Tencent’s e-Commerce Revival. Part 2: WeChat's e-commerce ecosystem

How Tecent is building true social commerce.

Contents

Things that caught our attention

These topics are mostly posts that Rui Ma and Ed Sander share on Twitter and our Substack Notes. Follow us there for shorter, worthwhile insights that won’t get their own deep-dive report.

Introduction

In June, we took a deep dive into WeChat’s new Send Gift function and shared its results so far and expectations for the future. The launch of this function is a sign of Tencent’s renewed interest in e-commerce.

Another indication that Tencent is reconsidering the role of e-commerce is that the topic was prominently featured in the annual WeChat Open Class held on January 9th. At the closed-door conference, plans for Send Gifts were discussed, as well as those for strengthening the link between various parts of its ecosystem: mini-programs, WeChat Stores and Service Accounts.

In this second part of our investigation into Tencent’s e-commerce revival, we take a closer look at the way WeChat’s ecosystem facilitates e-commerce.

The free section of the report below explains Tencent’s vision for WeChat e-commerce. Paid subscribers get full access to this report and will learn about the role the various components of that ecosystem play in growing e-commerce.

Become a paying subscriber to unlock the full report and support our in-depth research into key China tech trends.

Next week, in the third and final part of this series, we will explore the challenges WeChat has in making e-commerce successful and what the outlook for the future is.

Ed Sander, Tech Research Analyst

WeChat’s vision for e-commerce

WeChat has never been a key player in the e-commerce market and has even sold all of its e-commerce initiatives to JD.com at one point. Nevertheless, significant e-commerce and local services trade is facilitated in the WeChat ecosystem. In the WeChat ecosystem, mini-program payments account for a substantial share of the total e-commerce GMV. Currently, WeChat has about 80 million active e-commerce users, with annual mini-program e-commerce GMV approaching RMB 1 trillion.

Tencent is using WeChat's massive user base and social network advantages to develop its e-commerce business. By creating a social shopping environment, Tencent aims to attract consumers who are not interested in traditional e-commerce, thereby differentiating itself in a highly competitive market and increasing the platform's activity and user stickiness. This strategy aims to increase sales and customer loyalty while attracting more merchants to the platform and increasing the variety of goods.

Although Tencent predicts that competition in the e-commerce market will remain fierce, it believes that there is still great potential for development in the social networking area. To enhance its market competitiveness, Tencent is implementing a product innovation and differentiation strategy, of which the gift-giving function of WeChat Store is one example. This approach not only increases user activity but also enhances the platform's stickiness, laying a solid foundation for Tencent's development in the e-commerce field.

e-Commerce ecosystem

The operating model of WeChat e-commerce is significantly different from that of traditional e-commerce platforms. In WeChat’s ecosystem, e-commerce channels are rich and diverse, including public accounts, WeChat Channels, and music discovery feature Tingyiting, among which WeChat Channels is one of the largest traffic entrances.

WeChat e-commerce has adopted a unique decentralised strategy, integrating e-commerce functions as a component into the entire ecosystem, which is very different from the traditional Taobao platform. As a transaction service component, WeChat Stores does not have a central entrance like conventional e-commerce platforms, but primarily provides services through content, messages, and accounts. This model presents new opportunities and challenges for merchants and consumers, making e-commerce activities more flexible and diverse.

Zhang Xiaolong (Alan Zhang), president of the WeChat business group, has never been in favour of selling things through livestreams. He thinks it’s too monotonous and noisy. Still, he didn’t interfere when WeChat Channels started allowing live commerce. However, at a Tencent conference on November 11th 2024, he laid out his vision for e-commerce to his Tencent colleagues. He wanted product information to roam freely in WeChat, just like pictures do. Commodity transactions should not be limited to e-commerce for WeChat Channels; instead, they should be a transaction component of the entire WeChat system. They should be able to move freely in WeChat and be combined with other modules, such as red envelopes, payments, and mini-programs, to generate synergy. [1]

As anybody who uses WeChat knows, Tencent has created an impressive ecosystem inside the app. However, there has always been room for improvement in connecting the various elements of the ecosystem, and e-commerce seems to be a good reason to do that now.

