Shein 2024 update – Part 1: global growth, logistics, assortment and product development

Original image phone: Shein. Original image world map: Yuri.

Contents

Things that caught our attention

Tech Buzz China’s Rui Ma was one of the experts sharing thoughts about the potential TikTok ban/forced sale in a panel conversation by ChinaFile. Other participants included Kevin Xu, Ivy Yang and Donald Clarke.

Introduction

It’s been a while since we last wrote about Shein in November 2022. So we thought it was high time for an update on the company's status, especially now that it is allegedly starting a road show for a London IPO.

As the company has expanded worldwide into new markets like the Middle East and Latin America, there are a lot of new insights to share. Moreover, Shein has also differentiated into various sales models that are worth exploring and comparing to those of its competitors. Finally, there is more information on the current profitability of the company.

We have decided to split this Shein update into two parts. In October, we will share all information on its global expansion into various regions, as well as insights into its approach to logistics and product development. In November, we will publish the second part, which looks into sales models, expectations and profitability.

Ed Sander, Research Editor

Markets

Shein's main markets include North America, Europe, the Middle East, Southeast Asia, Africa and Brazil, mainly selling fashion products such as bags, shoes and hats, household items, beauty products, toys, etc., especially those related to women and infants.

South American countries such as Brazil have doubled their sales in the past two years, while the growth rate of the European and American markets has dropped to about 50%.

Shein’s penetration in the US and Europe is about 50%, and in other regions it is more than 30%.

Globally, the number of registered users has exceeded 200 million.

In the US market, registered users reached 60 to 70 million.

The platform has about 8 million daily active users and about 27 million monthly active users. These figures are significantly higher than last year. Last year, Shein's daily active users fluctuated between 5 million and 7 million, while the monthly active users ranged from 23 million to 25 million.

The total transaction volume in 2023 was about 58 billion US dollars, and the goal for 2024 is to reach 75-80 billion US dollars.

In the first half of 2024, Shein's total transaction volume reached 30 billion US dollars, an increase of 50% over the same period last year.

Looking ahead, it is expected that the share of the US market will be 30%, the share of Europe may drop to 20%-25%, and with the growth expectation in the Middle East, it can reach 25%. Latin America is expected to account for a 10% share, and the rest will comprise Asia and other regions.

Shein has given the North American market the highest priority worldwide, and resource investment and growth expectations have also increased significantly. The company has relatively few competitors in the North American market. Although large companies such as Amazon have tried to enter the fashion field, Shein still has an advantage in scale through its self-operated and cross-border operation model. And although platforms such as TikTok have developed in North America, their overall scale is still not comparable to Shein.

In general, Shein has seen different performances in various regional markets; some markets are growing rapidly, while others are facing challenges. Overall, the company has maintained growth momentum in multiple regions.

In the Asian market, Japan and South Korea performed exceptionally well, with growth rates exceeding 110%. At the same time, the Brazilian market also performed well, with an annual growth rate of 35%. In the Oceania region, the Australian market has an annual growth rate of 40%, which is a considerable growth, although its share in the overall business is still low. The New Zealand market and the market in South Africa account for a smaller proportion of the overall business.

Shein does face various challenges and risks in different overseas markets. In the European and American markets, the company mainly encountered difficulties in product certification, taxation and intellectual property rights. In Latin America, the biggest challenge comes from policy instability. For example, Brazil's tax policies often change, which brings uncertainty to the company's operations.

Although populous countries such as India, Indonesia and Brazil have huge market potential, they also have high policy risks. Therefore, Shein's investment strategy in these markets is relatively cautious, and it needs to carefully weigh the market potential and policy risks and formulate targeted market strategies.

In the current complex global political and economic environment, Shein may adopt mergers and acquisitions or strategic cooperation to enter new markets in order to balance risks and opportunities. To survive in this environment, the company may cooperate with local groups with government backgrounds or close relationships, even if this may mean sacrificing some profits.

The company faces relatively low potential risks in the Middle East and Asia compared to the US market. The company has close ties with the Middle East and maintains good relations with local governments. In terms of the Asian market, although the company currently does not operate in Indonesia and India, it has lower risks in countries such as Thailand, Malaysia and the Philippines. These factors will affect the company's considerations when formulating its internationalization strategy.

Shein faces fierce competition from well-known cross-border e-commerce platforms in the global market. Shein's main competitors vary in different regions. For example, in Latin America, Meikeduo is Shein's main competitor; in the Southeast Asian market, Shopee is its biggest competitor. Turning to Europe, Amazon has become the main challenge Shein needs to deal with. In East Asia, especially in the Japanese and Korean markets, Shein has to compete with Rakuten and Coupang. Despite facing these domestic cross-border e-commerce giants, Shein has remained competitive, mainly due to its unique pricing strategy.

At the start of 2024, Shein expected that production capacity in countries such as Turkey, Brazil, and Mexico would increase to 30% or more of the global clothing production capacity. In Latin America, the growth rate of new users in Mexico, Brazil, Chile, and Argentina was very fast, while in the Middle East, Israel, Turkey, and Egypt ranked second.

