's delivery services. These include Yonghui, Vanguard, Watsons, Mannings, Familymart, Lawson, MiniSo, Carrefour and Walmart. Walmart is also a major investor in JD Daojia. JD Daijia cooperates with 90 of the top 100 retailers and supermarkets. It also works with many leading convenience store chains. The cooperation with supermarkets was not smooth at first but improved when partnerships were created through investments. JD.com invested RMB 4.6 billion in Yonghui and Walmart invested in JD, creating such strong bonds. Currently, JD Daojia accounts for more than 20% of all orders in the stores of these two chains.

When a JD Doajia manager went to see operations at Yonghui, he found that it took the staff there half an hour to collect goods in the store and take it to the courier and walked 20,000 to 30,000 steps a day. He realized stores had to redesign their layout for instant retail. He persuaded Yonghui and Walmart to set up special shelves for JD Daojia and put the highest selling items there. It greatly improved efficiency of order picking. Nowadays, supermarkets dedicate up to 1,000 square meters of their stores to a front-end warehouse function for e-commerce.

An e-commerce distribution center at Walmart in Beijing.

A pilot store with a 300 square meter warehouse and e-commerce team was set up by Walmart and JD Daojia in Shenzhen in 2017. It achieved an average of 1,000 orders per day in one year. In 2022 this had increased to 2,000 orders per day; 30% of the store’s sales. In 2022 Walmart’s total online sales was RMB 44.3 billion, of which JD Daojia contributed several billions.

Dada Nexus went public in June 2020, raising $320 million and being valued at $3.5 billion. In 2022, JD.com invested another $546 million in Dada, giving it 51% ownership of Dada Group. Walmart holds 9%. Dada Nexus is still loss-making, although the loss has decreased in recent years.

Walmart stores often promote JD Daojia's services prominently. Floor sticker at Walmart advertising the JD Daojia delivery service. “Visit Walmart, go to JD Daojia online. New user, scan the QR code, place your order and get up to 15 yuan discount. Thousands of good products, delivered to your home within an hour.”

In 2022 there were 400 Walmart stores in China, half of which had made some of their products available on JD Daojia, essentially making them serve as JD's front-end warehouses. Dada also delivers orders from Walmart's own mini program. The reason why JD.com was able to build Walmart as its own front warehouse is that JD.com has a relatively close connection and a high degree of system integration with major supermarkets. Meituan started from small and medium-sized merchants and has less contact with large supermarkets.

For fresh products, JD Daojia has a specific channel called JD Grocery Shopping (京东买菜, Jing Dong Mai Cai). In January 2023, JD registered the Jingdong Maicai trademark and launched JD Maicai on the app’s homepage shortly after. Goods ordered through JD Maicai are supplied by third parties, including chain supermarkets and front-end warehouse operator Dingdong Maicai. Nevertheless, JD has also started testing the front-end warehouse model under the JD Maicai brand in Beijing.

Dada Now uses a crowdsourcing delivery model, which has lower costs and a larger capacity base. For merchants, the delivery fee depends on the delivery distance and their individual policies. For instance, with JD Maicai, it ranges from free to 10 RMB.

Over the years, Dada and JD Daojia have been adding additional tools and services for merchants to improve their business efficiency and boost online sales.

Most of the problems with instant retail orders are caused by errors during order picking (missing items, wrong items, out-of-stock, etc.). JD Daojia offers digital solutions to help merchants pick orders, reducing the order-picking time by 15% and order pick-up time by 23%.

Dada Youjian, a crowdsourced sorting management solution, helps merchants with picking services for omnichannel orders, product packaging, order delivery and other services. Because of this the supermarket does not need to recruit its own order pickers. It is currently used by Walmart, China Resources Vanguard, Yonghui Superstores, 7Fresh and other stores.

It has the following five functions: picking personnel recruitment, entry and management, picking process management, data aggregation and analysis, and service quality monitoring.

