6/5/22: The Changing Influencer Economy in China & Meituan Update

View this email in your browser

Insider Digest 6/5/22: The Changing Influencer Economy in China & Meituan Update

Housekeeping / Announcements / Fun:

As announced before, your Tech Buzz China memberships have been paused while I am on maternity leave. That means you will not be charged from 6/3/22 (last Friday) to 9/4/22 at minimum! The Circle forums and Discord community will remain open, so no need to do anything there. I will also remain active on Twitter and reachable via email. All that’s really happening is you’re not being charged for the next three months, yay! The investment syndicate will also still be running, so check for new deals there! I may still jump in from time to time with an email blast though!

What You Missed on TBC Discord:

I guess today is a good indication how bad sentiment is. Those BABA numbers were awful. Negative GMV growth in marketplaces (while JD grew ~20%!?!). True operating income (stock comp is a real expense) adjusted for the Ant shares write-back shenanigans was cut in half. Stock up 15% - w048cxh

I think the market cheered the fact that the cmr trend, which grew slightly, wasn’t commensurate with the decline in gmv. It’s a reversal from the narrowing spread trend and predicts better relative profitability. Wrt april guidance, I think the street has low teens decline in gmv next qtr so the cake is already baked in the stock price. If we saw cmr continue it’s decline at a rate faster than gmv, the reaction would have been disasterous. But looks like stabilization in ad rev. - maskedinvestor

MS note on JD might make you feel better. Thanks maskedinvestor!

Mizuho summary on China stimulus. Also maskedinvestor.

Shanghai is returning to normal

- Meituan coffee takeout +210% from last week ☕️

- Eleme small shops takeout 40% back online, some categories 50%+

- Parcel deliveries back to 80-90% of normal, Cainiao said yesterday was already back to prelockdown level for them

Mega Taobao livestream ecommerce influencer Austin Li Jiaqi currently not streaming because his team member brought out a “tank-shaped dessert” on 6/4. Image here. I find it hard to imagine it’s anything other than commercial sabotage, but others in the Discord disagree, what are your thoughts? Either way, could be bad for Taobao’s already declining clout in livestreaming ecommerce, and also for 618, though that’s already fairly muted this year.

Other Links:

I only noticed this myself, but People’s Daily wrote back in March that Amazon’s marketplace is a “chokehold technology.” It advocates for Chinese merchants to do more of their own shopping sites. As I’ve said before, that has been a particularly hot area of investment in China recently and we’re looking into it at the TBC Syndicate.

China’s Supreme Court wants to integrate blockchain into the judicial system. As mentioned before, China wants blockchain, but not crypto. And it’s especially eager to adopt blockchain into government.

6/2/22: Update on Douyin, Kuaishou and the Livestream E-commerce Economy

Some data on the latest two short video giants Douyin and Kuaishou, and their divergence, as evident from their ad mix and livestream mix, which I think are related.

(Random: TheInformation had an article out today provocatively titled “Why China’s influencers are losing their influence,” but less data than I cite below.)

As of March 2022, all data from QuestMobile, as quoted in this TF Securities report:

Kuaishou (both the main app and the Express version, including duplicate users) reached 607mm MAU, -1.1% YoY

Main app: 210mm DAU, -8.2% YoY, 108 mins / day (+13.7% YoY)

Express: 126mm DAU, +26.3% YoY, 106 mins / day (+18.8% YoY)

DAU / MAU ratio ~55%

Douyin (both the main app and the Express version, including duplicate users) reached 880mm MAU, +22.7% YoY

Main app: 418mm DAU, +25.5% YoY, 109 mins / day (+12.2% YoY)

Express: 209mm DAU, +46.6%, 99 mins / day (+9.8% YoY)

DAU / MAU ratio ~71%

For those of you who don’t remember, the Express versions of these apps are view-only, cannot be posted to, have smaller download sizes for simpler phones, and most importantly, often offer some kind of hongbao / cash reward for activities in app. Kuaishou pioneered this (although one can argue Qutoutiao did it at scale fist), and Douyin quickly followed suit. Obviously, this model explicitly encourages time spent. I’d put this feature on the “potentially endangered” list given China’s anti-addiction stance.

