TikTok Shop Watch #3 – A reality check on live commerce

An examination of TikTok Shop's different sales models and success (or lack) thereof

Content

Introduction

This week, we are wrapping up our deep dive into TikTok Shop. In the previous two weeks, we have taken you to Southeast Asia and the US to see how TikTok’s e-commerce ventures are doing there. We have also shared some information on the progress, or lack thereof, in the Middle East and Europe.

It has become clear that TikTok Shop has structurally overestimated its short-term potential, especially in the UK and US. Last year, it set a GMV target of $50 billion, with $17.5 allocated to the US market. The actual GMV was only about $33 billion, of which the US accounted for $9 billion.

There are various reasons why TikTok Shop did not meet its targets. Some were related to the temporary loss of GMV when it had to restart its business in Indonesia, others to stakeholders' reluctance to invest in a TikTok Shop business in the US with a potential ban on the app looming over it.

But the biggest reason for TikTok’s continuous hubris seems to relate to the gap between their expectations for live commerce and the actual willingness of brands, influencers, and consumers to adopt this new sales method. In this last of three reports, we will explore TikTok Shop’s sales models and the reasons for the disappointing results of live commerce.

At Tech Buzz China, we think there is a place for live commerce as a new sales channel in the market, and TikTok Shop is the most likely leader in this space. However, we do not subscribe to the claims of some social commerce service providers that live commerce will be enormous just because it is in China. As we will point out in this report, the circumstances are different between China and the West, and the context that made live commerce so enormously successful in China is often absent.

The sections on the first two dimensions of TikTok’s sales model (fully versus semi-managed and cross-border versus local) are available to all readers. The sections on the third dimension (shelf versus content e-commerce) and exploration of the limitations of live commerce are available for our paid subscribers only.

Cheers,

Ed Sander – Research Editor

Sales models

TikTok US e-commerce business has gone through four phases: [1]

1. Semi-closed loop stores (2020): traffic for third-party stores is generated by short videos and livestreams on TikTok, but transactions are completed on external websites like Shopify. TikTok still operates a SaaS system comparable to Shopify, enabling merchants to link to external websites for sales. This has advantages since no platform management fees have to be paid, only relatively low transaction fees. External websites can also operate independently and are not bound by platform rules.

2. Closed-loop local store (mid-2023): cross-border business through a fully managed model (see below) for local companies in the US and local shipments.

3. The ‘ACCU store model’ (September 2023): A model open to US-China joint ventures: US entities with more than 25% Chinese ownership, US inventory, and at least $2 million annual GMV in one category on Amazon can apply.

4. The ambitious global GMV goal is $50 billion for 2024 (a target it missed, as discussed in Part 2 of this series).

In the US market, the theoretical key factors for short video platforms such as TikTok Shop to successfully operate e-commerce mainly include the following aspects:

Localized operation. TikTok Shop's management has rich experience in China and can operate well with the characteristics of the US market.

The platform is highly user-sticky, and users are willing to spend significant amounts of time on it, which is beneficial for sales.

TikTokShop adopts the interest e-commerce model to attract users through live broadcasts and short videos, which has been very effective in China.

TikTok Shop's user profile differs from traditional e-commerce platforms such as Amazon, which helps reduce direct competition with these platforms. The company’s leading US user group comprises young women with higher incomes. By understanding and utilising users' characteristics, TikTok Shop can provide a more personalised and attractive shopping experience.

In the second part of this series, we concluded that TikTok is underperforming, so this theoretical framework might not entirely hold up. This report will examine how well TikTok Shop’s sales models are performing inside and outside the US.

There are various dimensions on which to explore TikTok Shop’s sales models.

Merchant mode: fully managed versus self-operated

Merchant location: cross-border versus local-to-local

Shelf e-commerce versus content/interest-based e-commerce

We will examine all these dimensions.

Fully managed versus self-operated

There are two models for merchants on TikTok Shop: the (fully managed) mall mode and the self-operated store mode (divided into cross-border merchants and local merchants, each with its own internal team). Both models are not available in all markets. In some markets, like Indonesia, TikTok does not allow cross-border business because of local governance and trade protection policies. [2]

Source: [2]

The popularity of these modes in different regions is closely related to local market characteristics. In terms of the operating model, the Southeast Asian market mainly adopts the self-operated merchant model and does not provide managed services. Due to Southeast Asia's low average customer price and cross-border logistics restrictions, the region prefers to use the self-operated merchant model.