Dada added geo-fencing functions that allowed merchants to determine the delivery area.

Logistics SaaS Dada Smart Delivery assists merchants and third-party delivery service providers with "managing orders, dispatching and routing for omnichannel on-demand orders".

In October 2019, Dada released ‘Haibo’ (Haibo Zhongtai SaaS system) an omnichannel solution for "supermarket omnichannel fulfilment". It currently covers 11,000 chain retailer stores. Haibo was recently upgraded with a ‘product builder’ that shortens the time to launch a new product on the platform by 80%.

Dada Haibo also provides omnichannel digital solutions integration fulfilment, marketing and memberships helping merchants to quickly digitally upgrade. It can be connected to all instant retail platforms in the market as well as Dada Youjian.

JD Daojia's revenue mainly comes from commissions from retailers, marketing services for brand owners and delivery services. It can also cooperate with brands to help launch more products and do same-city brand promotions. In 2022, more than 280 brands cooperated with JD Daojia for online marketing, increasing by more than 30% year-on-year.

According to iResearch, JD Daojia's market shares in instant retail for supermarkets in 2019, 2020 and 2021 were 21%, 25% and 27%, respectively, making it the market leader in this segment (with Meituan being the overall market leader in instant retail).

In Q4 2022, supermarkets accounted for 53% of the total GMV of JD Daojia. Consumer electronics and home appliances accounted for 43% of the total GMV, and other categories accounted for 6%. The average order value had increased to RMB 235 (RMB 165 for supermarkets). The AOV is expected to rise further thanks to changes in the product mix.

The difference between JD Daojia and Meituan’s Flash Shopping partner supermarkets is that JD Daojia’s main supermarket category consists of national key account supermarkets, while Meituan's are lightning warehouses. Instant retail accounts for 20% of the total online daily sales of JD Daojia's top key accounts, of which 50%+ comes from JD Daojia and 25% from the supermarket’s own platforms. For example, Walmart’s online sales business mainly comes from JD Daojia and Walmart Mini Programs. The remaining business comes from other channels.

Customer acquisition costs of JD Daojia are currently relatively small. A new customer costs RMB 10-20. Subsidies are shared between JD and the merchants. Delivery costs through Dada Now are RMB 7-8, in line with the industry average.

JD Shop Now

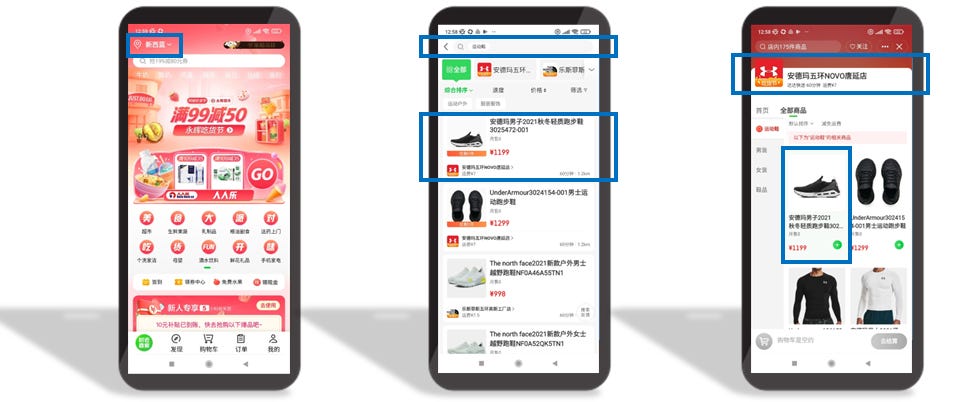

In Q4 2021, JD.com and Dada Nexus jointly launched ‘Shop Now’ (京东小时购, Jing Dong Xiaoshi Gou, literally ‘Jingdong Hourly Shopping’). This basically meant that JD Daojia was integrated into the main JD.com app. Merchants on JD Daojia were also connected to a newly launched ‘Nearby’ menu entrance in the main app. A Jingdong Shop Now WeChat mini-program was launched simultaneously, and Shop Now also received traffic from JD Search, JD Supermarket and other parts of JD's ecosystem.