While the mins / day data are all up YoY, it’s largely down or flat QoQ, so we may have started to hit a ceiling in terms of time spent. Which is just as well, because 109 mins could be considered to be encroaching upon serious addiction territory, and again, I don’t know that that’s compatible with the government’s clearly stated policy direction.

Per App Growing, for March 2022, the ads served on Douyin is ~7x larger than Kuaishou though, representing a growth of 150%, versus Kuaishou’s was actually -7.8% YoY. Just a year ago, the difference was only 3x.

As you’d expect, a lot of the increase in advertising for Douyin is related to its ramped up e-commerce efforts, as we can see from this comparison of Kuaishou vs. Douyin advertisers below:

Kuaishou: Gaming 27%, Entertainment 21%, Ecommerce 10%, Dating 8% and Other 5% in March 2022. A year earlier, Gaming was also #1 at 26% and Entertainment at 19%.

Given the unfavorable policies for gaming, it is actually very surprising that it continued to retain such a strong presence on Kuaishou.

Douyin: Ecommerce 11%, Cosmetics 9%, Clothing 8%, Entertainment 8% and Gaming 7%. Versus a year earlier, Gaming was 30%, Entertainment 16%.

Douyin has clearly shifted its advertising mix to be much more diversified, and focused on e-commerce as the top sector. This is consistent with what the leaked notes from ByteDance showed, and also reflected in our ByteDance model.

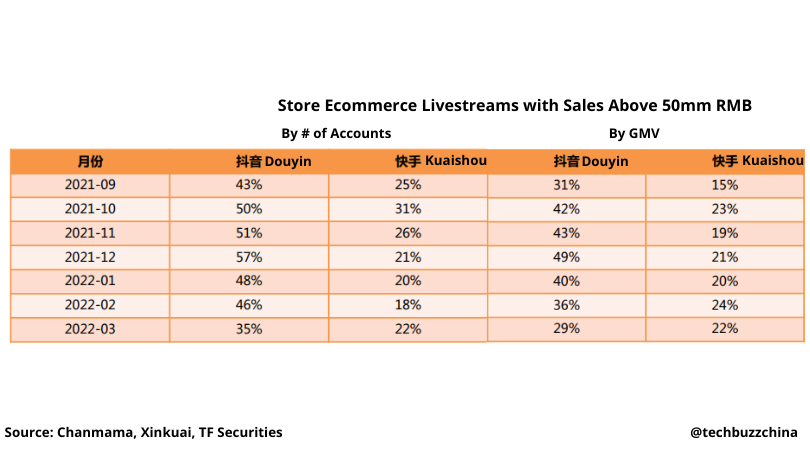

GMV: Spotlight on “store livestreams” versus influencer / KOL livestreams:

There are three types of ecommerce livestreams in China currently — by influencer, by brand, and by store. Most times, the last two are combined into one category as “by store,” but when they are separately broken out, generally, brand livestreams are operated by the brand (although often through operating partners), whereas store livestreams are typically operated by well, a store, which can feature multiple brands. In either case, they are more similar to each other and very distinct from KOL livestreams, which have dominated the conversation due to the wild success of folks like Viya and Austin, but are actually declining in relative importance, as stores figure out that they want to own their own fans (but of course!).

For Douyin, the top 1000 livestreamers have declined from 70%+ from KOLs to now just 49% KOLs and 27% brand livestreams and 25% store livestreams.

By a different analysis, for livestreams with sales above 50mm RMB, Douyin has about 1/3 to 1/2 of GMV from top accounts from store livestreams, whereas Kuaishou is 1/6 to 1/4. Again, this isn’t anything we didn’t know already … remember, Kuaishou has chosen to cozy up to creators more than brands. Its Xinba family of creators still account for 4-6% of total GMV on the platform, whereas no one in Douyin has remotely close to that kind of share.

Let’s talk about operating partners for a second. Basically, these are companies that do all the ecommerce operations for the brands. Almost everyone, for example, uses TPs, or Taobao partners, to operate on Alibaba, and in fact Alibaba comes out with a list every year ranking their top operating partners and has strict rules for verified partners. It is this ecosystem, by the way, that allows Alibaba to operate at scale efficiently. Nowadays, the fastest growing operators at DPs, or Douyin Partners, which take care of all your Douyin operations. It’s one of the pieces Douyin has been growing aggressively ever since it decided to focus on ecommerce — the Alibaba playbook is a good one to emulate.