Asia

Shein expects to double its GMV in Asia in 2024. Currently, the company has a 3% market share in Japan, about 1.5% in South Korea, and even less in Southeast Asia. Shein has ambitious plans to increase its market share in Japan and South Korea to 10-12% in the next three years.

Shein is also facing some challenges in the process of expansion. Compared with the European and American markets, the average customer price in the Southeast Asian market is low, which leads to a relatively high proportion of various costs, thereby compressing profit margins. This situation may have a certain impact on Shein's profitability in the region.

India

Shein is planning to return to the Indian market and expects the total transaction volume of products to reach $4 billion in the first year. Looking ahead, the company expects the GMV in the Indian market to grow to $8 - $10 billion next year. The Indian market undoubtedly has huge development potential, but it also faces challenges such as policy risks and joint venture requirements. India has taken protectionist measures to require foreign companies to cooperate with local companies, which makes it difficult to transfer funds abroad even if there are profits.

Although it is currently necessary to operate through a joint venture (with Reliance Retail), it will not significantly affect the profit margin due to the low traffic and logistics costs in India. However, given the high risks of setting up a production base in India, the company remains cautious.

If India relaxes restrictions, the company is expected to quickly restore its early user base. To seize the market opportunity, the company plans to cover mainly college students and young women. Although competitors are also entering the Indian market, the company still has a competitive advantage. Overall, despite the challenges, the company is positive about returning to the Indian market and has set clear strategic goals.

Middle East

Shein's order volume in the Middle East declined in 2023, possibly related to political situations and logistics issues. Although the region's share has dropped, the absolute value is still increasing, with the year-on-year growth rate remaining between 18% and 20%.

There are several key points to Shein’s performance in the Middle East market. First, Shein sets up pop-up stores to allow customers to try on clothes and then place orders through online channels in the store while providing coupons and holding events to attract customers.

As we know, Shein's advantages lie in its fast speed of new products, unique category design and competitive prices. The company's daily new products reach an average of 6,000 items, of which about 7% are for the Middle East market, meaning there are about 400 new products for this region daily.

Shein also offers a full range of products, sharply contrasting with competitor stores focusing only on a single category. In terms of product lines, Shein's Middle East product lines cover plus-size women's clothing, accessories, home furnishings, beauty and other fields. This caters well to the needs of Middle Eastern consumers because Middle Eastern consumers like to update jewellery frequently and have very high requirements for the quality of consumer goods.

Shein's poor sales performance in the Middle East may be related to various local conditions. First, Middle Eastern consumers, especially those in Dubai, are not particularly sensitive to prices and prefer to buy high-quality goods. Shein’s low-cost products are often of poor quality and prone to fading. In addition, during traditional festivals such as Ramadan, although demand will increase, there has not been explosive growth. Cultural differences and the existence of taboo styles also lead to supply difficulties. Sometimes products may need to be taken off the shelves soon after launch.

On a more positive note, the average customer price in the Middle East is about $4 to $5 higher than in the European and American markets. Specifically, the average order value in the Middle East market can reach $130, while in the US market, it is $75, and in the Latin American market, it is between $45 and $50. The net profit margin in the Middle East market may be higher than in other markets, usually between 5% and 10%.

As for marketing strategies, Shein mainly uses social media and cooperation with Internet celebrities to increase brand awareness in the Middle East. In addition, Shein adopts game strategies, issuing coupons and live broadcast interactions to attract new users and promote repurchases of old users.

The rest of this article, including an in-depth look at Shein’s developments in Latin America, its logistics, assortment, and product development, is available to paid subscribers only.

Latin America

Mexico and Brazil are the leading Latin American e-commerce markets. While the US market size is about 8 to 10 times that of Mexico, Mexico’s daily total merchandise transaction volume reaches $700,000 in the domestic market and $9 million in the international market. In contrast, Brazil's daily average transaction volume is higher, with domestic daily transactions between $3.7 million and $4.5 million and a ratio of domestic transactions to cross-border transactions of 1:3. Regarding growth rates, Mexico's target this year is 30%. In comparison, Brazil has set a target of 20%.

Shein has taken steps to adapt to the local market in Brazil. First, it adopted the OBM (original brand manufacturer) model. This strategic choice was mainly due to the 60-70% increase in Brazilian tariffs, plus a 17% turnover tax, which means that Shein must increase its selling price by 90% to achieve profitability.

In this Taobao-like model, Shein's platform is open to local suppliers, allowing them to sell products using their own brands and supply chains. In the traditional model, Shein would include domestic shipping, and Shein would determine the pricing. However, in the OBM model, pricing power is transferred to the supplier, who also manages the brand and logistics. In the previous model, Shein would pay the supplier the cost price and determine the selling price. The ODM model gives suppliers more autonomy and control and may bring higher profit margins.

Shein’s platform model has been very successful. Regarding finance, Shein's overall revenue in the Brazilian market in 2022 reached 8 billion reais, about 10.5 billion yuan. Compared with 2021, this revenue increased by 300%. Market forecasts show that the overall size of the Brazilian market has the potential to exceed 100 billion reais.