Searching for a product through Shop Now.

When placing an order on ‘Shop Now’ the system will match a consumer with a shop within 3-5 kilometres, based on the customer’s location. As on the JD Daojia app, orders are delivered by Dada Now. JD’s own self-operated retail, like 7Fresh and JD Computer and JD Mother & Bay stores, are also integrated into Shop Now.

This integration meant that JD Daojia's reach was increased from 50+ million users on its standalone app to 550+ million on the ‘mother app', or at least those users in cities where JD Daojia operated.

Search and recommendation entrances on the JD homepage account for 60-70% of JD Daojia's revenue, but the Nearby function is growing fast (tripling YoY in Q4 2022).

By Q4 2022, the Shop Now GMV had increased by 80%. The number of active stores had increased by 50% to 220,000. In Q1 2023, JD Daojia added more than 60,000 physical stores and by its 8th-anniversary promotion in which 300,000 stores from 1,800 counties, districts and cities participated.

In Q1 2023, JD.com’s hourly shopping GMV further increased by 60% YoY. GMV from ‘Same City’ (同城) is maintaining growth because the DAU of this option in the app continues to grow. Page revisions and optimization of shopping efficiency have further improved the conversion rate. The search functionality also displays a ‘price star’; the low-price option available through Shop Now.

An important goal of JD Daojia is to help JD.com acquire more customers from offline businesses. At the same time, it should help further penetrate JD.com's main app users. In the long term, the goal is to make 50% of JD.com's app users of Shop Now/JD Daojia.

All in all, JD’s Shop Now has become a major driver of JD Retail’s growth. According to insiders, JD plans to separate JD Daojia from Dada and merge it into the main JD app, eventually closing the separate JD Daojia app. Shop Now seems to be the first step.

Statistics

As of August 2019, JD Daojia provided delivery services in more than 100 cities for 500 retail chains with a total of 100,000 store locations.

JD Daojia had 41.3 million active users as of September 2020.

Dada Now recorded a 40% year-on-year increase in delivery workers, with 1 million active riders in 2022.

In 2022, the GMV of the JD Daojia platform reached RMB 63.3 billion, a year-on-year increase of 47%. The number of active stores exceeded 220,000, a year-on-year increase of more than 50%. In 2022, the number of active users on the JD Daojia platform was 78.6 million (up from 62.3 million in 2021).

Dada Group's total revenue (JD Daojia + Dada Now) in 2022 was 9.37 billion yuan, a year-on-year increase of 36.4%. In 2022, the revenue of JD Daojia platform was 6.21 billion yuan, a year-on-year increase of 53.5%. Dada Now's revenue was RMB 3.16 billion.

In 2022, JD Daojia’s business growth rate was 70%+, and the target market size was 70-80 billion yuan.

In the 12 months ending March 2023, JD Daojia’s GMV reached RMB 67.3 billion, a YoY growth of 37%.

In May 2023, Dada Group released its Q1 2023 results. Revenue had reached RMB 2.6 billion, a YoY growth of 27%. Its net loss narrowed by 16 per cent YoY. JD Daojia’s revenue within the group was RMB 1.8 billion, and Dada Express’ 800 million. The total GMV on JD Daojia reached 67.3 billion, a YoY growth of 37%.

Leading brand stores like Sephora, L’Oreal, Xiaomi, Decathlon and Oppo all saw three-digits YoY growth rates on JD Daojia.

60% of JD Daojia’s traffic comes from JD’s main app.

Among the daily transaction volume of JD Daojia and JD Shop Now, JD Daojia’s order volume is 500,000-600,000 orders, and Dada Group’s Q1 2022 report showed that the weekday order volume was 700,000-800,000 orders. For the total order volume of JD.com’s Shop Now, the unit price of JD Daojia’s customers is relatively high, and the AOV excluding 3C categories is 120-150 yuan.

