China in the Orbital Compute Stack: Where Value Accrues

Physical Constraints and the New Economics of Space-Based Compute

Content

Transmission and communication

What Is Musk Looking for in China

Introduction

In the past fortnight, orbital computing has shifted from a speculative debate to a headline issue in tech and space communities. OpenAI CEO Sam Altman’s public dismissal of Elon Musk’s vision of space-based AI data centers as “ridiculous” in the current era, citing high launch costs and operational challenges, has come into stark contrast with SpaceX’s push to deploy a constellation of AI-focused satellites in low Earth orbit.

The exchange underscores rising tension in 2026: is space really the next frontier for computing, or is it a high-cost distraction from terrestrial solutions? All the while, national and commercial actors are accelerating real efforts in space deployment. Integrating inter-satellite networking and real-time computing capabilities, China has shown that what was once theoretical is now being engineered in orbit, with its own AI satellite constellation.

These concurrent developments, high-profile skepticism from industry leaders, bold strategic bets by space companies, and tangible in-orbit deployments make clear that the discussion around space-based computing is no longer academic. It is now a matter of industrial strategy, technological feasibility, and economic calculus.

This report takes these real-world signals as its starting point. Instead of treating orbital computing as a futuristic theme or conceptual dream, we analyze it as a systems challenge defined by physical constraints rather than just contrasting narratives. Where will structural control and competitive advantage actually accrue in a resource-constrained future.

Enjoy reading!

Yours sincerely,

Rita Luan

Overview

A new contest is unfolding above the atmosphere. It is not primarily about rockets, nor even about satellites. It is about who controls the next layer of computing infrastructure.

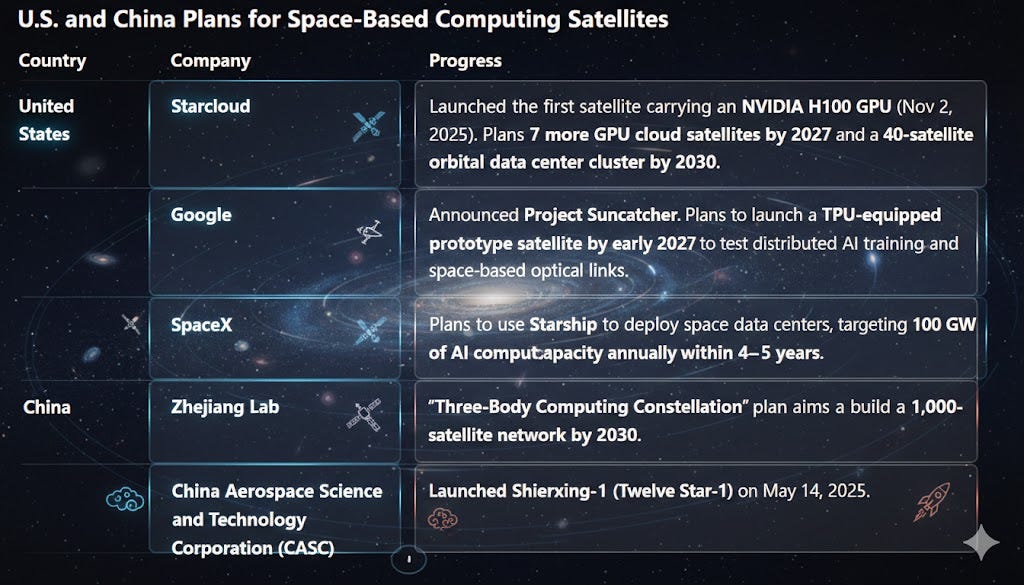

Last November, Starcloud placed an NVIDIA H100 into orbit aboard a SpaceX Falcon 9. The chip, identical to those training large language models on Earth, performed inference in space and processed synthetic aperture radar imagery in real time. The experiment was not a publicity stunt, but a signal. Compute is beginning to migrate upward.