On the contrary, in markets with higher average order values such as Europe and the United States, the managed model is more applicable. The UK and US markets adopt the fully managed model.

In Saudi Arabia the fully managed model accounts for 100% of sales. This is because in Saudi Arabia TikTok cannot conduct local-to-local business, the fulfillment cost is high, there is no content ecology, and there are many prohibited and restricted situations.

At the start of 2024, in the UK, the fully managed model accounted for about 30%, and in the United States it was 20% - 30% (while some sources claim it is as low as 15%). The cross-border self-operated model in the United States accounted for more than 30%, and the rest was the local-to-local model.

Let’s explore these modes in more detail.

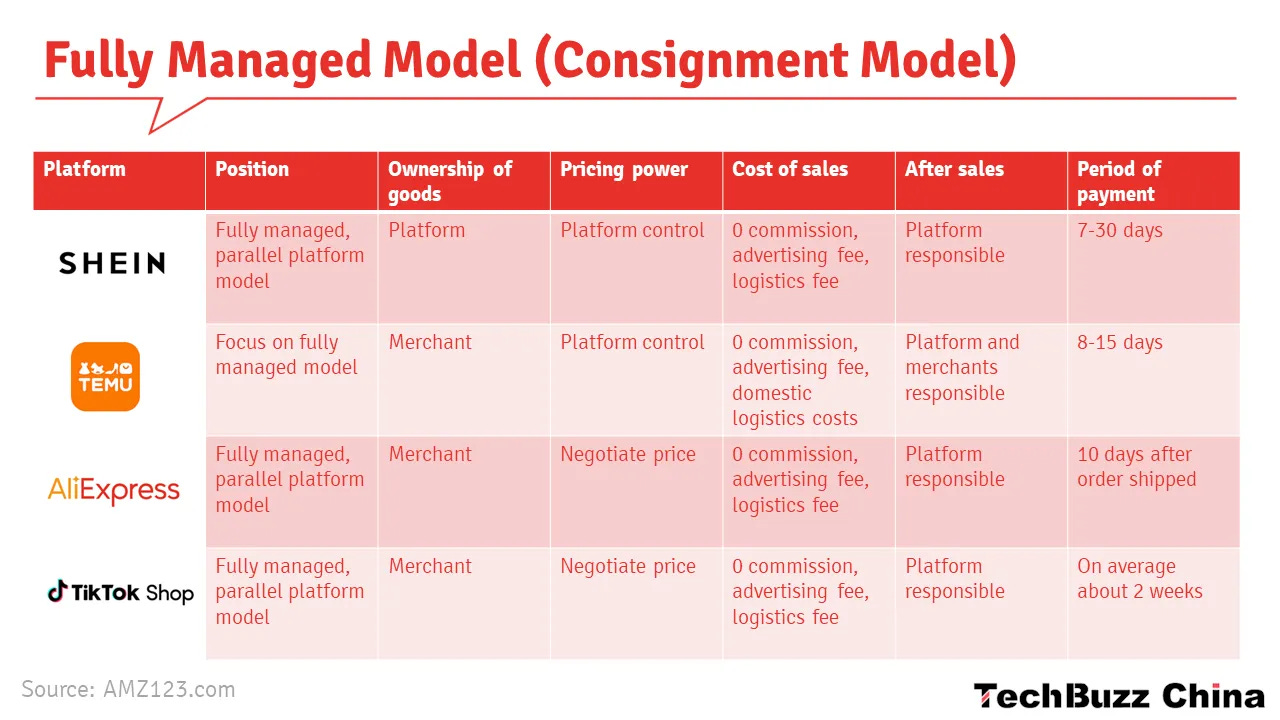

Fully Managed Mode (Mall)

In the mall mode, merchants have no pricing power and can only provide goods at the negotiated supply price. The platform purchases goods from suppliers and distributes them through its own logistical systems while also being responsible for marketing, pricing and after-sales. Under the fully managed model, shipments are made from Guangzhou, and no overseas warehouses are used. As such, it resembles Temu’s fully managed model. This model is more suitable for factory-type merchants with little cross-border e-commerce experience.

This model has several advantages, including simplified procurement processes, reduced costs of intermediate links, controlled pricing strategies, and improved quality of after-sales service. Overall, it optimises supply chain management and improves operational efficiency. Meanwhile, the manufacturer does not have to deal with the complexities of cross-border e-commerce and can focus on production efficiency.

Our December 2023 report explained how TikTok Shop applied the fully managed model and how it differs from its competitors' fully managed models.