Challenges

In 2022 JD Daojia was still making a loss of 1-5% per order. Dada Nexus expects to break even by mid-2023.

The instant retail business will affect JD Logistics since orders for certain products will be routed to instant retail. The JD app will intentionally prevent business conflicts and exclude products that will cause losses. If a product is delivered the next day, for instance, through JD Supermarket, it will trigger storage and logistical costs for JD. In the future, JD plans to remove such products (e.g. bulky and lightweight products) that create high storage and logistical costs and, thereby, losses from its self-operated business and offer them from third-party stores. If goods are, for instance, delivered from a local supermarket, JD does not pay for the storage costs.

A disadvantage for JD Daojia is that its couriers (‘Dada knights’) are crowdsourced, and unlike those of Meituan and Ele.me, they have less loyalty to the company while JD Daojia also cannot force ‘gigs’ on them. On the other hand, Dada Nexus does not have to bear personnel costs for the courier. If the supply of couriers is high, Dada's model has an advantage, but if the supply is low, the self-operated model will have greater advantages.

JD.com puts the instant retail business in a higher strategic position. As mentioned, you can select nearby channels on the homepage of the JD.com app. JD.com’s page pushes more instant retail promotions, and JD.com has adjusted its internal organisational structure and established an intra-city business department.

There are three focus points to improve the profitability of instant retail at JD Daojia:

Increase the retention of existing users.

Optimise the product categories and increase the average order value.

Improve efficiency and reduce redundancy costs.

In June 2022, news broke that JD Daojia was launching a pilot for a meal delivery service to help Dada Now increase its order density. If it only relies on JD Daojia, Dada Now might not be able to survive. If it combines instant retail and meal delivery, like Meituan and Ele.me do, it will have better coverage for its couriers and better chances of survival.

JD Daojia mainly cooperated with key accounts. In the future, it plans to attract small-scale merchants and move into lower-tier cities. Currently, orders in first- and second-tier cities account for 70% of the total volume of JD Daojia, and the sinking market accounts for 30%. The growth rate in the sinking market is relatively high, though.

The others

Alibaba - Ele.me

Compared to JD Daojiao and Meituan Flash Shopping, Alibaba's Ele.me remains a smaller third player in the instant retail market. There also seems to be less isolated information available on its instant retail business.

Meituan Flash Shopping was separated from the meal delivery business when it was identified as a second growth opportunity for Meituan. Ele.me is somewhat similar as it also started out as a meal delivery business, but the link to mobile payments and Ant Group play a more important role for Ele.me.

In 2022, Ele.me's daily instant retail orders were 1.2-1.4 million, while market leader Meituan saw 4-4.5 million. Ele.me continues to focus on meal delivery and has a low conversion rate in instant retail. Its instant retail orders are only 7-8% of its meal delivery orders. At Meituan, this is more than 10%.

Instant retail on Ele.me.

Alibaba - Taoxianda

Besides Ele.me, Alibaba offers instant retail via various other platforms.

Taoxianda delivers goods within an hour. In addition to the Sun Art stores like RT-Mart, several other supermarket chains are connected to the Taoxianda marketplace. Currently, Hummingbird (Fengniao), Ele.me's delivery service, provides delivery service for Taoxianda.

Another form of cooperation with Alibaba is the Tmall Supermarket inventory sharing program. This is comparable to JD's Jingchao: consumers place their orders via the Tmall Supermarket platform, but delivery is done from the Sun Art branches. This happens within an hour for customers within a radius of 5 kilometres and half a day for customers within a radius of 5 to 20 kilometres.

Through Taoxianda, Taobao offers ‘Taobao Hourly Express’ for fresh fruits and vegetables, rice noodles, flour and cooking oils, daily necessities and other commodities. It allows merchants to display an ‘hourly delivery’ label next to their products.