Meanwhile, the size of the Mexican market has surpassed Asia and is approaching the level of the Middle East market. Shein has also promoted this OBM model in Mexico. As a result, Shein’s merchants are mainly concentrated in Mexico and Brazil, numbering about 30,000. They expected this number to double in 2024.

The competitive landscape in Mexico and Brazil differs significantly. In Mexico, MercadoLibre holds 20% of the market share, while Amazon's share is about half of that. Walmart focuses mainly on its own business, while Coppel is similar to Walmart in its home country. Shein's market share is less than 10%. In addition, many small platforms in the Mexican market divide the remaining share.

In contrast, the situation in the Brazilian market is different. The market lacks leading cross-border e-commerce platforms. Amazon and Mercado Libre are the leading local platforms in Brazil, but their scale is relatively limited. Shein’s business scale in Brazil is about one-third of Shopee's. Temu has also launched in Brazil, while Kuaishou has entered the market on a smaller scale.

The e-commerce market in Latin America presents diversified characteristics. Take Brazil as an example; its clothing manufacturers pay more attention to the profit of each order than adopting a low-price strategy to win future orders. In contrast, although Mexico has a consumer electronics industry cluster, its prices are still much higher than those in the Pearl River Delta. Both Mexico and Brazil are not as flexible as China in terms of supply chain response speed and price adjustment.

In these two markets, significant differences also exist between local sellers and China's cross-border e-commerce platforms. Due to the lack of strong competition, local sellers in Mexico tend to set their own prices rather than participate in price wars. In Brazil, due to the existence of Shopee, price comparison control has become very strict, which can quickly reduce commodity prices. This makes it challenging to implement price control in the Mexican market, while Brazil has successfully reduced selling prices through strict price control measures and enhanced market competitiveness.

The market conditions in Mexico are similar to those in Brazil. The main reason consumers choose cross-border goods is that there is a lack of similar goods in the local market or the price is too high. These factors together shape the unique landscape of the Latin American e-commerce market, affecting the pricing strategies and market competitiveness of local and cross-border sellers.

The main challenge facing companies in the Latin American market is that consumers are extremely price-sensitive. This region has a clear rich-poor gap, and the middle and low-income groups account for a considerable proportion. Consumers pay close attention to prices when shopping. If the same product has different prices on different platforms, they will not hesitate to choose the platform with the lower price. Even if all platforms increase prices simultaneously, consumers will still tend to choose the platform with a slightly lower price to buy the same product.

Competition in the Latin American market is extremely fierce, especially in terms of price. When companies try to expand into multiple categories, the main challenges they face include insufficient supply chain control, lack of product uniqueness and scarcity, and weak price competitiveness. Take the clothing industry as an example. The key to success is to have strong supply chain control capabilities from the upstream and to respond quickly to market demand and launch new products. Fast fashion brands like Zara can quickly supply goods according to design requirements. In contrast, home appliances such as rice cookers can’t achieve such a quick response, so they face more significant challenges in market competition.

Shein vs Shopee

In Latin America, especially in the Brazilian market, the competition between Shopee and Shein is fierce. The two companies significantly overlap in terms of sellers, especially in the clothing industry. Shein is actively attracting local sellers from the Shopee platform, covering all categories, which has led many merchants to choose to operate on both platforms at the same time.

In Brazil, there is almost no difference in the quality and quantity of the goods on the two platforms. However, in Mexico, only Shein is currently conducting local-to-local business, so a direct comparison cannot be made. Shopee's cross-border e-commerce business in Brazil performs better than Shein's. Shopee has enriched its product variety using external cross-border platforms, and its sellers have a high overall operating level. This has also enabled Shopee to receive more positive reviews from customers.

Shein also faces some other challenges. Due to the limitation of logistics capabilities, Shein can only collect parcels in some cities and states, which makes it difficult to surpass Shopee in terms of the number of merchants. Nevertheless, judging from the goods displayed on the platform, the situation of the two companies is almost the same. This fierce competition undoubtedly provides more choices for local sellers while also bringing consumers a richer selection of goods and more competitive prices.

Shopee has begun to build its own logistics system in Brazil, adopting a platform logistics model. In this model, Shopee outsources some logistical links (such as first-end delivery) while operating the critical links by itself. Shopee's approach is to send packages from different states to the corresponding transit warehouses according to the destination, then merge the packages and deliver them uniformly to ensure the timeliness of delivery. In contrast, Shein adopts the method of waiting for all packages to arrive before shipping them together.

Although Shopee's model is more efficient, the cost also increases accordingly. Although Shein saves some costs, its delivery time is usually 1.5 to 2 times that of Shopee. Shopee can usually complete delivery within 2-3 days, while Shein takes longer. These two logistics strategies have their advantages and disadvantages. Although Shopee's method is more expensive, it can provide faster delivery services and may be more suitable for customers with higher timeliness requirements. Although Shein's strategy has a longer delivery time, it is cheaper and may be more suitable for price-sensitive customers.

