11/11 Tech Buzz China Insider Digest

View this email in your browser

Insider Digest 11/11/21: Muted Single’s Day Is a Strategic Shift for Alibaba, The China ClimateTech Opportunity, Some Chinese “Metaverse” Startups, Is There Decoupling in Chinese VC?

Housekeeping / Announcements:

The biggest announcement is that we’re going to launch our first deal soon for the Tech Buzz China Investment Syndicate. That’s right, due to our unique position in the nexus of startups that have China connections or are inspired by China tech, we have some access to allocations in private companies, and will be opening up our first deal to accredited investors in the next month or two. Insider subscribers will get first dibs, of course. We’ll be holding information sessions soon, and I’m here to answer all your questions. But if you’re interested, please fill out this form.

Whew, we’re almost at the end of the year! We have more Insider Events every week for the next few weeks! Please sign up via the Calendly links below (where confirmed) so that you get the reminder email and calendar invite:

[TOMORROW! Insider Sharing] 11/12, 11AM PST / 2PM EST: Zak Dychtwald, TBC Insider & Founder of Young China Group & author on Understanding Chinese Gen Z, and we’ll probably go over 11/11 as it pertains to Gen Z too!

[External Expert] Thurs. 11/18 5PM PST / 8PM EST / Next day 8AM Asia time: Greg Pilarowski on Chinese gaming industry & regulations

[External Expert] TBD: Richard Turrin on the Chinese Central Bank Digital Currency

If you are interested in sharing what you’re working on with the community, provided that it’s about China tech / investing, please do reach out!

Here are our articles for the week!

11/11/21 Muted Single's Day is a Strategic Shift for Alibaba

Throughout the day, rumors kept on leaking that the GMV for many of the top brands were in fact drastically below last year's record shattering $75Bn haul, or that the max bandwidth being used by the major banks is a fraction of last year's peak. But then, a bit past midnight, Alibaba and JD both announced "record" Single's Day GMVs for the year:

Alibaba: 540.3 Bn RMB or ~$84.5Bn USD, +8.5%

JD: 349.1 Bn RMB or $54.6Bn USD, +28.6%

As meaningless as GMV metrics are, especially around the ultra-engineered Single's Day, it's still an important data point. And to put things into perspective, not only were some analysts (Citi) expecting a +15% for BABA this year, but the entire market was forecasted to grow 11% by eMarketer. So ... it's not really some amazing result.

Here's what I think it all means:

This muted Single's Day represents, in my mind, a major strategic shift on behalf of Alibaba. Single's Day is played out and going further down this road erodes its competitiveness and destroys both customer and merchant relationships. It needs to find a less exploitative way to grow, or to embark on an entirely new path altogether.

Why do I say Single's Day is exploitative? Well, most English accounts don't capture it, but there has been an increasing number of complaints from merchants around Single's Day in recent years, because of the amount of promotional discounts that they must give in order to satisfy their Alibaba overlords. OK, well, not exactly overlords, but there is immense pressure to go all in on 11.11 promotions, and many of the smaller merchants lose rather than make money. And don't forget, prior to this year, they had no choice but to participate due to Alibaba's egregious 2-choose-1 tactics. And by the way, if they did, the platforms would often force them to give "lowest prices on the internet" guarantees. Here's a comic from 21st Century Business that draws this out.

But even louder than merchant complaints are customer complaints. Multiple state media have written this year that consumers need to have "Math Olympiad" skills in order to figure out how to get the best deals (in Chinese). The platforms are at fault here for their complicated promotions. But also at fault are merchants, who are increasing prices in the weeks before the event in order to show a drastic discount (in Chinese). The practice is so prevalent that the government came out last week and issued warnings to consumers to watch out for these tactics, and to ban them (official policy from SAMR here).

So if I had to summarize, many of the "deep discounts" that were powering Single's Day GMV growth were either the result of the platform exploiting merchants or the users, or the merchants exploiting the users. Sure, the platforms were largely unscathed, but this is clearly some kind of unsustainable. The TMall VP Guang Yang put it rather delicately this morning when asked why there was no real-time scoreboard of the GMV as in years past, it was because in their longer-term strategy, the user experience of merchants and consumers have become more important. Implicitly acknowledging that it wasn't as much of a priority before?