In May, Alibaba announced that Taoxianda and Taocaicai would merge and be renamed Taobao Maicai. The combined offering includes 24-hour and 30-minute delivery. In March 2021, Alibaba had already merged Hema Jishi (a community group-buying concept that was taken out of the Hema group) and Ling Shou Tong (零售通) into the ‘MMC department’. The external brand names Taobao Maicai and Hema Market were merged into Taocaicai in September of that same year.

Tao Cai Cai can be found as a menu item in the Taobao and Taote (C2M) apps. Tao Caicai also has its own mini-program, which features the same gamification that we have come to know from Pinduoduo.

In May 2023, Alibaba also organised Tmall Supermarket, Taocaicai, Taoxianda, Shiping Shengxian 食品生鲜 and other businesses into the local retail sector of the domestic digital commerce spin-off (Taotian). MMC was disbanded by this reorganisation.

Taoxianda was born out of the delivery system of Hema (Freshippo). The question arose if the same system could be applied to hypermarkets like RT-Mart. Initially, RT-Mart established its own delivery service (Feiniu) and found the online share of orders reached 10-20%. This increased to 70-80% during the pandemic. After opening up, this ratio dropped to 50%, still much higher than before the pandemic now that consumer habits had changed. The AOV increased, though, and RT-Mart's online sales now account for 60% of its revenue.

Tmall Supermarket (like JD Supermarket) uses large warehouses and ships tens of thousands of SKUs to the whole country. Taoxianda only offers 80% of the highest-selling products and delivers these intra-city from supermarkets like RT-Mart.

RT-Mart is also integrated in the Tmall Supermarket platform. Before the pandemic, it only accounted for 0.5% of that platform's sales. Now it is 10-20%.

Tmall Supermarket accounts for about 1% of Tmall's roughly RMB 4 trillion GMV, or RMB 40 billion. The instant retail part of that is about 1/6th to 1/5th of that, so less than RMB 10 billion.

The total annual sales of Alibaba's Ele.me instant retail and Taoxianda business (see below) together are RMB 35 billion.

In the future, Alibaba will offer a new model called ‘shared retail', a low-cost retail model. In this model, Alibaba's entities will not procure any goods. Instead, it only uses its own technology to sell goods of other parties with their own supply chain.

Searching for a specific shop on Taoxianda.

Selecting a product on Taoxianda.

Douyin

Earlier this year, we wrote extensively about Douyin’s moves into local services through in-store group-buying and food delivery. In 2022, Douyin also launched an instant retail service called Douyin Xiaoshi Da (抖音小时达, ‘Douyin Hour Express’) in some pilot cities like Shenzhen, Wuhan and Tianjin. The service focuses on merchants of fruit, vegetables and other fresh products. Hotpot and pre-made dishes are also available.

Participating merchants include Wumart, Dingdong Maicai and Yonghui Supermarkets, but also Apple franchised stores. The merchant is responsible for delivery. Earlier, Douyin had already launched Douyin Supermarket, which offers next-day delivery.

As with the local services discussed in an earlier article, merchants can promote their businesses through livestreams and videos, generating extra advertising income for Douyin.

Tencent

Earlier this year, Tencent started testing a WeChat mini program called ‘Shop Express Delivery’ (门店快送, Mendian kuai song) in Shenzhen and Guangdong. Products range from food & beverages, fresh groceries and daily necessities. The merchants on the mini-program are mostly chain brands and large internet companies with offline stores or front-end warehouses.

No commission is charged during the pilot period, and delivery is either done by Meituan Maicai, Dingdong Maicai, Pupu Supermarket, KFC and other companies with delivery capabilities or by merchants themselves or third-party logistics service providers like SF Express.

According to Tencent, 'Shop Express’ is meant to help consumers find high-quality mini-programs for instant retail. As such, it sounds more like an aggregator than a stand-alone business.