However, globally, Shein has a significant competitive advantage in the global fashion market. Although Shopee has tried to get involved in similar business areas, the results have not met expectations. Today, Shopee has completely transformed its related businesses into a managed operation model. Shopee's full range of management services covers all kinds of goods. However, in terms of fashion, Shopee's performance has not yet shown significant results compared to Shein.

Tax policies

Mexico has imposed tariffs of about 20% on certain goods since mid-April this year. In mid-June, the Mexican government will discuss adjusting the tax exemption amount, which may be reduced to $20-30 or completely cancelled, and may impose value-added tax and tariffs, with a total tax rate of up to 40%. The purpose of these new policies is to increase the operating expenses of cross-border e-commerce, enhance the market competitiveness of local merchants, and increase government fiscal revenue. However, these policies may reduce consumers' enthusiasm for overseas shopping and hurt cross-border e-commerce platforms.

There are two possibilities for the timing of policy implementation: one is to implement it after the big sale in November, and the other is that the government is eager to implement it in advance. In either case, the conversion rate and sales of cross-border self-operated goods may decline in the short term. However, in the long run, fast fashion clothing will remain competitive because Latin America lacks a related industrial chain. Overall, these changes will have a profound impact on the development trajectory of cross-border players in the Latin American e-commerce market.

Meanwhile, in Brazil, the tax exemption policy for small personal purchases has been cancelled since the new government came to power at the beginning of 2023. The government requires platforms to assist in collecting cross-border taxes and to count the total amount of personal purchases. For goods worth more than $50, tariffs of 60% to 90% will be imposed, and personal information will be required for verification. As described, these policies have also promoted an increase in the proportion of business in the local market of Brazil through platforms such as Shein.

The new tax policy and compliance requirements will impact Shein's operations in the Latin American market, but the situation is not entirely pessimistic. Although tariffs will affect prices, Shein's unique style makes its loyal customers still choose to shop on the platform because it is difficult to find similar products in other channels. Under the new policy, the product advantages of new sellers remain unchanged, but the conversion rate may decline. Compliance requirements lead to higher operating costs for high-priced orders, affecting profits.

Specifically in the Brazilian market, the average customer unit price is $27 to $28, and the fulfilment cost accounts for 22% to 23% of the total cost. These fulfilment costs cover the entire transportation process and warehousing operations. In contrast, in Mexico, the average consumption amount per order is $25 to $26, while the fulfilment cost is between $4.5 and $4.6. Looking ahead, costs are expected to fall, especially after the scale effect emerges. Delivery costs can be effectively reduced by merging orders and other means. For example, after expanding business in Mexico, the fulfilment cost per order may drop to about $4. These changes will undoubtedly affect Shein's market competitiveness and future development strategy, but the company seems confident that it can cope with these challenges by optimizing operations.

Localisation

Multinational e-commerce companies such as Shein have significant advantages in the Latin American market. Although local clothing manufacturers understand local market demand, they face challenges in product update speed and price competitiveness, and it is difficult to compete with international e-commerce companies. Multinational e-commerce companies such as Shein are adopting a fast-response small-batch production model and plan to cooperate with Brazilian suppliers to further enhance their competitiveness.

However, the clothing supply chain in Latin America is relatively inefficient, and it takes time to adapt to this new model, and the effect has not yet been fully seen. In the long run, fast fashion brands will continue to maintain a significant advantage in Latin America, mainly because some problems in the local supply chain are difficult to solve quickly. Although such goods are regarded as fashion products and sales may fluctuate in the short term, they are expected to pick up in the future. The long-term impact of this market structure on the Latin American clothing industry may prompt local manufacturers to continuously improve efficiency and innovation capabilities to compete internationally.

Logistics

e-Commerce cargo now occupies 60-70% of air freight capacity, while traditional trade accounts for 30-40%. Shien’s business is one of the drivers of this development.

Currently, Shein has multiple warehouses in China, mainly concentrated in Guangdong Province, located in logistics industrial parks in cities and managed by leasing. Shein's domestic logistics centres cover Foshan, Zhaoqing, Jiangmen, Nanshan District, Qingyuan and Huadu. In addition, there is also a warehouse in Yiwu, Zhejiang. Among these locations, Foshan and Zhaoqing are core distribution centres. Looking ahead, it is expected that Shein's warehousing network in China will continue to maintain its existing layout, mainly distributed in the Pearl River Delta region and cities near Guangzhou, especially Zhaoqing and Foshan, close to Guangzhou Airport.

Regarding cross-border e-commerce logistics, Pinduoduo and Shein have adopted some innovative strategies to reduce costs and improve efficiency. Usually, couriers pick up items at customers' locations and then deliver the goods to the service for processing. However, Pinduoduo and Shein have set up pre-processing in their warehouses. This approach allows them to handle large quantities of goods more efficiently. Since Temu and Shein's goods are usually low-priced, around $30, it is costly and uneconomical to use high-end logistics services such as DHL to transport single items. Therefore, these platforms usually combine many small packages into one large package.