11/11/21 China's Climate Tech Opportunity

Since it is the COP26 Summit this week, I figured it would be fun to dig up Sequoia China's excellent report released earlier this year on climate tech that explains why they are planning to go all in on the sector. The sector is already flaming hot, and if we count CATL (battery maker) and the many EV companies as part of the space, then it is actually already quite big. But here are some more reasons for you to be excited:

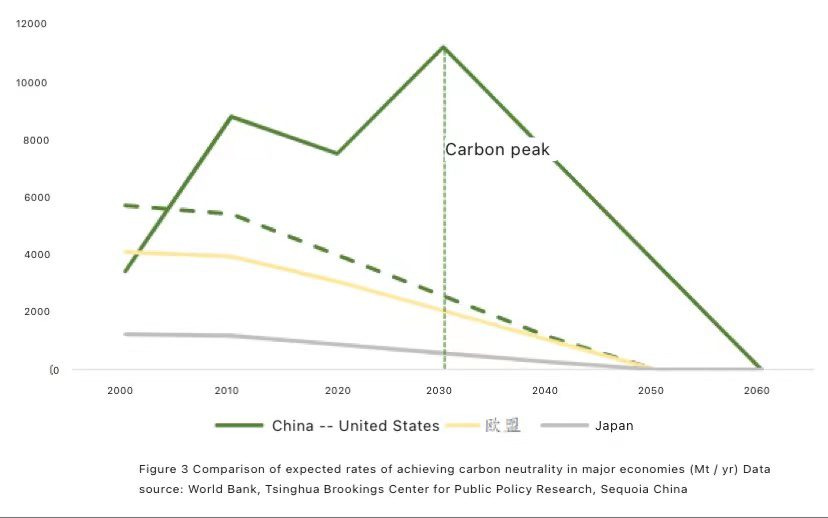

China has agreed to peak carbon emissions in 2030, with zero net emissions by 2060 (Europe & US plan to do so by 2050).

US peaked in 2005, and Europe in 1979, meaning that they will have had 45 and 71 years respectively to reach zero net emissions. China, however, has yet to peak, and will only have 30 years. The dropoff will have to be extremely steep, and thus, an immense opportunity. Carbon emissions in mm tons (yellow is Europe)

11/10/21 Some Chinese "Metaverse" Startups

You can kind of put anything into the Metaverse bucket these days, but are there any that are actually getting interesting traction? I spent a few days on this just to make sure I'm not really missing out on anything big and so far ... I don't think so. Here are some examples of the most oft-mentioned names and the categories I think they represent. The ones that could be of interest and worth following are the top 3 (with screenshots).

VR

Oasis - Yeah, it is actually called Oasis (like the game from Ready Player One), and it's exactly what you think it is. A VR world. Steam link here. The PC version (VR) seems to have been offline, and the mobile version (not VR) was at one point ranked higher than Facebook's family of apps in Brazil earlier this year. Est. 2018 and launched in 2019. Probably one of the best known companies in China in this space.

Platform

Minovate - As far as I can tell, basically a Roblox / Minecraft. Founded in 2015, near 1000 employees, with a DAU of 2mm+ (as of April 2021, pre-regulations). It's obviously had to comply with the minor video game restrictions. I imagine it's not in a great place right now, but don't have specifics to share.

Metaverse Builder?

Yahaha - A "metaverse maker" whose founding team comes from Unity. No-code real time UGC metaverse builder. Lead investors are Coatue, ZhenFund, 5Y, Bilibili, Xiaomi, Hillhouse, BAI. (Was Tencent conflicted out? Probably?) They raised 3 rounds in just a few months. This is clearly targeting a global market. This is supposed to be a screenshot of their current progress. One competitor is Manticore, which is funded by SoftBank, Benchmark, Epic Games et al. and has raised $160mm.

11/10/21 Is There Decoupling in Chinese VC?

If I had to generalize, then I would probably say that prior to 2014, there was almost no RMB investment in early stage venture capital in China, and while it ballooned in the last few years, these funds generally invested in different sectors from their USD counterparts, and also gave different terms (which may account for their different sectors).

First, the terms. The terms for RMB funds as of the beginning of this year is still typically less than 8 years in length (compared to the US standard of 10). 5 or 7 years is more common, but as short as that is, it's still better than the standard 3 year term that was prevalent just five years ago. That's just because there are fundamental differences in the investor base of LPs (limited partners) who put money into these funds:

In general, USD LPs are long term investors, and will commit over multiple cycles, meaning that fundraising cycles are short once they're already in. But RMB LPs are two types, and do not have streamlined deployment processes:

If government funds, then it's largely coming from the budgets, and the goals of investment are generally to boost local employment, draw in more investment into the local economy, and also increasing tax revenues of course. For funds coming from financial institutions, then it is all about the returns.

To give you a sense of the disparity, mature markets may have 50% of private equity (including venture capital) funds contributed by long term investors (such as endowments, pensions, etc.) But in China, that number is just 5% as of 2019 (in Chinese). Click through for more ….

Have any comments or questions? See you on the Discord server!

Copyright (C) *|CURRENT_YEAR|* *|LIST:COMPANY|*. All rights reserved.

*|IFNOT:ARCHIVE_PAGE|**|LIST:DESCRIPTION|**|END:IF|*

*|IFNOT:ARCHIVE_PAGE|**|HTML:LIST_ADDRESS_HTML|**|END:IF|*

Update Preferences | Unsubscribe

*|IF:REWARDS|* *|HTML:REWARDS|* *|END:IF|*