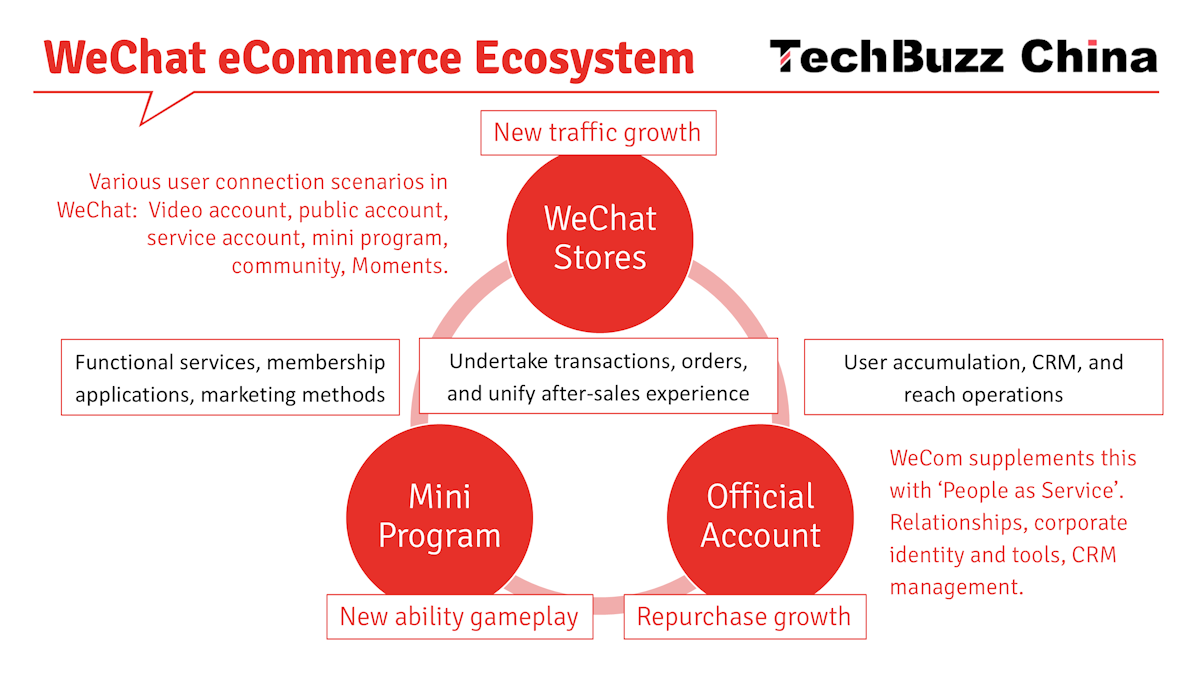

According to the WeChat team's plan, WeChat stores, mini programs, and service accounts will form a "three-in-one" system in the WeChat e-commerce system. The idea is that WeChat stores will be where transactions and after-sales services occur. Mini-programs will be used for functional services, while memberships and marketing and service accounts (a type of public account) should drive retention and repurchase. [2] In other words, mini-programs will serve as brand websites where people can learn about brands. WeChat Stores are where they make purchases, and they will become fans by following Service Accounts. By integrating the ecosystem of WeChat stores, mini-programs and WeChat Channels, Tencent hopes to drive a new round of growth for the overall business.

Translated slide presented during the WeChat Open Class held on January 9th, 2025. Source: 36Kr

WeChat has traditionally been cautious in e-commerce, employing strict review standards, high deposits, and restricting many product categories. However, in the Open Class in January, it was announced that WeChat would open all categories, lower commissions, and no longer request deposits. It seems like Tencent is serious about giving e-commerce another try.

The WeChat e-commerce ecosystem consists of these main components:

Below, we will dissect the several key parts of the WeChat e-commerce ecosystem and how they interact.

WeChat Channels

We reported extensively on WeChat Channels, the short video and livestream functionality inside WeChat, in 2023 and 2024. You might also want to refer to those reports for background information on WeChat Channels.

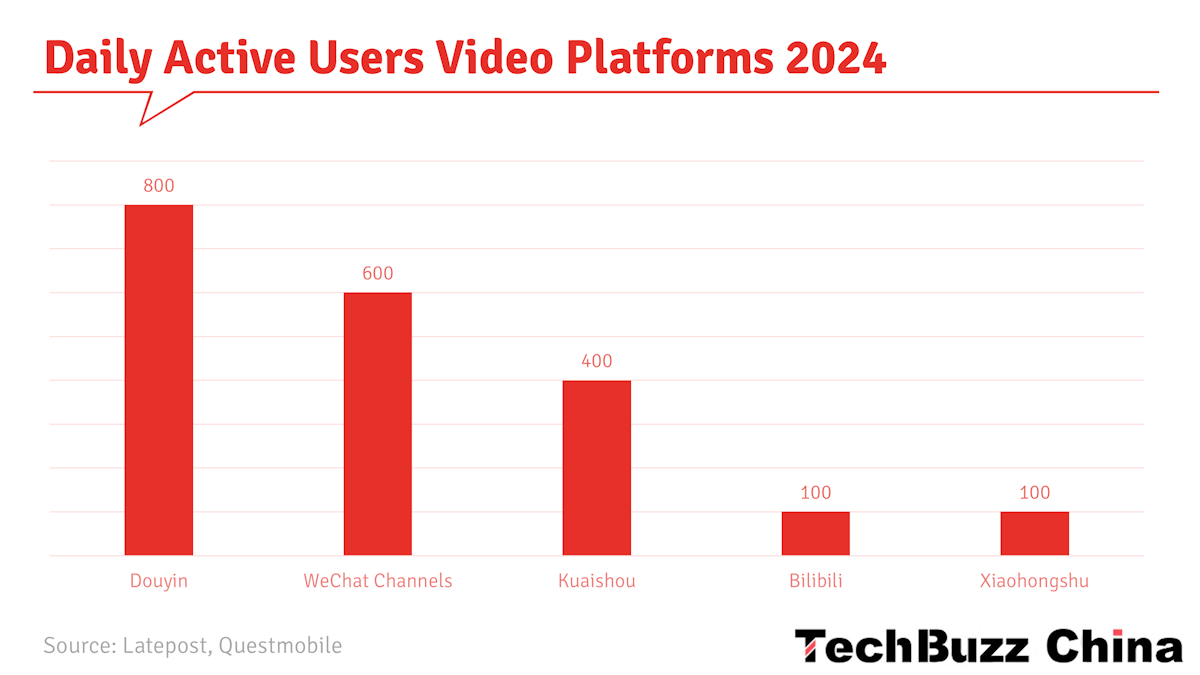

WeChat Channels has overtaken Kuaishou and become China’s second-largest video platform based on daily active users. The number of daily active users of WeChat Channels has reached 600 million, based on the standard that users watch a 15-second video in full. The next goal of WeChat Channels is to increase the number of daily active users to 800 million, aiming to reach a user base comparable to WeChat Moments.

The average daily usage time of Douyin and Kuaishou users has exceeded 120 minutes, whereas WeChat Channels users spend only 70 minutes, indicating WeChat Channels still has significant growth potential. However, although the short video field has broad prospects, it remains to be seen whether WeChat Channels can reach the level of its competitors (see ‘Challenges’).

Although WeChat Channels has less usage time than its competitors, it has significantly increased WeChat's overall usage time. In contrast, Moments' usage time remained unchanged, while public accounts saw a decrease. WeChat users now spend an average of 100 to 110 minutes per day on the WeChat app. Although WeChat Channels and Moments overlap in some aspects, each product is designed for different needs, so WeChat Channels have a limited impact on the usage time of other functions.

