China's Tesla: Beyond the Car, The Structural Battle for Humanoid Robotics

Two Chinese Automakers' Divergent Strategies: Xpeng's Algorithmic Bet vs. Xiaomi's Ecosystem Scale in the Embodied AI Race

Content

Things That Caught Our Attention

AI’s Bottleneck Is Power. The US and China Feel It Differently.

Instant retail:

Temu isn’t going away (Temu’s GMV forecast).

Introduction

As the Holiday Season arrives, many industries are turning their attention toward next year’s growth opportunities. Yet, beneath the calm of the consumer season, a strategic competition for future industrial dominance is intensifying.

Humanoid robots are no longer a speculative niche. They are becoming a centerpiece of national strategy and industrial competition. On December 3, 2025, reports revealed that the U.S. government is preparing a major robotics initiative, including a possible executive order in 2026 and coordinated programs from the Departments of Commerce and Transportation. This move follows similar strategic planning in China, Japan, and the EU, where embodied AI is increasingly seen as the next frontier after electric vehicles and large language models.

The stakes are rising. Morgan Stanley now estimates the global humanoid robot market could reach $5 trillion by 2050, with over one billion units deployed. That forecast is drawing automakers and tech companies into the same arena. As robotics begin to overlap with EV architecture, from batteries and sensors to autonomous driving stacks, joint ventures and equity tie-ups are accelerating.

For carmakers, the entry point is both technical and financial. A humanoid robot shares key subsystems with an EV, allowing manufacturers to repurpose components and leverage their supply chains. Industry analysts widely believe automakers enjoy a significant cost advantage when entering humanoid robotics — thanks to shared EV supply chains, scale manufacturing and parts reuse.

At the same time, China’s EV market is maturing, with rising price competition and margin compression. Automakers need a new growth story. Tesla’s share price jump after its Optimus announcement made clear that, in the eyes of investors, robots hold more upside than cars.

Chinese firms are positioning for this shift, but not all are taking the same route. Among the most closely watched players are Xpeng and Xiaomi—two companies with radically different strategies for vehicle–robot convergence. One is betting on algorithmic leadership; the other on ecosystem leverage and cost efficiency.

The free section sets the stage: the industry backdrop, Tesla’s strategic template, China’s competitive map, and the early positioning of Xpeng and Xiaomi. From “What ‘Being Tesla’ Actually Means” onward, the article lays out a concrete framework for “being Tesla” in data, costs and profit architecture, then applies it in a side-by-side comparison of Xpeng and Xiaomi—how they differ in strategy, technology and economics, and which is better positioned to capture the humanoid-robotics frontier. Don’t miss this deep dive into the future of embodied AI competition.

Enjoy reading!

Yours sincerely,

Rita Luan

Overview

The public debut of Xpeng’s IRON female humanoid robot sparked a wave of online debate over whether the machine was actually a costumed performer—a controversy that unexpectedly became a lens on how Chinese automakers are entering the embodied-AI race. The robot’s lifelike gait prompted widespread skepticism, leading Xpeng to respond with a single-take video and an on-site teardown. The global attention that followed had little to do with whether the robot looked real. Instead, it offered the first visceral signal to outside observers: Chinese carmakers are now attempting to transfer their autonomous-driving capabilities into humanoid robots, mirroring the strategic arc Tesla has laid out for its own future. Commenting on IRON’s debut, Elon Musk said, “Not bad … Tesla and China companies will dominate the market.”

Tesla has already rewritten its narrative for investors. At the 2024 shareholder meeting, the core performance metrics tied to Elon Musk’s compensation plan were directly linked to the commercialization of Full Self-Driving (FSD), subscription growth, and the production progress of the Optimus robot. Roughly 75% of votes supported the package. Musk has since reiterated on multiple earnings calls that Tesla’s long-term value should not be defined by its vehicle business, but by its autonomous-driving network and robotics segment. The company’s financials increasingly reflect that pivot: software and services have become the fastest-growing revenue lines, FSD subscriptions are expanding rapidly year-over-year, and Optimus is already performing repetitive task trials inside Tesla’s factories. Musk has said the company aims to deploy “thousands” of units in 2025, with an eventual ramp toward an annual production capacity of 50,000–100,000 units—effectively placing the robot into Tesla’s formal capacity-planning cycle. Meanwhile, several Chinese suppliers have disclosed work on “overseas humanoid robot programs,” suggesting Tesla is leveraging its electric-vehicle supply chain to push robots closer to mass manufacturability.