To ensure the timeliness of transportation, Temu and Shein usually work directly with airlines to charter flights to transport large quantities of goods and then entrust local express companies to complete the last leg of delivery. However, this operating model is difficult for Temu and Shein to manage because they cannot integrate professional logistics resources. In contrast, local professional logistics companies are able to provide comprehensive management services, from signing contracts with airlines to docking with overseas suppliers to last-mile delivery to ensure seamless connection and efficient operation of the entire process.

Staff at a DHL sorting centre in The Netherlands unpack boxes with multiple individual packages from a Chinese cross-border e-commerce platform. Labels and faces are blurred for privacy reasons at the request of DHL.

Shein's short, flat, fast and flexible supply chain is very strong, but its most significant disadvantage is that it has no warehouses overseas. Shein has always wanted to change this but never had the opportunity to change it in the early stages. The cycle of Shein's products is seven days. Few customers will send goods to overseas warehouses in 7 days. The cost of going back and forth is too high.

But now, the international environment has changed greatly. It used to be easy to do cross-border business, but now all regions have begun to do so-called localization. The first shot came from Indonesia. E-commerce in TikTok was banned, and Bytedance had to acquire Tokopedia to be able to sell in the country. Brazil, which has high import tariffs, and the United States, where consumers expect fast delivery and where import tariffs are looming, also require cross-border giants to do localization.

With the aforementioned local IDM platforms, Brazil and Mexico now require the establishment of overseas warehouses. The contractor is still Jitu, but Jitu's terminal transportation capacity is limited because Pinduoduo, Jitu 's strategic investor, operates Shein’s competing platform Temu. Temu required Jitu to put aside all difficulties and invest as soon as possible in Mexico and Brazil, which affected Jitu's cooperation with Shein abroad.

Cross-border e-commerce platforms usually adopt a variety of strategies when choosing logistics partners. Currently, these platforms generally use freight forwarders to find suitable transportation service providers. Initially, they mainly cooperated with domestic freight forwarders in China. However, as their business developed, some multinational e-commerce companies began establishing partnerships with logistics companies through intermediaries or directly.

E-commerce companies of different types and sizes have different considerations and choices when choosing cooperation models. For example, some cross-border shopping platforms tend to find transportation services or carriers through freight forwarders, while others choose to sign contracts directly with transportation service providers. In general, cross-border e-commerce platforms have adopted diversified cooperation strategies according to their respective situations and needs. This diversified approach enables them to better adapt to the needs of different markets and business models.

In the current cross-border e-commerce logistics environment, due to shrinking profit margins and intensified market competition, some platforms have begun to bypass the logistics middlemen and negotiate directly with aviation and shipping giants. Shein is no exception. However, although Shein’s freight volume is huge, the high cost of chartering flights cannot fully meet the needs of all routes. For routes with less freight volume, such as South American countries such as Brazil, Chile and Mexico, Shein prefers to cooperate with large freight forwarders. Through this collaborative approach, Shein can reduce its expenses on customs clearance and terminal distribution abroad.

Some large e-commerce companies usually do not rent the entire aircraft but cooperate through the palletization method. In some specific express services, such as China's B2C e-commerce products, it may be necessary to rely on the four major express companies. Some e-commerce companies do not have a fully developed overseas logistics network and may need to cooperate with major express delivery companies or suppliers with international delivery capabilities.

When choosing partners, Pinduoduo (Temu) and Shein first focus on cost, followed by the coverage of the international delivery network. About 60-70% of the goods still need to be handled by freight forwarders because the e-commerce companies are mainly platform operators and do not operate both platform and logistics businesses like Amazon and JD.com. On stable routes, Shein may cooperate with airlines to charter entire aircrafts. The choice and adjustment of this strategy mainly depend on the characteristics of different markets and routes, as well as the scale and needs of the e-commerce platform itself.

The business scale of cross-border e-commerce giants such as Pinduoduo and Shein is astonishing. It is estimated that about 60-70% of the transportation business of these e-commerce platforms is handled by freight forwarders, and the remaining 30-40% is directly in cooperation with logistics companies. E-commerce platforms like Shein must rely on large freight forwarders to meet their vast logistics needs. Different platform payment methods will affect the proportion of whether they cooperate directly with carriers or transit through freight forwarders.

These e-commerce platforms will constantly adjust their strategies according to their conditions and select the most suitable freight forwarding companies. Especially for platforms with large business volumes like Shein, it is necessary to optimize logistics costs because international logistics costs are high and have a significant impact on overall operational efficiency.

Freight forwarders' operations are extremely dependent on cash flow, and insufficient capital turnover may lead to operational difficulties. Due to Shein's excellent payment cycle performance, American express delivery companies regard it as an important customer and provide it with priority services. Logistics companies prioritize meeting Shein’s freight space needs.

An analysis in April pointed out that large platforms usually sign contracts directly with carriers, and it is estimated that 70-80% of their business does not go through freight forwarders. However, this view is different from what is currently observed by industry experts, which may be due to differences in payment habits or observation angles of different platforms. This difference reflects the complexity of the relationship between payment cycles and logistics priorities in the e-commerce industry and their impact on platforms of different sizes.

