Tencent's AI Bet Is Not a Chatbot. It Is WeChat as an Action Layer

Tencent is not trying to win the chatbot beauty contest. It is wiring AI into the places where users already message, pay, order, and work.

Things you might have missed

A quick roundup of recent signals we’re tracking in parallel.

From our recent coverage:

XPeng self-driving survey reveals stark China-Europe gap. Only 13% of Europeans would ride in a fully self-driving car versus 70% in China, though acceptance converges for assisted driving. Read more

Moonshot AI (Kimi) is in talks to raise $2B at a $30B valuation. The third financing round in under six months, amid soaring capital demand for Chinese AI labs. Read more

Alibaba pivots instant retail strategy from subsidies to infrastructure. Taobao Flash Purchase sets aggressive goals while spending half as much overall, focusing on front-end warehouses. Read more

From Weijin Research:

Supernodes are the New Paradigm of Computing Architecture: Huawei — Huawei argues that in the agentic AI era, scale-up supernodes replace scale-out clusters, reshaping how we think about computing power and business scenarios.

We have tracked Tencent’s deepening e-commerce push inside WeChat’s ecosystem and the broader shifts in China’s AI app landscape as platform giants turn models into product layers. When Alibaba started wiring agent capabilities directly into Taobao, we examined how a super-app can become an action layer. More recently, our look at Meituan’s own AI ambitions highlighted how service platforms are embedding models into real-world transactions. This piece is the next step in that thread.

The Problem Is No Longer the Model

On June 5, 2026, at the Beijing National Convention Center, two of Tencent’s most senior AI figures held a public conversation that was less a product announcement than a statement of strategic intent. Dowson Tang, Senior Executive Vice President and CEO of Tencent’s Cloud and Smart Industries Group, opened by asking Yao Shunyu why he had chosen Tencent at this moment. Yao, Tencent’s chief AI scientist, gave an answer that reframed how the competitive landscape should be read.

Yao is not a routine executive hire. He came through Tsinghua’s Yao Class, earned a Princeton Ph.D., helped define the modern agent toolkit through ReAct and Tree of Thoughts, and then worked at OpenAI on Operator and Deep Research. In Chinese AI circles, he is often grouped with Tang Jie, Yang Zhilin, and Lin Junyang as part of the “基模四杰,” literally the four standouts in foundation models. His Tech Buzz China AI Atlas profile gives him a 9/9 research score, with agent work as the through-line. Tencent recruited him from OpenAI in September 2025. He seems to have been formally appointed Chief AI Scientist by December, reporting to Martin Lau while also heading Tencent’s AI Infra and large-language-model departments. By April 2026, Hy3 Preview was already out under his leadership. Whatever else one thinks about Tencent’s AI lag, that is a very fast reset.

In Chinese tech shorthand, the “second half” means the game has moved past its opening phase. Everyone has seen the basic plays; winning now requires a different strategy. Yao’s version is more specific. For most of AI’s history, the hard problem was methodology: finding better algorithms, architectures, and training regimes. That problem is now largely solved. Pre-training and post-training have produced a universal hammer. The difficulty has shifted to problem selection: which nails are worth driving, and for whom.

That gives Tencent a plausible opening. If the methods are widely available, what is scarce is access to good problems rooted in real user behavior. The company with the most daily-use products has an advantage in finding them. Yao said this was one reason he chose Tencent: the company has many products, many real user contexts, and the environments an agent needs to act. An AI can only order food if it is connected to a tool that can actually place the order.

The environment Yao is describing is WeChat, which together with Weixin reached 1.432 billion combined monthly active users as of the most recent reported period. Every Mini Program, payment flow, and social connection is something an AI sitting on top of that network could act on directly. Tencent wants to turn what users already do inside WeChat into a place where AI can take real actions on their behalf.

The capital spending behind that ambition is large, reflecting the cost of running inference at WeChat scale while also training frontier models. Tencent does not yet have the conversion, yield, or margin data that would show how quickly this pays back. The payoff would have to come from a mix of better ads, more transactions, cloud demand, and cheaper inference.