This shift is redefining what merits a premium valuation in the mobility sector. Electric vehicles have entered a price-war cycle that is compressing margins. Autonomous driving and robotics, by contrast, offer recurring subscription revenue, declining hardware costs, and the prospect of large-scale deployment—attributes that capital markets are increasingly willing to reward.

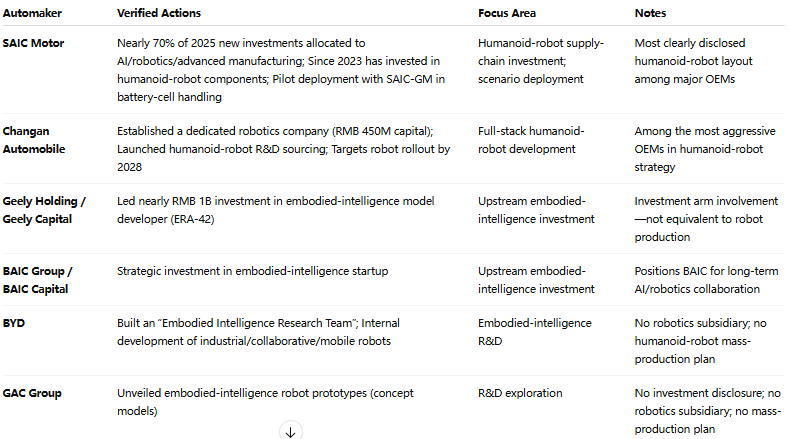

According to incomplete data compiled by Chinese financial media, non–“new-energy EV upstarts” engaging in robotics through in-house development, investment, or equity participation include FAW Group, JAC Motors, Chery Automobile, and BYD. For these companies, investing in or taking stakes in robotics ventures has become one of the most efficient ways to “cross over” into the humanoid-robot sector.

Chinese Automakers’ Humanoid-Robot / Embodied-Intelligence Activities (Non-Exhaustive)

Among the more than 40 Chinese companies that have showcased humanoid-robot prototypes, only two automakers meaningfully meet Tesla’s three-part framework—large-scale vehicle operations, deep autonomous-driving capabilities, and a clearly defined humanoid-robot roadmap: Xpeng and Xiaomi. Both have made robotics a core strategic direction and have invested heavily in advanced driver-assistance and high-level autonomous systems, yet the paths they are taking diverge sharply.

From a technology-roadmap perspective, Xpeng’s actions over the past three months have materially shifted the competitive landscape. The company has committed to mass-producing its IRON humanoid robot by the end of 2026 and plans to launch three Level-4 (L4) Robotaxi models at the same time. Its approach, an end-to-end (E2E) vision system paired with a unified intelligence architecture that powers both cars and robots, most closely mirrors Tesla’s FSD–Robotaxi–Optimus stack. This makes Xpeng one of the few Chinese automakers attempting to train embodied-AI systems using real-world driving data, giving its technology narrative a coherence that stands out in the domestic market.

But what determines whether a company can command a Tesla-style valuation premium is not how closely its roadmap resembles Tesla’s, but whether it can generate scaled, recurring cash flow from real businesses. On this front, Xiaomi’s infrastructure and device-side advantages remain significant. Its AIoT platform surpassed 1 billion connected devices (excluding smartphones, tablets, and laptops) in Q3 2025, providing a massive, steadily growing data stream for its large-model training. The company’s fourth-generation humanoid robot has completed hundreds of hours of testing in factory settings, with deployment plans ranging from hundreds of units to tens of thousands between 2025 and 2027. Backed by a deeply localized supply chain and an extensive hardware footprint, Xiaomi appears better positioned to push robots into mass production quickly. Xpeng, by contrast, excels in architectural consistency, but still needs time to catch up in production capacity, manufacturing efficiency, and ecosystem scale.

Both companies approach their mass-production windows around 2026. But the one that ultimately delivers Tesla-style investor returns will be the company that first turns autonomous driving and humanoid robots into high-margin subscription businesses.