With the rapid development of the e-commerce industry, payment schedules have had a significant impact on the market share of each platform. Large e-commerce companies like Amazon have their own logistics systems, and companies like Shein may face the same challenges if they expand to a similar scale. Currently, the industry is undergoing changes, and Amazon has parted ways with traditional express delivery companies. If Shein builds its own logistics network, its suppliers may encounter a similar situation. However, since Shein is not as large as Amazon, it currently does not take the risk of building its own logistics system.

With the expansion of e-commerce, many logistics companies have established warehousing facilities abroad and provided storage services to enhance customer experience. Temu and Shein have adopted a semi-managed model in the United States (see our May article), with merchants shipping their products to local overseas warehouses and completing the last leg of delivery after they are sold. Abroad, logistics companies may form delivery teams or cooperate with local large companies such as the US Postal Service and truck companies to complete the last mile of delivery tasks. To meet customer needs, it has become crucial to provide additional services, and the simple port-to-port transportation method will gradually be eliminated.

In comparison, Shein’s delivery speed is faster than TikTok’s. Shein's fully managed delivery (shipped from China) takes 7 to 9 working days, while semi-managed delivery (shipped from local warehouses) takes 3 to 5 working days. TikTok's delivery speed is one day slower than Shein’s. This delay is mainly because many orders on TikTok require notification of brands before they can be shipped for delivery, and individual sellers do not attach much importance to timeliness and user experience. Shein's delivery time in China still has room for improvement.

However, if the speed is fast, it may lead to an increase in the return rate. This is because faster delivery speed will shorten the backlog time of orders, but it may cause more users to return goods, thereby increasing logistics costs and affecting profits. This difference in delivery speed may have a significant impact on both companies. Faster delivery speeds may increase customer satisfaction and loyalty, but at the same time, it may also increase operating costs and return rates. Conversely, slower delivery speeds may affect user experience but may reduce return rates and related costs. Therefore, both companies need to balance speed, cost and customer satisfaction.

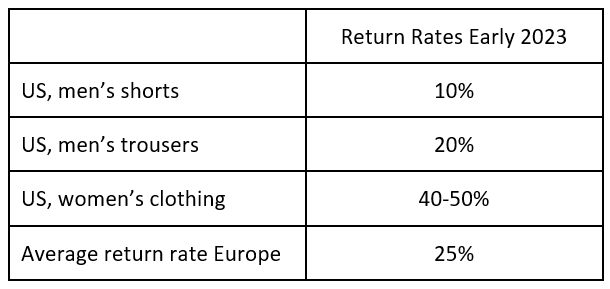

Shein return rates

Products

When exploring Shein's performance in the global fast fashion market, we can see that the brand has a significant market share in different regions. Taking the US market as an example, Shein's fast fashion retail market share is close to 20%. In the Brazilian market, Shein's market share is as high as about 30%, and in the UK market, it remains between 12% and 13%. However, when we look at non-fast fashion areas, Shein's sales share or influence in these corresponding regions appears relatively low. This may mean that the brand's main focus and advantages are still on fast fashion products.