Compared with Douyin and public accounts, the user base of WeChat Channels is quite unique. Compared with Douyin, WeChat Channels have a higher age level, a larger proportion of male users, and are more distributed in second- and third-tier cities. However, compared to users of public accounts, the user base of WeChat Channels appears to be younger and more urban. In terms of content, Douyin primarily focuses on entertainment themes, including pop music, fashion, beauty, humorous pet videos, and short dramas. In contrast, WeChat Channels concentrates more on financial, news and educational content.

In terms of traffic sources, almost half of the traffic of WeChat Channels comes from the private domain (‘owned traffic’ from people who follow accounts), mainly relying on social networks. Users primarily access WeChat Channels through Moments or group sharing and browse less actively. The expansion of the WeChat Channels market mainly depends on algorithm recommendations and the improvement of public domain traffic. The public domain traffic of WeChat Channels has now exceeded 50%, and the growth rate is high.

As a multi-functional platform, WeChat Channels has many unique advantages. First, it encompasses a range of usage scenarios for social interaction and capturing daily life. Second, it meets users' ‘peeping’ needs, such as viewing the interactive content of their contacts in the WeChat social network, which is a function that Douyin does not have because it’s not a social network. In addition, WeChat Channels integrates functions such as e-commerce and local services, which help to extend users' usage time.

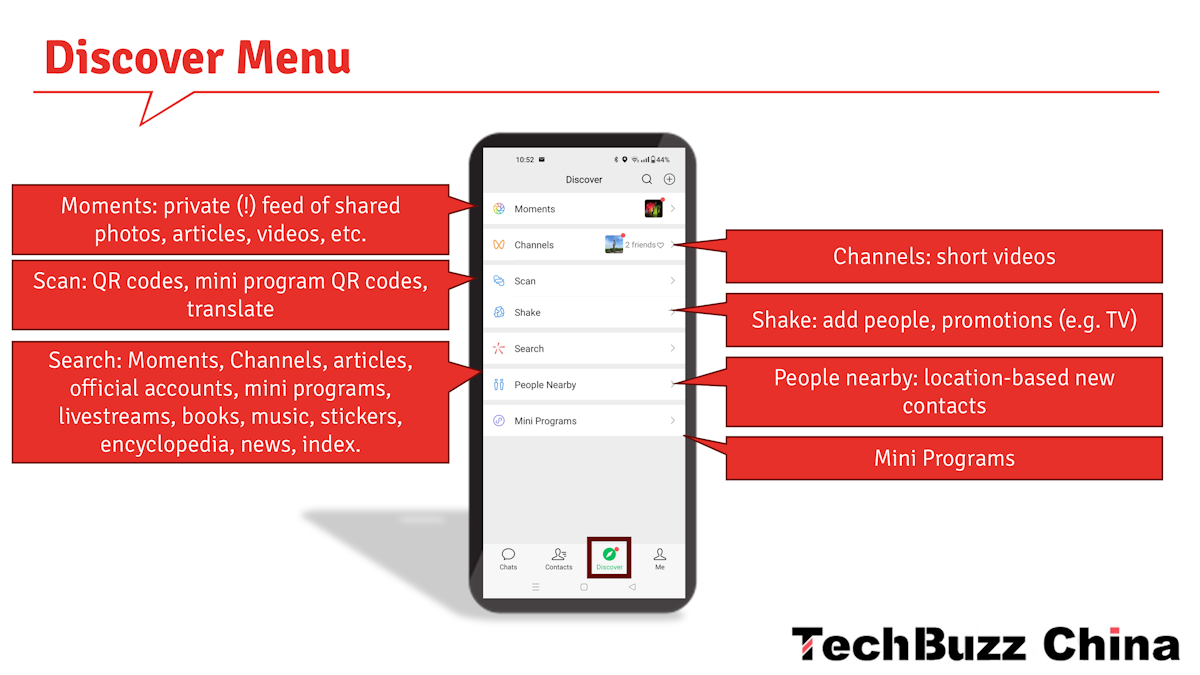

The claim that WeChat Channels will be added to the fifth menu bar at the bottom of WeChat is not correct, according to Tencent. The four menu bars at the bottom of WeChat (Chats, Contacts, Discover, Me) symbolise its primary functions, covering accounts, social relationships, messages and plug-ins. The core design concept of WeChat is reflected in the Contacts, which remains in the second position despite its low frequency of use. WeChat Channels is classified in the ‘Discover’ category, which will not affect the existing design classification and hierarchy of WeChat. The entrance to WeChat Channels will continue to remain in the ‘Discover’ menu without any changes.

Note: Shake has been removed from the Discover menu.

WeChat Channels are actively taking steps to increase the platform's influence and user growth. Attracting more KOLs/anchors (livestream hosts) and well-known brands to join will become a key strategy to influence consumer behaviour. To achieve this goal, WeChat Channels has begun signing agreements with partners to increase traffic and expand their influence. In addition, in order to attract more merchants to join, WeChat Channels may implement some preferential measures in the near future. These measures are designed to enhance the platform's competitiveness and provide users with richer, more valuable content.

WeChat Channels has undergone several important changes between 2023 and 2024. First, Tencent now provides traffic support for high-quality content, and even without advertising, high-quality content has the opportunity to increase its fan base. Secondly, WeChat Stores merged with WeChat Channels Stores (see ‘WeChat Stores’).

WeChat Stores

The term ‘WeChat Stores’ (微信小店, literally WeChat Small Stores) can be a bit confusing. To clear things up, let’s first look at its history over the past 10 years.

History of WeChat Stores

In March 2014, WeChat introduced WeChat (Small) Stores, a shopping function, to service accounts (a type of official account). The functionality was open to ‘official accounts that are verified by WeChat and qualified for using WeChat Pay’. [3] A limitation was that the store was only accessible to those who already followed the official account. Products also had no reviews or ratings, and, in those pre-Douyin days, consumers were not used to buying goods in a social app. [4]

Besides WeChat’s own WeChat Small Stores, there were external SaaS platforms like Weimob, Youzan, Mengdian and YouShop. Confusingly, the latter’s Chinese name, Weidian (微店, literally Micro Store), uses the first and last character of the Chinese name for WeChat (Small) Stores.