What “Being Tesla” Actually Means

Strip away the futuristic products and look instead at how value is actually created, and “being Tesla” begins with a fundamental truth: it is a scale-driven intelligence business disguised as a car company. In the third quarter of 2025, Tesla delivered 497,099 vehicles and produced 447,450, both record highs. Millions of Teslas on the road generate real-world driving data every day, forming a behavioral dataset that no single Chinese automaker can match. Autonomous-driving specialists often argue that the foundation of end-to-end systems—models trained directly on raw sensor inputs rather than hand-coded rules—is not algorithmic elegance but volume: “enough real, messy data.” High-volume fleets therefore enjoy a structurally higher performance ceiling.

A second component of the Tesla model is the company’s willingness to push compute and model size far ahead of the industry’s comfort zone. In its 2024 third-quarter update, Tesla disclosed that its FSD (Supervised) Version 12.5 had grown to five times the parameter count of its preceding version. It had also installed 29,000 Nvidia H100 chips at its Texas facility, with a year-end target of 50,000. This compute footprint allows Tesla’s driving and robotics systems to iterate on increasingly large neural architectures, producing version-to-version gains in safety and driving smoothness that exceed what rules-based systems typically achieve. The latest FSD v14, offered with a 30-day free trial in North America, doubled the mileage between “critical interventions” in urban settings—from roughly 229 miles in v13 to around 500 miles in v14. The system is far from fully autonomous, but the direction is unmistakable: more data + larger models + more compute.

Tesla’s third structural pillar is its “second hardware curve”. Omdia projects that global humanoid-robot shipments will exceed 10,000 units by 2027 and reach 38,000 by 2030, while Goldman Sachs estimates a $38 billion global market by 2035, with annual demand reaching 1.1 million to 3.5 million units. For Tesla, robots are not simply another hardware category. They are compute multipliers—paired with its world model from autonomous driving, robots can act simultaneously as factory labor and distributed data-collection endpoints, feeding back into the same intelligence loop that powers the vehicle fleet.

Tesla’s financials already reflect this shift. In the third quarter of 2025, the company reported $28.1 billion in total revenue, including $21.2 billion from Automotive sales and $3.42 billion from Energy Generation and Storage. Its “Services and Other” segment reached $3.48 billion, rising approximately 25% year-over-year and continuing its rapid growth. The segment includes FSD software, network services, used-car sales, repairs and insurance—business lines unified by higher margins and subscription-like attributes. Both the energy and services segments now produce significantly higher gross margins than the vehicle business, which continues to face pressure from global price competition, leading to a GAAP gross margin of 18% in the quarter.

On the technology front, Chinese engineers report similar structural convergence. Since 2023, end-to-end architectures—which gradually unify perception, prediction and control—have become one of the dominant approaches across the autonomous-driving sector. Traditional modular pipelines (“perception—post-processing—rules—control”) deliver shrinking marginal gains in complex scenarios. Yet experts stress that the decisive factor is not whether a company adopts end-to-end models, but whether it can maintain a stable, high-frequency data-feedback loop: generating, cleaning, labeling and re-training on real-world data at scale. Companies with large fleets and self-owned cloud infrastructure are naturally better positioned to replicate Tesla’s rapid iteration cadence.

Taken together, these elements clarify the real meaning of “being Tesla.” The company’s valuation premium rests on three underlying variables:

A data ceiling defined by real-world scale.

The accuracy of an end-to-end system is determined less by algorithmic ingenuity than by how many long-tail scenarios the fleet has encountered on actual roads.A cost curve shaped by iteration speed.

The leap from FSD 12.5 to v14 demonstrates that the ability to complete training, deployment and retraining cycles quickly is what allows a unified model for cars and robots to approach practical reliability—and push the marginal cost of hardware toward zero.A profit structure built on a second hardware curve.

Financial disclosures show that software, energy and services are Tesla’s fastest-growing and highest-margin segments. Only when autonomous driving and robotics enter measurable subscription structures does an automaker’s valuation begin to resemble that of an AI-and-robotics network rather than a traditional car company.

These three variables correspond to technical ceiling, cost floor and profit architecture. They form the benchmark for evaluating whether any company, not only in China but globally, can pursue Tesla-style capital returns. They are also the only meaningful baseline against which to assess contenders in the next wave of autonomous driving and humanoid robotics.