By the way, brands are being quite smart about who they work with. Many will work with different partners and have different flagship stores for specific product categories, in a sort of “racehorse” scenario where they are trying to figure out who will end up being the best collaborator.

But in other ways ByteDance is doing the opposite of Alibaba. BigOne, for example, told me that there’s not really a meaningful contribution from store livestreams on the Taobao platform due to Alibaba’s boosting of KOLs such as Austin in the last few years. Of course they’d like to diversify, but no one’s really willing to change direction too much at this moment, not when there’s so much pressure on the company.

The important thing to remember about KOL livestreams is that the way many brands think about them is as a combo marketing + sales channel. Recall that there is usually a minimum fee just to be featured, often “lowest price on the internet” guarantees to be made, and of course a 20%+ cut to the influencer for sales made. The costs are significantly more manageable, of course, for a brand’s own streams, which are more directly sales driven. So it makes intuitive sense that on a less KOL-dominated platform like Douyin, brands would be spending more to promote their own IP versus riding on the IP of a powerful livestreamer. It’s a different part of the marketing funnel.

Finally, Douyin has done a lot to make the platform more equitable for smaller players, unlike Alibaba who is known for driving traffic to the top KOLs. The share of GMV from Top 1000 livestreamers has declined from 40% in July 2021 to 26% in March 2022. Based on anecdotal evidence, this is why more and more folks are choosing to get started on Douyin / abandoning Taobao livestreaming. It’s simply not possible to compete with a platform who was built around individual starpower.

It’s tempting to say Douyin is growing while Kuaishou has stagnated, but that may be overly dramatic. The sense I got from talking to data providers such as BigOne is that the industry has changed so much in the last year that everything is in flux and very dynamic. Nonetheless, it is clear that Douyin has become the first place player, and its focus on integrating ecommerce into its content platform is paying off. Kuaishou, on the other hand, does not seem to be effectively integrating all of its assets — advertising is heavily gaming and content (digital instead of physical products from brands), and KOLs still dominate compared to Douyin, true to its “private traffic” roots. Versus Douyin who has built a bigger brand livestreaming ecosystem, and are having success getting many of them to advertise on the platform in a “closed loop.” I assume this will be the same playbook TikTok uses as it grows overseas.

None of this is surprising, but it makes me re-evaluate the overly simplistic and content focused narrative I had for Kuaishou, and appreciate more the holistic approach here that seems to be Douyin’s strategy. For reference, see below the many pieces I’ve written on Kuaishou, which now I think perhaps gave the platform more credit than it’s due:

1/18/21: Kuaishou IPO: Too Much Power in Hands of Creators?

2/9/21: Kuaishou 1H 2020 Content Report vs. Douyin 2020 Report

2/16/21: Are Bilibili and Kuaishou Very Comparable?

4/29/21 Kuaishou Creator Conference Overview

8/9/21 Kuaishou's Woes

12/2/21 Is Kuaishou a Victim of Narrative?

6/5/22: LatePost on Meituan: Paranoid or Prepared?

This LatePost update on Meituan one of the most widely read articles in my WeChat friends circle in recent months (you can see how many of your friends read an Official Account post that you subscribe to, and this was in the hundreds for me), and I thought it was interesting enough to share. (In addition, I know that the team has an especially close relationship with Wang Xing, so their Meituan coverage is extremely strong … but fairly balanced too, in spite of the closeness.)

Wang Xing is in the habit of asking provocative questions of his team. In 2H of 2021, he told his team to prepare for “3 years without any new capital infusion.” In March 2022, he went even further and asked executives to prepare a survival plan for where Meituan has zero revenues for the next three years. It isn’t a realistic scenario, but people think it shows where his headspace is at … that the next few years will be very lean indeed.

But a few things have been in Meituan’s way:

COVID, for one. Meituan had internally decided to make Shanghai the shining example of its ridehailing business, giving it the highest subsidies (20% vs at most 12% in other cities), resulting in the city contributing 20-30% of its total self-operated orders. But obviously the lockdown decimated all business. Going forward, it’s possible Meituan goes even more all-in on Shanghai because the city has effectively been “reset,” but that would also be extremely risky, again due to the unpredictability of COVID.