In 2015, iResearch found that purchase frequency in WeChat Stores was low. Most WeChat users had not developed a habit of shopping online through WeChat Stores. What’s more, the sources of the goods were not reliable, and it was easy to purchase the same products through other channels. iResearch believed WeChat would not become the main shopping channel in the short term. [5]

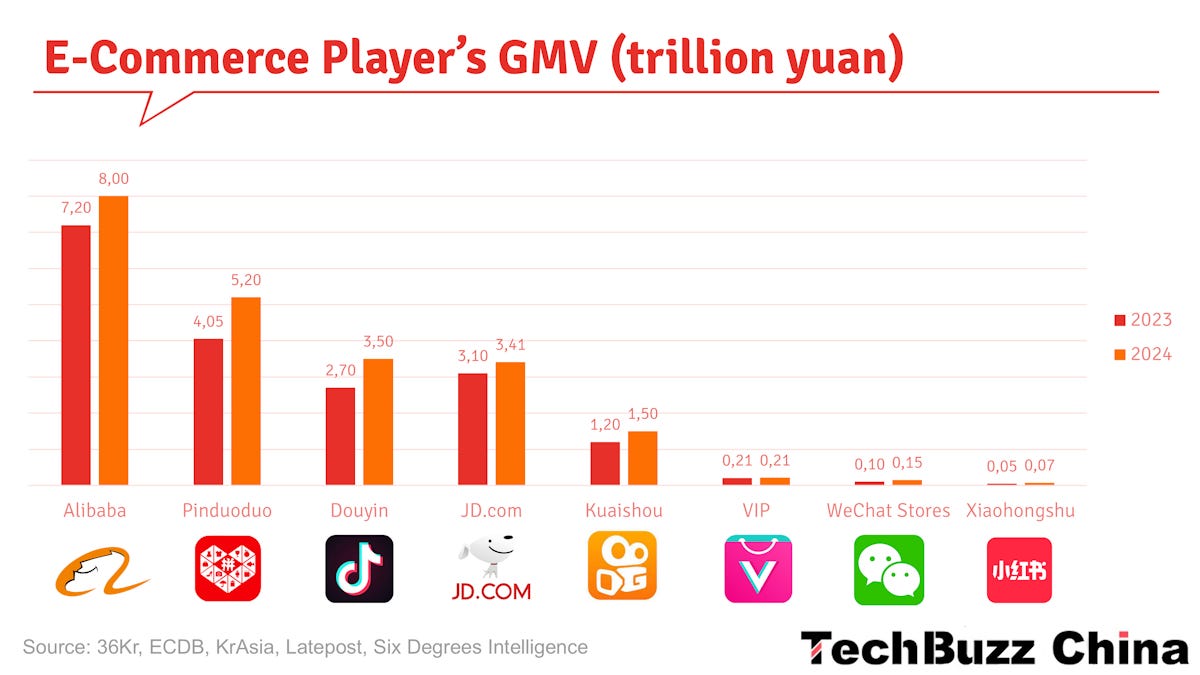

In 2016, iResearch reported that WeChat eCommerce had a GMV of RMB 329 billion. [6] At the time, the size of the Chinese e-commerce market was about RMB 5 trillion. In other words, WeChat had only conquered 6.5% of the market. The estimation at the time was that WeChat’s GMV would reach about RMB 1 trillion in 2019. However, in the years that followed, new players such as Pinduoduo, Douyin, and Kuaishou emerged on the scene and captured significant shares of the e-commerce market. WeChat Stores slowly became irrelevant.

In April 2017, after the launch of mini programs, WeChat launched the Store Mini Program (门店小程序, Mendian Xiao Chengxu). Between 2019 and 2021, WeChat shifted its focus from WeChat Stores to Store Mini Programs and the aforementioned third-party platform tools. WeChat Stores were discontinued in 2021.

Meanwhile, the GMV of WeChat Channel Stores exceeded RMB 100 billion in 2023. But for WeChat, which had more than 1.3 billion users (including overseas versions), this was not an ideal result. By comparison, two years after its establishment, Douyin e-commerce has exceeded RMB 750 billion in sales. [1]

In August 2024, Tencent announced that it would upgrade its WeChat Channel Stores (视频号小店) to WeChat (Small) Stores (微信小店), using the same name as the old 2014 feature it had shut down three years before. WeChat Channels no longer provide independent transaction functions, and merchants now need to use WeChat Stores to conduct transactions instead.

Compared with the previous WeChat Channels Stores, the store and product information of WeChat Stores can be circulated in multiple WeChat scenarios, including public accounts (subscription accounts, service accounts), WeChat Channels (live broadcasts, short videos), mini programs, and search. [7]

WeChat Stores today

The (re)launch of WeChat Stores is aimed at building a complete e-commerce system, but it is still in its early stages. New features, such as gift giving, have entered the testing phase, but the overall function still needs further improvement and has great development potential, according to Tencent. Additionally, the gift-giving function of WeChat Store may be difficult to replicate on other platforms, which lack integration with a social network.

Tencent's e-commerce business model is now mainly operated through WeChat Stores, and all transactions are carried out through the WeChat payment system. If a merchant wants to operate multiple categories, he needs to pay the corresponding deposit. In terms of transactions, Tencent charges a technical service fee ranging from 3% to 10% for each transaction, which is similar to Tmall's charging standards. In addition, when using WeChat Pay, a 0.6% handling fee will be charged for each transaction.

WeChat Stores currently have a relatively low position in the Tencent ecosystem, accounting for less than 2% of the total GMV, which is almost negligible compared with mini-program e-commerce. The GMV of mini-program e-commerce has reached the trillion-dollar level. In 2023, the GMV of WeChat Channel Stores exceeded 100 billion yuan, and in 2024, it was expected to reach 150 billion yuan, although the growth rate has slowed down.