When comparing the operational characteristics of Temu and TikTok’s fully managed model, we can see that TikTok combines shelf and content e-commerce, promoting products through short videos, and usually has a higher AOV but a lower number of items per order than Temu.

TikTok only provides fully managed services in three countries globally (US, UK and Saudi Arabia), but it faces problems such as thin profits and policy restrictions. In addition, since TikTok requires suppliers to bear additional costs, its turnover speed has slowed, making it difficult to compete with pure-player e-commerce platforms.

The fully managed model has not performed well on TikTok. It has only achieved some results in small categories such as beauty and yoga clothes, and most small and medium-sized sellers have failed to obtain the expected benefits. The fully managed business, in which merchants only have a 20% margin, is relatively small in the US compared to other developed markets. Compared with other mature platforms, TikTok's scale in fully managed business has also not yet reached the same level, and there is a gap in overall operating results.

The profit potential of the fully managed model is considered to be higher than that of the self-operated model, as the platform ensures profitability through its own margin. However, in early 2024, the fully managed model was still loss-making. In 2024, TikTok Shop planned to focus on developing the local-to-local and cross-border POP business and reduce the proportion of fully managed cross-border business.

In the summer of 2024, the fully managed business only accounted for 1/5th of GMV. To compete with Shein and Temu, TikTok’s subsidy rate was as high as 40%. As soon as the subsidies ended, TikTok lost users. [4]

A reason given for the poor performance of the fully managed model is that it is not accurate enough in platform marketing, resulting in its poor performance compared to the POP model. Chinese merchants' performance in the POP model is particularly good because the threshold of the POP model is high, and merchants need to have specific content marketing experience. Such experience is crucial to improving sales performance.

Self-operated Store Mode (POP)

In the self-operated store mode (POP), merchants can set prices independently. This mode is more suitable for companies with sufficient operating capabilities for cross-border e-commerce.

In the United States, TikTok launched the cross-border POP model in October 2023, which led to an increase in business volume. It also invited large sellers such as Walmart and Amazon to participate. These large sellers have high market recognition of their products, have warehouses, a rich assortment, and strong fulfillment capabilities.

The (combined local-to-local and cross-border) share of GMV of the self-operated store mode (POP) reached 70% in early 2024, significantly higher than that of the fully managed model.

Moving towards Semi-Managed

In Southeast Asia, TikTok Shop's strategy for logistics management of merchants has been undergoing significant changes in 2024. The platform is moving towards a more assertive approach for semi-managed services, which will allow merchants to take charge of their own warehousing and shipping operations. This marks a shift from their former stance, where TikTok Shop is not prioritizing business models that require merchants to handle their own logistics.

However, this transition may present challenges for merchants. A review of merchant preparedness reveals that less than half of them possess the necessary skills for autonomous logistics management. This is particularly evident in the case of Tokopedia merchants, many of whom lack the advanced business skills required to effectively manage their own logistics operations.

Although TikTok's semi-managed model may be more flexible than Temu's fully managed model in some aspects, it still mainly relies on profit through price margins. Therefore, even if TikTok implements this model in Southeast Asia, the effect may not be particularly ideal.

Among the semi-managed models of major platforms, Shein and Temu have performed particularly well. Meanwhile, sources disagree on the success of TikTok Shop’s semi-managed model. Some say it has very low sales and can be ignored. But according to a former JD Operations Director, data showed that TikTok's semi-managed business growth rate and scale in the first quarter of 2024 were significantly higher than Temu’s, with orders about 10 times that of Temu and 30 times that of Shein.

Cross-border versus local

Besides the managed or self-operated (POP) modes, there are two more dimensions in which TikTok Shop’s operating model can be categorised:

Cross-border business, handled by TikTok's cross-border business team, includes the fully managed model and cross-border big-selling POP stores entering the US market.

Local-to-local business, often operated through Fulfilment by Amazon warehouses. The SKUs in the local-to-local model are inexpensive and have many categories. TikTok mainly makes profits by charging commissions and commercial investment fees, while the cross-border POP model primarily charges information service fees. The Southeast Asian market mostly adopts this (self-operated) merchant mode and does not receive managed services.

TikTok evaluated Shein’s cross-border model but found the supply chain too long, making it difficult to increase volume quickly. Therefore, the platform decided to supplement with local-to-local and cross-border business. [3] However, the expansion potential of cross-border businesses is limited, and they rely more on large sellers with local qualifications.

The rest of this report, including information on TikTok Shop’s forms of content e-commerce and the progress (or lack thereof) of live commerce is available to paid subscribers only.