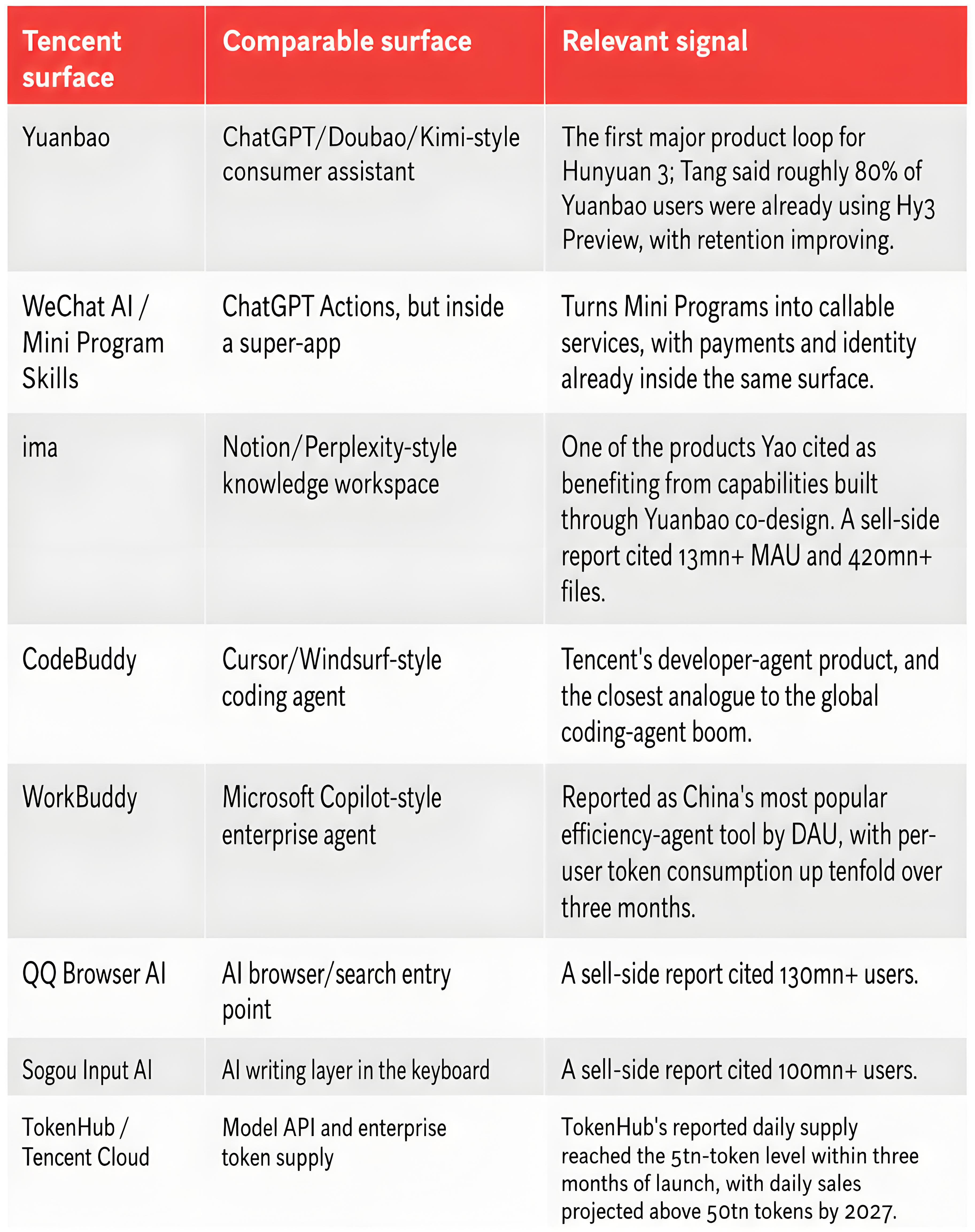

The product is still pre-release: Tencent’s Hunyuan models (Hy overseas), WeChat Mini Program Skills, and third-party services are being linked into a callable layer. Yuanbao has a different job: it is the consumer assistant and feedback surface where Hunyuan improvements are tested in real usage. The June 5 conversation shows the intended system before the public rollout.

The Organization: Foundation, Product, Frontier

Tang is responsible for moving AI capability into products, enterprise customers, and revenue. Yao owns model quality and research direction.

Yao’s shorthand for the organization he wants is a balanced triangle: foundation work, product, and frontier exploration. The idea is to keep the pretraining and post-training infrastructure solid, keep researchers close to real product problems, and still leave room for research directions that do not yet have obvious product homes. His critique of many Chinese AI organizations is that they lean too hard on one or two sides of that triangle and let the other side weaken.

When Tang asked why he had chosen Tencent, Yao pointed to two things: the density of real problems inside Tencent’s products, and company culture. If the harder problem is now choosing valuable problems to solve, Tencent has more real usage contexts than most AI labs. On culture, Yao described Tencent as more trust-driven than metric-driven, which he sees as necessary for long-horizon AI work.

For Hunyuan 3, he translated that view into three changes: rebuilding the pretraining and reinforcement learning infrastructure from scratch; overhauling data and evaluation, including how problems are defined and data is categorized; and treating hiring, release timing, and daily tradeoffs as judgment calls that cannot be reduced to a formula.