Compared to other e-commerce players in the Chinese market, WeChat Stores remains insignificant. While it had a higher GMV than Xiaohongshu in 2024, it was still smaller than VIP Shop.

Like WeChat Channels, the traffic sources of WeChat Stores are mainly concentrated in the private domain (followers), accounting for about 90%, while public domain traffic accounts for only about 10%. Therefore, the future growth potential of WeChat Stores lies mainly in the development of public domain traffic.

At present, many well-known brands have begun to establish a presence in the WeChat ecosystem, with notable areas including clothing, jewellery, and health products. However, traditional categories such as beauty, home cleaning and home appliances have not yet achieved scale in the WeChat ecosystem.

To further increase transaction volume, WeChat Channels and WeChat Stores need to strengthen traffic diversion strategies. Merchants choose WeChat Stores because they provide unique activities and functional support. At the same time, WeChat Channels can provide merchants with more exposure opportunities than other advertising channels.

Merchant and user recruitment

For merchants seeking support and traffic, WeChat Stores has become the preferred platform. By the end of 2024, the number of merchants in WeChat Stores was about 20 million, covering multiple categories. However, the share of monthly active merchants was only 20%. Meanwhile, there were close to one billion mini-programs in WeChat.

WeChat Stores have implemented various measures to attract merchants and consumers, thereby enhancing sales performance and user engagement. First, they provide merchants with an annual marketing schedule to help them prepare in advance for promotional activities during key festivals, such as the Spring Festival, Mid-Autumn Festival, and National Day. At the same time, WeChat Stores have launched a variety of preferential activities covering all product categories, including discounts and limited-time sales, and encouraged anchors to participate.

During the hot season, WeChat Stores also launched unique activities, mainly promoting cooling equipment and drinks, and providing limited-time discounts and free shipping services. In addition, WeChat Mini Programs attract new users and increase order conversion rates at a lower cost by providing interactive marketing tools such as group buying and lucky draws.

WeChat Stores makes full use of the dissemination effect of social platforms and integrates the resources of the WeChat ecosystem. This year, they will encourage users to share links in Moments and group chats to get rewards, thereby raising brand awareness. WeChat Stores will also strengthen its integration with the WeChat ecosystem and improve product displays and purchase links in public account articles. They also plan to expand into offline promotion by cooperating with physical stores to conduct scan code shopping activities and recommending products through WeChat Pay.

In addition, WeChat Stores will cooperate with WeChat Channels to provide traffic support and technical assistance to high-quality merchants, and use the live broadcast function to achieve instant purchases. They can directly guide viewers to place orders on WeChat Stores, realising the seamless connection between live broadcast and e-commerce.

WeChat has launched these various incentive measures, but requires users to interact within the platform. Some functions will no longer be open to external platforms, and the platform will guide users to WeChat Stores for transactions.

Tencent has provided substantial traffic subsidies for the WeChat Channels entrance, targeting 100,000 white-label merchants with over one million followers. These white-label merchants generate 2 to 3 million yuan in daily transactions and receive free advertising display. Future subsidy plans will cover more industries, including beauty, fast-moving consumer goods and electronics.

Mini Programs vs WeChat Stores

In the second half of 2023, WeChat Channels started encouraging offline merchants to operate in both the private and public domains. The team initially focused on chain brands, aiming for each store to attract offline customers through a WeChat official account. They would then encourage these customers to place orders via the WeChat Channels Store during live broadcasts. [1]

However, many brands and dealers were unfamiliar with operating private domains, and those who could manage communities were not necessarily inclined to direct customers to live broadcast rooms for transactions. Some merchants questioned, "Why do we have to open a WeChat Channels Store when we already have a mini program?" The mini program establishes a direct connection between the brand and the customer, with all transaction revenue belonging to the brand. In contrast, the WeChat Channels Store have a large but uncontrollable flow, necessitating revenue sharing with the platform. [1]

As a compromise, WeChat Channels agreed to allow brands to display their own mini-programs in the live broadcast room without opening a WeChat Channels Store. But new problems arose. The requirements for products in the mini-programs and WeChat Channels Stores were different, as were the return and subsidy policies. This led to a split in user experience, and the pressure of customer complaints from merchants and platforms rose sharply. Merchants such as Luckin Coffee and Burger King even complained to WeChat headquarters about the confusing experience, as they are all important advertisers of WeChat. Soon, the business stopped this practice. [1]

So, with WeChat Channels now requiring WeChat Stores for transactions, should merchants get a mini program or a WeChat Store?

Mini-program e-commerce differs significantly from WeChat Stores in terms of development complexity, function selection, data display and traffic distribution. Developing a mini-program e-commerce solution requires coding and custom design, which can be expensive and time-consuming. In contrast, with WeChat Stores, one only needs to apply for use. Mini-program e-commerce can design various functions, such as membership systems, interactive games, coupons, and group buying, whereas WeChat Stores have fixed functions and poor scalability.

In addition, the data panel of mini-program e-commerce can be customised, including brand logos. In contrast, the display of WeChat Stores is relatively concise. In the process of transforming from mini-program e-commerce to WeChat Stores, the degree of dependence of enterprises on service providers changes (see ‘Service Providers’). These factors are key considerations that merchants should take into account when selecting and utilising these tools.

When choosing an e-commerce platform, merchants need to weigh the pros and cons of the short-term and long-term. At present, the customised service fees provided by service providers are relatively low, with a handling fee of about 1% and a service fee of about 5%, so merchants may not completely abandon mini-program e-commerce in the short term. In the future, merchants may adopt a dual-track strategy, continuing to maintain the existing mini-program e-commerce business while introducing the application of WeChat Stores.