Pinduoduo

In early 2022, Pinduoduo started recruiting local offline retailers, front-end warehouse operators, wholesalers, and couriers in China’s first-tier cities of Shanghai, Beijing, and Shenzhen. Pinduoduo focussed on fruit, flowers, cakes, etc. However, since Pinduoduo allowed merchants delivery times up to 48 hours, not only shouldn't this be considered instant retail, but we should also not expect it to become a major player.

The major differences between platforms

Let's look at some of the biggest differences between Meituan Flash Shopping, Dada Nexus and Ele.me.

Dada Now couriers deliver 50 orders daily, while Meituan's do 30. The reason for Meituan's lower number is that its orders are concentrated around noon and night. Dada's couriers deliver 13 orders more daily than its crowdsourced ones.

The target audiences of Meituan Flash Shopping and JD Daojia differ: Meituan targets high-end young consumers, while JD Daojia targets housewives. Meituan's post-90 consumers comprise 60% of their customer base, while only 20% at JD Daojia. At Meituan, post-80 consumers account for 85%, and at JD Daojia 70% (where they are mainly married working mothers).

Meituan Flash Shopping has fewer users in the sinking market than JD Daojia: 24% versus JD Daojia's 33%.

Meituan sees relatively higher order frequency and lower order value, while JD Daojia sees lower order frequency and higher order value. In 2021, Flash Shopping had an average purchase frequency per consumer of 5, with an average order value of RMB 74, while JD Daojia's were 3-4 times and RMB 192, respectively. JD Daojia also sees more public holiday purchases.

Meituan Flash Shopping offers more small and medium-sized supermarkets, convenience stores and vertical businesses like flower shops and has longer business hours. JD Daojia works more with large-scale supermarkets.

Among Meituan, JD and Ele.me, Meituan Flash Shopping has the biggest reach in cities, reaching fourth-tier cities. JD Daojia's coverage of third- and fourth-tier cities is much smaller. The reason is that couriers in such cities can't rely on instant retail from supermarkets alone to make a living. Meituan can also offer these couriers meal delivery ‘gigs'.

Meituan Flash Sales has monthly sales of about RMB 10 billion. JD Daojia's monthly GMV is estimated to be RMB 5 billion. Almost half of JD Daojia's GMV concerns 3C products with a high sales price. So, while Flash Shopping has a 2 times higher GMV, the difference in orders would be even bigger, probably 4-5 times. Ele.me is estimated to be about the same size as JD Daojia.

JD Daojia mainly relies on large supermarkets, while Meituan Flash Shopping relies on medium-sized supermarkets and convenience stores.

Conclusion

The development of instant retail has two stages: the first is generating enough traffic, and the second focuses on ensuring retention by increasing supply (number of merchants and SKUs). While the maximum user penetration has not been reached, many platforms are shifting from stage one to stage two. Meituan's Flash Shopping is expected to perform better than JD Daojia at this stage.

The lack of effective supply (the number of stores offering a richness of SKUs in the area around the consumer) is considered to be the short-term limiting factor to the growth of the instant retail platforms. According to data from Meituan, 40% of users’ product searches on Meituan are unmet, and the potential demand exceeds the category supply of the platform. The development of user consumption habits also requires an increase in supply.

Meituan believes that, regarding supply optimization:

Compared with self-operated e-commerce, instant retail platform e-commerce will become the main force for expanding supply, and its characteristics of high turnover and regional precision marketing are expected to drive brands to increase investment.

Small and medium-sized vertical stores and new formats will contribute to supply density and category diversification.

The average order value of instant retail is expected to rise with the gradual development of user habits and the increase in the operating experience of the platform and merchants (more SKUs, better recommendation of popular products/related products, coupon setting, etc.).