Tencent has not presented this as a completed reorganization. For now, it is a working model: Yao is trying to keep foundation models, product feedback, and frontier research in the same loop, while Tang carries the commercialization pressure.

Hunyuan 3: Rebuilding the Engine

Yao’s account of Hunyuan 3 starts with infrastructure, not algorithms.

When Tang asked what specifically changed, Yao was direct: the team rebuilt the infrastructure from scratch, covering both pretraining and reinforcement learning systems, then made substantial changes to data pipelines and evaluation methods. He said the algorithm work was relatively straightforward once those foundations were in place. The harder problems were definitional: how to construct more realistic training problems, broaden the categories of training data, and raise data quality in what he called “an endless pursuit”. The third category was judgment-driven decision-making: choices about hiring, release timing, and daily tradeoffs that do not reduce to a formula.

Hunyuan 3 is not a version increment. Rebuilding the pretraining and reinforcement learning setup means the model was trained on different data and rewarded for different things, not just given more compute on the same pipeline. Yao pushed to cut low-quality training data and shift the goal from benchmark scores toward user experience. A model trained toward product satisfaction will behave differently inside Yuanbao and WeChat than a model optimized mainly for leaderboard scores.

The model rebuild connected to product outcomes through the Co-Design loop with Yuanbao, Tencent’s consumer AI assistant. When Yuanbao’s post-training needed strengthening, the Hunyuan team sent its best post-training engineers to help, even though Hunyuan’s own pretraining was not yet finished. The reasoning was straightforward: keeping Yuanbao’s daily active users up would matter for the model team’s future work, and the two teams working closely together would drive better results down the line.

That decision was internally contested. Yao noted that many algorithm engineers did not understand the rationale and required significant explanation. In retrospect, he argued it was the right tradeoff: it showed the product team that the model team was working in the product’s interest, and that trust was what allowed Hunyuan 3 preview to launch on Yuanbao. Without that trust, the feedback loop would not have held, no matter how cleanly the technical integration was done.

What Tencent learns from Yuanbao does not stay in Yuanbao. Yao argued that the Co-Design process built strong chat and search capabilities into the underlying model, which then carry over to other Tencent products, including ima, the creative collaboration tool, and WorkBuddy, the enterprise productivity application. User interactions across these products feed back into model training, and improved model versions then roll out across all products built on Hunyuan.

Yao’s first public appearance at Tencent was used to explain this system rather than announce benchmark results. Tencent is betting that the feedback loop becomes harder to copy as more products feed into it.

Why WeChat Changes the Agent Problem

For Tencent, WeChat is the obvious place to test whether agents can move from answers to actions. The Mini Program library already gives WeChat 4mn+ lightweight services that run inside the app without a separate download, spanning almost every conceivable use case, roughly the role Apple’s App Store plays for native apps. Add payment credentials, social relationships, and service history, and the AI is operating inside an environment where many user intents already have a path to completion.

When WeChat’s AI calls a Mini Program, the user has already granted trust, WeChat Pay can close the transaction, and Tencent controls the authorization rails end to end. Every completed order, booking, or service request can become payment volume, ad inventory, or a better signal about user intent.

On the user side, the right-swipe AI panel inside chat is still reported as a product test, not something WeChat has fully launched. Developers have something more concrete: a Skill document tells WeChat what a Mini Program can do, what inputs it needs, and what outputs it returns. The AI can then choose the right Skill, pass the required parameters, and keep the user inside the chat instead of sending them to hunt through an app interface.

Automatic mode is for Mini Programs that were never built to be called this way. Once the developer opts in, WeChat’s AI can navigate the interface directly, tapping buttons and filling in forms on the user’s behalf. The other path is custom developer adaptation, which is still in testing. Both paths start from developer authorization.

ByteDance’s Doubao phone-agent effort is the cautionary contrast. Doubao’s agent, preinstalled on ZTE’s Nubia M153, quickly ran into WeChat’s app boundary: users reported WeChat suspensions after using Doubao’s agent to access WeChat, and Doubao then disabled WeChat access. Tencent is taking the opposite route inside its own platform, getting Mini Program developers to authorize access before their services become callable.

Meituan is an exceptionally good early partner for this, so it is no surprise it is among the first use cases. Food delivery is frequent, local, transactional, and already depends on a tight handoff from intent to payment. In the reported flow, a user asks the WeChat AI assistant to order lunch, WeChat’s AI calls the Meituan service through the Skill layer, location and preference data become order inputs, and WeChat Pay can close the loop. JD.com has separately announced an AI agent partnership with Tencent; other reported examples include Didi, KFC, Ctrip, Tongcheng Travel, and Dewu.