Brands can operate customised mini programs and WeChat Stores at the same time. The two channels can complement each other. However, the main challenge currently faced is the migration of member data, especially when transferring data from third-party platforms, which may have a certain impact on user experience. To meet this challenge, some brands choose to manage both channels simultaneously to avoid data problems. This strategy enables brands to fully leverage the benefits of both channels while maintaining data integrity.

The WeChat Store platform will charge a fee of 2% - 3%, all of which belongs to Tencent. At the same time, operating service providers can obtain a tiered service fee of up to 5% per year. Whether merchants choose to use mini-programs or WeChat Stores, the fees charged by relevant service providers are approximately between 4% and 5%. Still, mini-programs will have a one-time development fee in the early stage. This choice may have a substantial impact on the merchants' operating strategy and profit model. They need to weigh factors such as cost structure, platform functions, and user experience according to their situation.

WeChat Search

In the third quarter earnings conference call in 2024, Tencent Chief Strategy Officer James Mitchell said that Tencent planned to add search functions to WeChat Channels and mini programs, use search technology to optimise information flow, and add commercial search entrances in different locations. According to data from other live e-commerce platforms, consumers who arrive through keyword searches tend to have a higher conversion rate. [7]

"We hope to create a unified and trustworthy shopping experience through the WeChat ecosystem. The key lies in indexing and standardisation." Tencent President Martin Lau said that in the future, Tencent hopes to form more incremental closed loops through the combination of WeChat Channels and WeChat Search, and use AI big models to improve the relevance of search results. [7]

WeChat's Search function has shown great potential in terms of user growth and commercialisation. Currently, the function receives a staggering 600 million searches per day, with 250 million active users, resulting in an average of slightly more than two searches per person per day. The usage and user base of the function have maintained a growth rate of between 20% and 30% every year.

As can be seen in the screenshots below, the results of WeChat search open up many commercial links.

The search results in WeChat are grouped in categories, arranged in tabs at the top. Some of these offer commercial opportunities. A search for the assorted nuts brand Three Squirrels results in several WeChat Stores selling their products, with the official WeChat Stores of the brand at the top. The Account tab displays the official account and mini-program of the brand. The product page showcases a variety of products from the brand. Clicking on these will direct people to the concerned product in a WeChat Store. The video tab shows the brand's WeChat Channels account, which, as discussed, can also be linked to its WeChat Store.

Despite the enormous commercial potential of WeChat's search function, its current level of monetisation is still low. WeChat's AI search function has begun to try to make money, but it is still in the early stages. Compared to traditional search engines such as Baidu, its core indicators still have considerable room for improvement. Nevertheless, artificial intelligence technology brings more possibilities for the innovation of search products (more on this in part 3).

At the same time, the diversification of WeChat Channels’ content and the introduction of various services such as WeChat Stores have further promoted the growth of search demand. These factors have jointly created favourable conditions for the development of the ‘Search’ function. This means that the ‘Search’ function still has excellent development potential in the future and may achieve greater breakthroughs in user experience and commercialisation.

Building WeChat Mall

All the e-commerce features in which transactions take place on WeChat, including mini-program stores, WeChat Stores and third-party integrations like Youzan and Weimob, are collectively (and confusingly) referred to as ‘WeChat Mall’.

In its development strategy for 2025, WeChat Mall has three key aspects:

Expanding the corporate customer base.

Using the marketing tools of social platforms to establish a stable consumption model.

Enhancing social media shopping behaviour and customer loyalty through artificial intelligence and big data technology.

There are significant differences in the operating philosophy and market positioning between WeChat e-commerce and traditional e-commerce platforms. The core of WeChat e-commerce focuses on meeting users' transaction needs and leveraging the platform's capabilities to achieve this, with the growth of GMV as a secondary objective. This differs from the operating philosophy of traditional e-commerce platforms, such as Pinduoduo and Tmall. If GMV decreases, it will have little impact on the WeChat platform as a whole.

As such, WeChat Mall currently prioritises steady development over rapid GMV growth, primarily achieving this by enhancing user stickiness. Despite this, WeChat Mall still sets a challenging goal: the annual transaction volume growth rate must exceed 30%, and the target growth rate for certain specific industries even needs to reach more than 50%.

This seemingly contradictory strategy is closely related to the core advantages of WeChat Mall. The primary advantage of WeChat Mall lies in its social attributes, which aim to integrate the e-commerce ecosystem with the social functions of WeChat, rather than merely being a traditional e-commerce platform. Based on this unique positioning, the platform pays more attention to the user's purchase frequency and recognition rather than the single consumption amount. This strategy aims to increase user activity and dependence, thereby achieving stable and sustainable growth in the long term.

The rise of WeChat Mall is expected to have a significant impact on content e-commerce platforms such as Douyin and Kuaishou. WeChat Channels will become an essential platform for content dissemination and merchandise sales. Users watching content on WeChat Channels may reduce their time on Douyin, which will have an impact on the business of Douyin and Kuaishou. Compared with its competitors, WeChat still has excellent potential for improvement in this area.

Service providers

Tencent adopts an outsourcing model to manage WeChat Stores, mainly to focus on technology development and hand over user and business affairs to third parties. In this model, external service providers help small and medium-sized enterprises manage their private domain traffic, while large enterprises have more autonomy in this regard. The advantage of this model is that service providers have rich experience in managing merchant resources and private domain traffic. At the same time, Tencent protects the user experience by limiting the openness of APIs. This approach not only meets the needs of merchants of different sizes but also provides Tencent with a scalable business ecosystem.

Mini programs, which fall into the category of private domain traffic, are usually developed by merchants themselves or built with the help of third-party platforms. The operating model of WeChat Stores enables the establishment of up to 30 stores with a single business license, providing merchants with the convenience of diversified operations.

Examples of service providers are:

Weimob Group, one of the leading e-commerce service providers on the WeChat platform, focuses on providing a full range of e-commerce solutions. Weimob Group integrates public domain resources and uses membership systems and marketing activities to enhance the value of private domain traffic.