The numbers being discussed are no longer symbolic. Starcloud has outlined a path toward 40 megawatts of orbital capacity by 2030 and 5 gigawatts over time. China’s Three Body Computing Constellation is targeting roughly 1,000 satellites by the end of the decade and a 1 gigawatt orbital data center. Beijing has gone further, outlining plans for more than 1 gigawatt of concentrated space-based computing capacity in Sun synchronous orbit at an altitude of 700 to 800 kilometers. A gigawatt is not a laboratory. It is a power plant.

At prevailing terrestrial construction costs of roughly US$8 to US$10 million per megawatt for AI optimized facilities, single gigawatt capacity implies capital spending of US$8 to US$10 billion before launch costs are considered. That framing matters. Orbital computing is no longer being described in research grants. It is being described in utility scale terms.

For the first time, the market is no longer hypothetical. Industry data compiled at the end of 2025 show that the global space data center sector closed the year at roughly US$8 billion in revenue. Projections now place the market on a trajectory toward roughly US$28 billion by 2030, implying annualized growth north of 35%. US$8 billion is not yet hyperscale territory. It is, however, large enough to attract capital, and growing fast enough to change allocation priorities.

Morgan Stanley continues to project a broader space economy exceeding US$1 trillion by 2040 and has flagged falling launch costs as a potential inflection point for space based computing economics. Goldman Sachs has focused on the terrestrial side of the equation, highlighting how AI is pushing data center power demand toward grid-breaking levels. Neither has issued a dedicated orbital data center model. That omission reflects timing, not disbelief. The capital markets tend to model what already exists, and this is a market that is still being engineered.

The real driver is energy arithmetic. Global data center electricity consumption is projected to approach or exceed 1,000 terawatt hours by 2030 under high growth scenarios. China alone could reach more than 525 terawatt hours, close to 5% of national power demand. At an average industrial tariff of 0.50 yuan per kilowatt hour (≈ US$0.07/kWh at today’s exchange rate), that translates into annual electricity spending of roughly 263 billion yuan (≈ US$36.5 billion). Energy has shifted from operating expense to structural constraint.

Training frontier AI systems already requires hundreds of megawatts. RAND Corporation, a U.S. defense and policy research organization, has suggested that a single future training run could draw as much as 8 gigawatts, equivalent to eight large nuclear reactors operating simultaneously. When one model can rival the load of a regional grid, computing turns into an energy allocation problem.

Orbit offers a different equation. Solar irradiance above the atmosphere is roughly 30% stronger than at sea level. In sun synchronous orbit, capacity factors can exceed 90%. Cooling relies on radiative heat rejection into deep space rather than water intensive evaporative systems. If launch costs fall toward the much cited threshold of US$200 per kilogram later this decade, the cost structure shifts in ways that terrestrial grids cannot easily match. In that world, whoever controls scalable energy in any domain, including space, controls the next phase of the AI economy.

Lift Is the Dividing Line

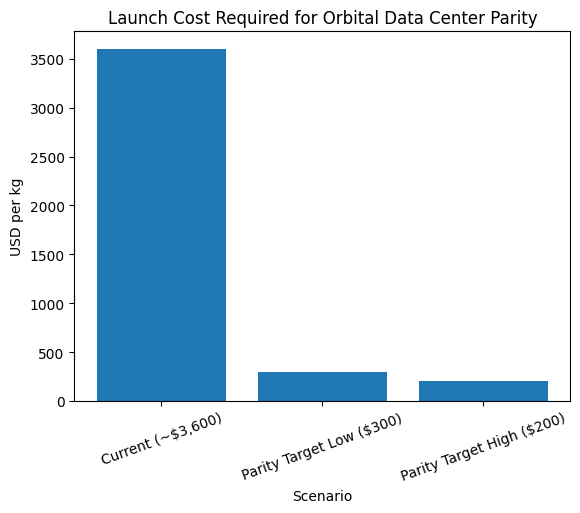

Orbital computing does not begin with chips. It begins with lift. A Google study in November 2025 put the economics bluntly. Launch to low Earth orbit currently runs about US$3,600 per kilogram on SpaceX. For space-based data centers to approach cost parity with U.S. terrestrial facilities, that number must fall to roughly US$200 to US$300 per kilogram:a further 92% to 94% drop. Until then, orbital compute will remain strategically provocative yet commercially limited.