Players like Alibaba (Ele.me), Meituan and JD.com, which already have their own delivery infrastructure, have the best chance of winning this market. Douyin had the advantage of its 700 users that frequently open the app, but merchants are required to make extra costs in advertising and have to arrange delivery themselves (or through 3rd parties that already offer instant delivery directly). Because of its experience and well-developed infrastructure for food delivery, Meituan is considered to be a potential leader in the instant retail segment, followed by JD Daojia.

Meituan Flash Shopping and JD Daojia are expected to reach RMB 438 billion and RMB 140.1 billion by 2025, accounting for respectively 62% and 20% of the instant retail market. At the same time, JD Daojia's average revenue per order (related to the average order value) is expected to remain higher than Meituan's. Despite this, the average profit of Flash Shopping is still expected to be higher owing to the higher efficiency of Meituan's platform. It is expected to be the first to turn a profit in this sector: RMB 1.58 per order (or 1.6% of the order value), accumulating RMB 6.9 billion in operating profit. Meanwhile, these figures are expected to be RMB 4.4 and RMB 2.5 billion for JD Daojia.

The shorter the delivery time, the higher the costs. Still, market players have little choice to enter this sector, if only to block the market for their (potential) competitors.

As Meituan and Ele.me have entered instant retail from supermarkets, convenience stores and pharmacies, JD Daojia has come under pressure. Meituan Flash Shopping is encroaching on the supermarket and electronics segments that JD Daojia was traditionally strong at. Xin Lijun, CEO of JD Retail, said at the JD Retail Commendation Conference held on March 7 that the intra-city business is one of the four must-win battles for JD Retail in 2023.

Industry insiders consider instant retail a win-win business of integration and symbiosis. Retailers digitise and expand their service area. Consumers get convenience and easy price comparison (many apps show what a product is sold for at multiple participating retailers). Instant retail also offers more jobs for delivery workers (7.52 million nationwide) and offers more ‘gigs’ during downtime if they are not delivering food.

The fact that many instant retail models actually support the ‘real economy’ instead of trying to replace it will also please the Chinese government. A recent policy document by the Central Committee and State Council mentioned instant retail as a new model that should be further developed.

Meanwhile, in the West, we have seen the emergence (and largely demise) of many flash delivery brands like Gorillas, Getir, etc. These are also forms of instant retail. But unlike platforms like Meituan Flash Shopping and JD Daojia, they don’t add extra services to existing physical retail infrastructure. Instead, they try to replace existing retail by setting up their own dark stores and delivery couriers. This attempt to compete with decades of retail experience of supermarkets that have learned to deal with single-digit net margins has many people scratching their heads.

And just as we’ve seen with other new forms of e-commerce, as the market share of instant retail increases, the market share of traditional (‘far field’) e-commerce will decline.

Sources

Six Degrees, a leading global expert network/quantitative research firm that operates in China. Augmented with information from:

Fung Business Intelligence 2022-07-22, Equal Oceans 2021-11-25, Supchina 2022-08-25, Hexun News 2022-08-24, 36Kr 2022-08-22, Linkshop 2022-11-26, Linkshop 2022-11-13, 第三只眼看零售 2023-05-11, 第三只眼看零售 2023-03-29, Linkshop 2023-04-14, Tech Planet, 2023-04-26, 第三只眼看零售 2023-03-30, 零售商业财经 2023-05-26, 第三只眼看零售, 2023-02-17, Linkshop 2023-03-02, 第三只眼看零售 2023-02-21, LatePost 2022-06-08, Linkshop 2022-12-29, TechPlanet 2023-04-12, LatePost 2023-3-16, LatePost 2022-07-25, Linkshop 2023-04-01, Pandaily 2021-09-08, Equaloceans 2021-12-03, TechPlanet 2023-02-15, Technode, 2022-04-21, 第三只眼看零售, 2023-06-21, Latepost 2023-06-21.

All visuals by ChinaTalk.nl unless stated otherwise. These visuals may not be used or reproduced without the prior consent of ChinaTalk.nl.