Youzan has a significant impact on the construction of WeChat Mall. Youzan supports a range of product display formats and flexible store designs, offering a variety of marketing tools, including coupons, full discounts, and limited-time discounts. In addition, Youzan's analysis tools provide the necessary data support for merchants' operational decisions.

Pairui Weixing, a subsidiary of the Zhejiang Women's Federation of Culture and Arts, is also one of Tencent Advertising's main partners. Pairui has performed well in the field of performance advertising, especially in promoting categories such as clothing, beauty and daily necessities.

Weimeng (see below).

These service providers help merchants enhance operational results and user value through their respective advantages and characteristics, thereby promoting the overall development of the WeChat e-commerce ecosystem.

Service providers can also help with WeChat Channels. There are two main ways for large enterprises to operate on the WeChat Channels platform: building their own team or outsourcing management. Major companies in the cosmetics industry, such as Chando and Lin Qingxua, have begun to outsource the operation of their WeChat Channel accounts to external teams.

All the transaction fees inside WeChat belong to Tencent, and partners don’t get a share of them. So, how do partners make a profit? Their primary source of income is to provide the services mentioned above, especially to connect resources for small businesses. In addition, they can also earn income through various channels such as WeChat Channels advertising, live broadcast operations, store management and community maintenance. The core value of partners is to support merchants lacking a mature operational team in e-commerce, a value that is particularly important.

The rise of WeChat Stores is both a challenge and an opportunity for third-party service providers. WeChat Stores initially allowed merchants to use mini-program stores developed by third parties, such as the solutions provided by Youzan and Weimeng. However, when Tencent relaunched its WeChat Stores product, enabling merchants to operate e-commerce without purchasing additional systems, it had an impact on SaaS service providers. The primary source of income for Youzan and Weimeng is merchants purchasing mini-program store services, which usually cost RMB 12,800 or RMB 19,800, but Tencent's new model has lowered the threshold for use.

Tencent's decision to build its own ecosystem has made it challenging for service providers to retain their customers, especially small customers. Tencent's new backend design is similar to Taobao or Douyin e-commerce, making it easier to operate and more attractive to merchants. In comparison, the complex SaaS system seems less popular. However, since many merchants are not familiar with the operation of WeChat Stores, this provides new business opportunities for third-party service providers. Service providers can increase their revenue by providing operational support and developing marketing tools centred on WeChat Stores.

Advertising in the ecosystem

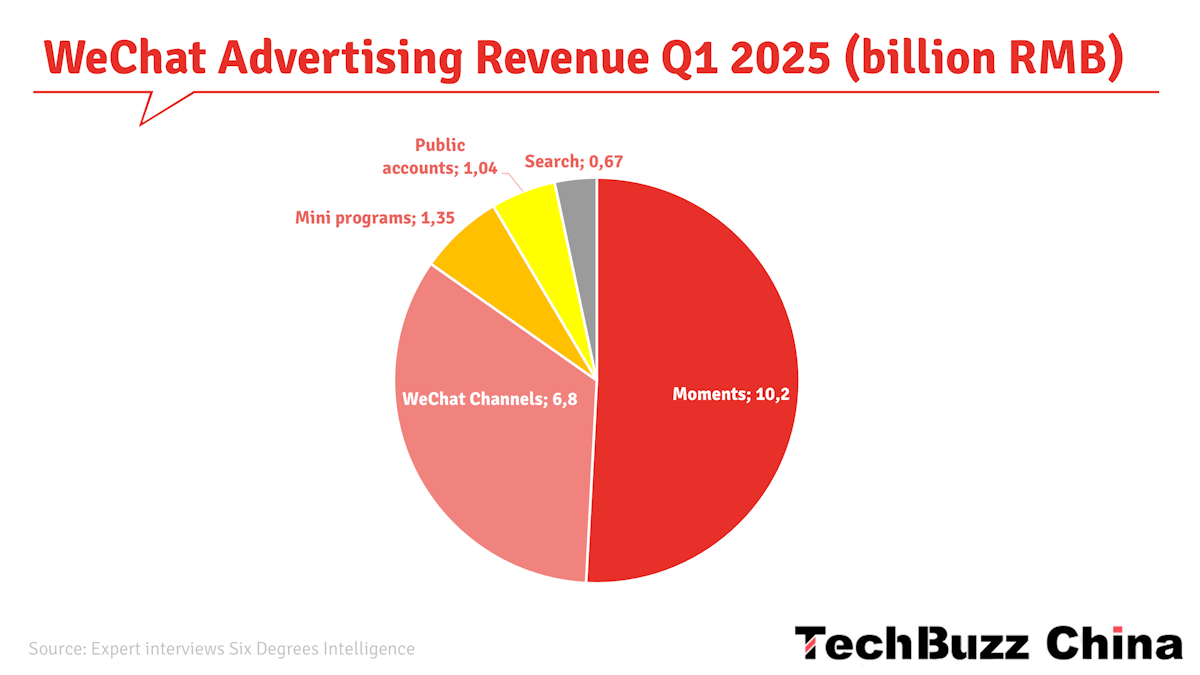

Tencent's advertising revenue in the first quarter of 2025 was about RMB 31 billion. Among them, WeChat's advertising revenue performance was the most outstanding, reaching 20 billion yuan, accounting for 64.5% of the total revenue, an increase of 23% year-on-year. WeChat's advertising revenue comes from a variety of sources, including RMB 10.2 billion in Moments advertising revenue, RMB 670 million in search advertising revenue, RMB 1.04 billion in public account advertising revenue, RMB 1.35 billion in mini-program advertising revenue, and RMB 6.8 billion in WeChat Channels advertising revenue.

In terms of growth rate, Moments grew by 3%, search grew by 68%, public accounts grew by 17.5%, mini-programs grew by 22%, and WeChat Channels led with a growth rate of 70%. WeChat Channels has entered the commercialisation stage in the second half of 2022, and it still has strong growth potential. Last year, the total revenue of WeChat Channels advertising was about RMB 25 billion, and it is expected to grow significantly this year.