In-store GMV has also been hit hard, due to COVID. In March, Shanghai F&B dropped by 60-70%, in April, GTV was just ~60% of expected. The only way forward is to go deep into rural China, into 5th tier cities and beyond, where revenues per user are 1/3 of the first tier cities. (I’m still astounded the Shanghai numbers reported by everyone has been 60-70% declines instead of 99% ~~)

Thus Meituan has been lowering targets across the board:

Shangou (AKA Instashopping), it’s 30-minute delivery service, had 60 to 70Bn RMB in GTV last year, with a goal of +70% to 110Bn RMB this year. That’s been adjusted downwards 10%.

It’s shut down CGB (AKA Meituan Select) in 4 provinces already, Gansu, Qinghai, Ningxia and Xinjiang (some of the poorest in China).

CGB hit 120 Bn RMB in GMV last year, far from the 150 Bn target. Employees expect continued losses for the next 5-10 years.

Kualv, its B2B Meicai / Sysco-like service I’ve written about before, has shut down in 6cities, and Maicai (AKA Meituan Grocery), its 30 minute grocery delivery service, is similarly cutting estimates and subsidies.

Nonetheless, the company is marching towards its 100 million food delivery orders a day goal. In Q4 2021, the average number was 42.5mm. The goal is to reach 60mm by end of 2022, an increase of 40%+. (That’s still a good ways to go, but that’s what BHAGs are, I suppose!)

One of the experiments has been Pinhaofan, which lets you group-buy from the same restaurant as other friends for a low cost. (Ele.me tried to copy the same model, but gave up fairly quickly.) While it saves the rider some time on the pick-up side, it doesn’t all need to go to the same delivery address so there are still significant costs involved on the delivery side. I’m not a fan of this business …

Another experiment is corporate food delivery, which is still in its infancy.

Food delivery subsidies will be slashed 0.3% from last year. This corresponds to savings of 2Bn RMB or so.

Meituan is in full cost cutting mode:

From the small things: business trips need higher level approvals than before, and flights must be at least 30% discounted, and no flights from 11am-4pm. No more allowances for weekend or holiday trips.

To bigger, like how all hiring has been frozen since March:

Most layoffs have been at mid to low level, main platform cut 7%, bikesharing has been less affected (due to naturally higher attrition), most other departments 10-20%.

The goal is to be just like Amazon:

Junior and frontline workers don’t need to work overtime for the most part, but executives do. The two most important mechanisms they want to clone are the a) Operating Plan (twice-annual planning process) and b) S-team (senior team) goals. They’ve also adopted Amazon’s WBR / MBR / QBR (Weekly / Monthly / Quarterly Business Reviews) as well as Amazon’s meeting flow and principles.

The belief is that Meituan’s business is much like Amazon’s core business — low margin and operationally heavy.

The focus is now on obsessing over “controllable inputs.”

And … Wang Xing assured everyone (at least as of March 2022), he won’t be retiring any time soon. He’s determined to see Meituan through to its 100mm (food delivery) orders a day scale in 2025, and Shangou / Instashopping (the 30-minute delivery service) to 400 Bn RMB scale in 2026 (it’s at maybe 1/4 of that right now). Beyond that, the goal is to have 100mm people use Meituan’s groupons every day for F&B.

No real comments here, just observing Meituan and its struggles. Do you agree with the insistence on CGB even though profitability could be 5-10 years away and its core business and new initiatives such as Instashopping are mostly geared towards 1st-3rd tier city dwellers? That seems slightly schizophrenic to me. Is Amazon the right operational model to copy? That does seem to be a better argument. What do you think?

Have any comments or questions? See you on the Discord server!

Copyright (C) *|CURRENT_YEAR|* *|LIST:COMPANY|*. All rights reserved.

*|IFNOT:ARCHIVE_PAGE|**|LIST:DESCRIPTION|**|END:IF|*

*|IFNOT:ARCHIVE_PAGE|**|HTML:LIST_ADDRESS_HTML|**|END:IF|*

Update Preferences | Unsubscribe

*|IF:REWARDS|* *|HTML:REWARDS|* *|END:IF|*