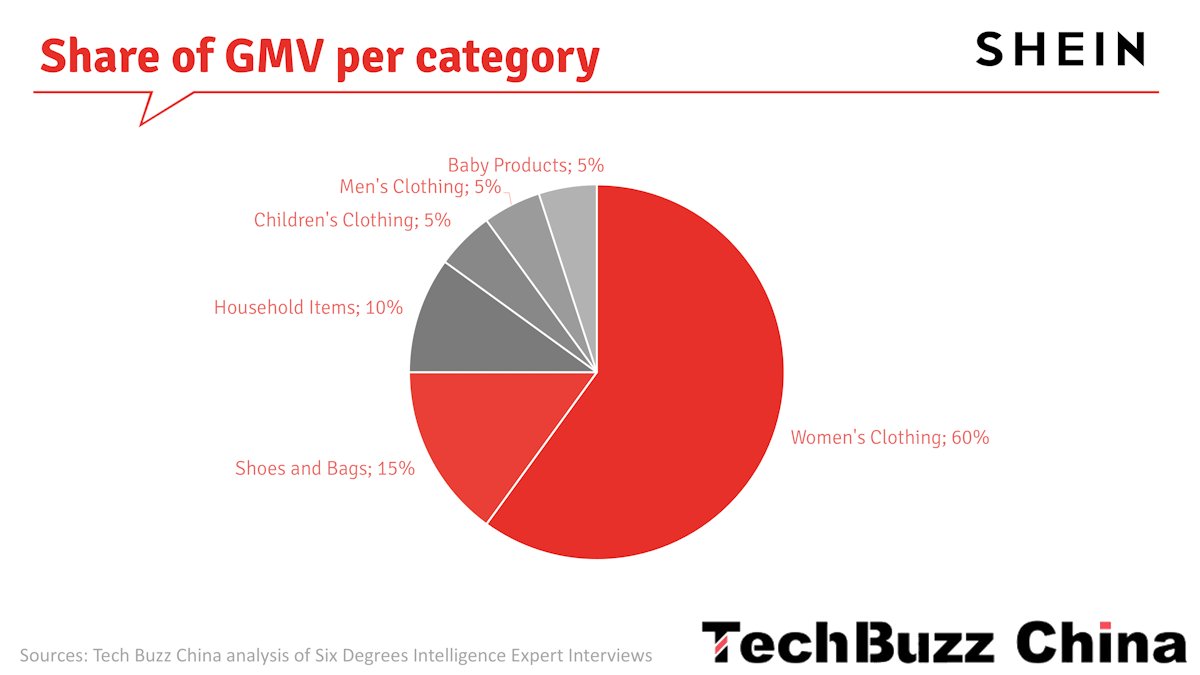

With the opening up to the outside world and the introduction of third-party brands, Shein has also begun to supply household items, daily necessities and outdoor equipment. Apparel products still dominate 80% to 82% of Shein's total sales, while the rest covers diversified products such as baby products, beauty products and household products. Specifically, baby products account for between 3% and 5%, household products account for nearly 10%, and the rest is made up of handicrafts and sewing supplies.

In Shein's merchandise sales structure, the GMV of total apparel products accounts for about 70%, mainly from the sales of its private brands. As for sales in 2023, the GMV of women's clothing products accounts for about 60% of Shein’s total sales. The sales GMV of children's and men's clothing both account for about 5%. Although these figures are relatively small, they show Shein's market presence in these categories. In general, Shein's performance in the fast fashion field is strong, while other areas need further development and expansion.

The sales of shoes and bags accounted for about 15% of the total sales, of which more than 70% of the goods were self-produced. In addition, Shein's other categories include daily necessities, tools, consumer electronics, small appliances, and pet supplies. Looking at 2024 and 2025, Shein plans to expand its product lines of footwear and small household items.

Specific data of small categories such as beauty, pet and children's products are difficult to quantify accurately. As an emerging category, the growth rate of small household appliances (such as electric kettles, hair dryers, etc.) is significant. The unit price range of these products is between $15 and $45, mainly targeting female consumer groups, and Shein experiences a current market demand that is very strong.

Although Shein's product range has touched many aspects of clothing, food, and home decoration, it mainly focuses on small commodities. It has not yet involved large commodities such as transportation, office equipment or large furniture. In many product categories, such as shoes and bags, accessories and cosmetics, Shein mainly uses products from third-party suppliers, although it has also launched its own brands. In these categories, the proportion of Shein's own brands is not high. Shein once tried to launch 8 independent high-end brands, but these brands did not perform as expected, with annual sales of only tens of millions of yuan.

For example, Shein has launched a shoe brand called CUCCOO, but most of its shoe products are still produced by external suppliers, which may be unbranded or branded products of suppliers. A similar pattern is also seen in the cosmetics field. Although Shein has its own brand, most of its products are still supplied by third parties.

Faced with this development bottleneck, Shein is actively expanding its product range and business model. In its new attempts in the baby and household products markets, Shein has demonstrated significant price competitiveness with China's robust supply chain system. In addition, Shein has a vast user base of between 100 million and 200 million. The potential purchasing power of these existing users in other consumption scenarios is undoubtedly a significant trend for Shein to expand into new markets.

There are also limitations. In the clothing industry, Shein has a unique advantage in that it can quickly process small-batch orders, which is difficult for other cross-border or local e-commerce companies to achieve. However, when expanding new product categories, Shein faces a significant challenge, which is changing the perception of European and American consumers that it is mainly a clothing brand. In response to this challenge, Shein has adopted a strategy of attracting consumers through price advantages and improved delivery efficiency. However, the effectiveness of these strategies is not significant. It may take some time for consumers to gradually accept Shein's image as a comprehensive platform.

Suppliers

For the manufacturing of its own products, Shein currently does not have its own factory but chooses to entrust all production work to external suppliers, more than 4,000 production factories, using a variety of cooperation methods such as FOB (Free on Board), OEM (Original Equipment Manufacturer) and ODM (Original Design Manufacturer). Shein does not hold shares in any supplier's factory but maintains a procurement cooperation relationship with them.

In the early stages, Shein may provide certain financial support to the factories, such as subsidies or loans. Still, as the supply chain system matures, this practice is no longer necessary. If a factory wants to become a partner of Shein, it must first apply and attach the necessary documents. After review and approval, it will enter a three-month trial cooperation phase, during which the factory will be assigned some small-scale orders that need to be completed quickly.

Shein adopts an operating model similar to Didi Chuxing, where orders are directly allocated to factories by the company headquarters, avoiding competition for orders between factories. When allocating orders, Shein will consider factors such as the factory's production capacity, product quality, cooperative attitude, and response speed and prioritise factories with strong production capacity, fast feedback, and good cooperative attitude. Suppliers cannot actively compete for orders, and Shein completely controls the allocation of orders.

After the initial cooperation phase, only companies that meet specific assessment standards can be promoted to formal suppliers; companies that do not meet the standards will be eliminated. Once a formal supplier, the company will be rated based on multiple indicators such as its production capacity, product quality, delivery time, and ability to handle urgent orders. It will be given an S, A, B, C, or D grade. In the supplier classification, grade A represents the top supplier, while grade B is the ordinary supplier. Many of the C- and D-tier suppliers are likely to be eliminated or replaced.