The growth in advertising revenue over the past two years has been primarily driven by the development of WeChat Channels, which has seen growth in e-commerce, a slight increase in user engagement time, and a rise in the number of daily active users. Part of this advertising revenue is driven by ‘closed-loop e-commerce’, which refers to merchants opening WeChat Stores and promoting them through various WeChat Channels.

The increase in advertising revenue mainly comes from advertising forms that focus on sales results (including those on third-party platforms like Taobao), such as live broadcasts and WeChat Stores-related advertising. Live broadcast and WeChat Stores advertisers will become the primary driving force behind the growth of performance advertising, especially for well-known brands in the beauty and food sectors. In the short term, local services will not significantly contribute to the development of WeChat Channels advertising, as the relevant infrastructure has not yet been perfected.

The advertising ratio of WeChat Channels is now about 3-4%. This ratio is still lower than its competitors’; Douyin's advertising ratio exceeds 10% and Kuaishou's level is 12%-14%. Despite this, the number of daily active users and usage time of WeChat Channels continue to rise, increasing the advertising income.

In 2023, most merchants had not yet advertised on WeChat Channels, but by 2024, some small and medium-sized brands began to try to advertise on the platform. WeChat's annual advertising growth rate is expected to be 13.2%. Although lower than Douyin, WeChat Channels’ growth rate is expected to reach 50%, becoming a bright spot.

Another interesting trend is that the share of advertising on WeChat Channels among medium-sized merchants has gradually increased from zero to 5%, and then to 10%, and these ads are mainly used for private domain traffic and existing customer maintenance (see below). Meanwhile, medium-sized merchants are reducing their advertising expenditure on Douyin, mainly due to the difficulty in guaranteeing a return on investment. Similarly, on the Kuaishou platform, the proportion of advertising by medium-sized merchants is also decreasing. However, the proportion of advertising on Xiaohongshu among medium-sized merchants has increased, mainly for promoting seeding content.

Large merchants' advertising investment strategy on Douyin remains stable, their proportion of advertising expenditure on Xiaohongshu has increased, and the proportion of advertising on Kuaishou remains stable or slightly decreases. At the same time, the proportion of advertising on WeChat Channels is gradually growing and is expected to increase from 10% to 20%.

Public versus private traffic

Public traffic (or ‘paid traffic’) is traffic from sources that are visible to anybody on a platform, e.g. advertising. Private traffic (or ‘owned traffic’) refers to followers, e.g. those who have subscribed to an official account. WeChat has adopted a multi-pronged approach in balancing and integrating private and public traffic strategies. First, WeChat encourages brand merchants to utilise both private and public traffic. Merchants can obtain public traffic through various advertising tools provided by WeChat and convert this traffic into private traffic, for instance, by having the users follow their WeChat Channel or Official Account. At the same time, to maintain and develop private traffic, merchants can make full use of WeChat groups, live broadcasts, and short videos.

WeChat's system adjusts the allocation of public traffic based on the activity of merchants' private traffic. This mechanism is designed to encourage merchants to continually improve the quality and effectiveness of their private operations (e.g., content). This strategy not only helps brand merchants achieve better marketing results but also has a profound impact on merchants' operating methods and resource allocation.

E-commerce advertisers who advertise on WeChat Channels usually allocate 20% to 25% of their budget to private traffic, mainly used to guide users to e-commerce platforms through Moments or WeChat Channels.

Next week, in the third and final part of this series, we will explore the challenges WeChat has in making e-commerce successful and what the outlook for the future is.

Key Takeaways

WeChat's e-commerce strategy leverages its vast social network, aiming to create a unique social shopping environment and attract consumers who may not be interested in traditional e-commerce platforms.

The core e-commerce ecosystem is designed as a "three-in-one" system, where WeChat Stores handle transactions and after-sales, Mini Programs manage functional services, memberships, and marketing, and Service Accounts drive retention and repurchase.

WeChat Stores were relaunched in August 2024 as an upgrade from WeChat Channel Stores, serving as the primary transaction hub and allowing product information to circulate across various WeChat scenarios, including public accounts, WeChat Channels, mini-programs, and search.

Despite its relaunch, WeChat Stores currently hold a relatively low position in the Tencent ecosystem, accounting for less than 2% of total GMV, while mini-program e-commerce accounts for a substantial share, approaching RMB 2 trillion annually.

WeChat Channels is a critical traffic entrance and growth driver for the e-commerce ecosystem, having reached 600 million daily active users. It also significantly contributes to WeChat's advertising revenue growth.

WeChat Search presents a significant commercial opportunity with 600 million daily searches. It plans to integrate further with WeChat Channels and mini-programs to optimise information flow and improve conversion rates for merchants.

"WeChat Mall," which collectively refers to all WeChat e-commerce features, prioritises enhancing user stickiness and achieving steady development over rapid GMV growth, leveraging its social attributes as a core advantage.

Tencent employs an outsourcing model for managing WeChat Stores, with a focus on technology development. At the same time, external service providers assist small and medium-sized enterprises with private domain traffic management and operational support.

WeChat's advertising revenue, particularly driven by WeChat Channels, is experiencing strong growth, with medium-sized merchants increasingly shifting their advertising expenditure towards WeChat Channels for private domain traffic and customer maintenance.

Sources

This article has been compiled from an analysis of exclusive expert interviews within the Six Degrees Intelligence network, supplemented by insights from the articles listed below.

Images by Tech Buzz China’s Ed Sander, unless stated otherwise. These images may not be reproduced without Tech Buzz China's prior consent.

[1] Latepost 2024-12-03 [2] 36Kr 2025-01-23 [3] Tech in Asia 2014-05-29 [4] CKGSB 2014-08-26 [5] iResearch 2015-09-08 (now offline) [6] iResearch 2017-05-23 (now offline) [7] 36Kr 2024-12-19