Costs are falling, but not yet to that level. Falcon 9’s list price sits near US$3,000 per kilogram. With aggressive reuse, industry estimates suggest real costs may now be below US$1,500 per kilogram, down sharply from the expendable era’s roughly US$18,500. The U.S. has translated that cost curve into cadence. In 2025 alone, SpaceX conducted 170 launches, accounting for about 85% of U.S. orbital activity.

Regulation tightens the frame. Under International Telecommunication Union rules, low Earth orbit systems typically have about seven years to activate allocated spectrum and orbital slots. Spectrum is a license, not property. High launch frequency is therefore a strategic asset. It secures orbital real estate before the clock expires. Starlink’s edge lies as much in tempo as in price.

China operates at a higher cost base. Reported commercial launch prices range from 50,000 to 100,000 yuan per kilogram (≈US$7,000–US$14,000 per kilogram), with some missions reaching 150,000 yuan (≈US$21,000 per kilogram). Even after declines from 120,000 yuan per kilogram in 2019 (≈US$16,800) to about 80,000 yuan in 2023 (≈US$11,200), the gap with SpaceX remains wide. Launch frequency tells the same story: about 73 Chinese launches in 2025 versus 170 by SpaceX alone.

Scale makes the constraint obvious. A 1-gigawatt orbital data center could require tens of thousands of tons of hardware. At current payload capacities, that means hundreds or thousands of launches. Without low-cost, high-frequency reusable heavy lift, completing such a buildout within a seven-year regulatory window becomes structurally difficult. Time risk becomes capital risk.

The oft-cited US$200 per kilogram threshold is not symbolic. At that level, analysts estimate five-year amortized launch power costs could fall to about US$810 per kilowatt per year, below parts of the U.S. terrestrial electricity range of US$570 to US$3,000 per kilowatt per year. Only near that point does orbital compute approach energy-equivalent competitiveness. The U.S. is pushing toward a US$60 to US$200 per kilogram future with Starship. China is still building its reusable base. The gap may narrow, but the regulatory window will not wait.

Lift has become the dividing line between vision and viability. Yet rockets will not be where the lasting profits sit. As launch scales, it becomes infrastructure, and infrastructure margins compress. Durable returns will belong to those who own what comes after.

Where the Real Constraints Lie

Orbital computing is not yet a business; it is an engineering proposition bounded by physics and capital discipline. Five constraints are typically cited in assessing its viability: energy supply, thermal management, radiation exposure and hardware reliability, launch cost and cadence, and the economics of application demand. All matter, but they do not operate at the same structural level.

Launch cost and workload monetization determine how quickly systems can be deployed and whether revenue models can close. They influence timing, scale, and investor appetite. Over time, however, launch trends toward infrastructure, and applications evolve to match available capability. These variables shape the pace of development, but they do not define the inner limits of the architecture itself.

The more durable constraints are embedded within the system. In vacuum, thermal management cannot be separated from power generation; energy production and heat dissipation scale together, linking compute density directly to mass and structural design. Radiation exposure imposes long-duration survivability requirements on processors and memory that cannot be serviced once deployed, forcing tradeoffs between performance and resilience. Transmission capacity, spanning inter-satellite links and satellite-to-ground networks, determines whether distributed nodes function as an integrated computing platform or remain isolated processing assets.

When reduced to engineering fundamentals, the five commonly cited constraints converge into three structural bottlenecks: the design and scaling of orbital energy systems, the ability to sustain reliable computation under persistent radiation exposure, and the capacity to integrate orbital processing into terrestrial networks through high-bandwidth transmission. These variables define the practical boundaries of large-scale orbital data center construction and form the basis of the analysis that follows.

Engineering limits do not exist in isolation. They are addressed, financed and governed by institutional systems that determine who controls capital allocation, spectrum access, manufacturing depth and network coordination. The practical question, therefore, is not only which constraints matter, but which actors are positioned to manage them.