Among the 4,000 suppliers, S-level and A-level suppliers account for about 15%, and B-level suppliers account for slightly more than 35%. Usually, Shein decides to eliminate and replace about 30% of C-level and D-level suppliers based on specific circumstances. Core suppliers of B-level and above are Shein's primary source of production capacity. In contrast, C-level and D-level suppliers provide flexibility and help shorten delivery time when demand surges.

As Shein's sales performance continues to climb, its entire clothing production chain has expanded accordingly. Shein tends to enhance the production capacity of existing high-quality suppliers rather than adding a large number of new suppliers. This is because it usually takes a long time to adapt to establishing a partnership with a new supplier, and small-scale factories often cannot maintain consistency in production quality.

Shein needs its top suppliers (such as A-level) to double their production capacity within a year to cope with the growing order volume. This may lead to a decline in the profit margin of individual products. Still, due to the increased number of orders and the continuity of cooperation, these suppliers have become more critical in Shein's clothing supply chain.

Even S- and A-level suppliers usually cannot conduct effective price negotiations when faced with Shein's huge order volume. Shein's pricing department will review the cost of each order and ensure that suppliers of grade A and above can obtain a net profit of 8-12%, while the net profit of grade B suppliers is set at 6-10%. As for grade C and D suppliers, their profit margins are even smaller, and sometimes they can barely break even.

Big Data Analysis

A former Marketing Director of Shein shed some light on how the company uses big data, a topic on which many myths have been told.

Shein collects information about fashion through a complete set of information technology systems, including automated programs such as web crawler technology to continuously collect data in designated markets and countries. This information is systematically classified and sorted, for example, by country, category, and popularity. The sorted data is then handed over to the designers of the commodity centre, who carry out innovative design work and complete the production of design drafts based on the product line or category they are responsible for.

In addition to operating its own brand and the direct participation of designers, Shein has also implemented a buyer system. In this model, buyers go directly to physical markets and stalls based on their experience, select ready-made products from suitable suppliers, and assign factories or trading companies to produce them, which avoids using front-end data analysis and design processes. In Shein's operating model, the direct sales method of independent designers accounts for a large proportion, while the buyer model is relatively small.

Shein's online platform enables information collection around the clock, and this automated approach is significantly more efficient than traditional manual offline collection methods, such as those used by Zara. Although Zara may also use online systems, it mainly relies on its mature offline business processes. If Zara plans to expand its e-commerce business, it will take a long time to transition. When deciding whether to focus on online or offline, a choice needs to be made. In contrast, Zara's investment and attention to online platforms are not as high as Shein's, and it also lags behind Shein in data collection and its use.

Compared with the limited offline information sources, online technology can automatically collect a large amount of data. This gives Shein more abundant resources than ZARA in obtaining product categories and detailed information.

Product development

A former Marketing Director of Shein shared more insights about Shein’s product development.

Shein's design process usually takes only three days from start to review, significantly shorter than the corresponding cycle of ZARA. Although Shein and ZARA have similar designer teams, both with hundreds of designers, Shein provides its designers with more comprehensive materials. This allows them to focus on making minor modifications and mild innovations, which is similar to assembly line operations and, therefore, has higher work efficiency.

In contrast, ZARA's designers must undertake more combined creative tasks, which not only requires higher skills from designers but also increases the workload, resulting in relatively low efficiency. In Shein's small order and fast return model, the pass rate of product testing is not fixed but will be adjusted according to the collected market information and the efficiency of the design. This rate usually fluctuates between 50% and 70%. It is important to ensure the quality of new products, and products that do not meet the standards are not allowed to be listed.

Over time, Shein's data processing system and model have undergone continuous operation and progress, which has gradually improved the accuracy and efficiency of each operation link. Therefore, the success rate of new product launches each year has also shown an upward trend, although there is no clear quantitative standard for the specific value of this increase.

When the success rate or popularity of a new product decreases over a certain period, this usually indicates that there is a problem in the data collection or acquisition process. Therefore, specific data, values or acquisition channels need to be adjusted. At the same time, designers are responsible for making necessary adjustments to the product's intellectual property rights while maintaining the core characteristics of the product.

Usually, to ensure the consistency of the production process, a specific product will be manufactured by a specific factory. When the production capacity of this factory reaches its limit, it may consider transferring some orders to other factories with the same level and producing similar products. In addition, when suppliers belong to the same category and are of the same level, their manufacturing technology and product quality are often similar because the design and production process of such products is usually relatively simple.

There is a lack of service providers in the market that specialize in selecting product directions. There are currently two main methods of selecting products: one is to develop a system to collect data independently, like Shein; the other is to use third-party ERP tools to analyse store sales data of specific categories. Apart from these approaches, few other approaches have produced models that are commercially valuable or can be widely replicated.

Next month, in the second part of this Shein update, we will investigate Shein’s various sales models, market strategies and current profitability.

Sources

This article and part 2 have been compiled from an analysis of around 15 expert interviews of the Six Degrees Intelligence network.