5/23/22: 2022 Q1 Chinese VC/PE Update & Overseas Investments Summary

View this email in your browser

Insider Digest 5/23/22: 2022 Q1 Chinese VC/PE Update & Overseas Investments Summary

Housekeeping / Announcements / Fun:

As announced before, we will be pausing your Tech Buzz China memberships while I am on maternity leave. That means you will not be charged from next Friday 6/3/22 to 9/4/22. The Circle forums and Discord community will remain open, so no need to do anything there.

What You Missed on TBC Discord:

I spoke with some folks who were helping their bosses prepare for this meeting and was told that it was originally meant to be a forum for the companies to share their current situation, but was (mis)reported in the (Western) media as a policy meeting. From the attendees (~100, composed of many medium sized cos) I think it is pretty clear that it was not meant to announce any policy, although they did reiterate economic stabilization as a priority, etc.

Entity lists have been increasing in scope and this seems like it would be very problematic to enforce

Many Insiders think this kind of capital control is counterproductive for America. What do you think?

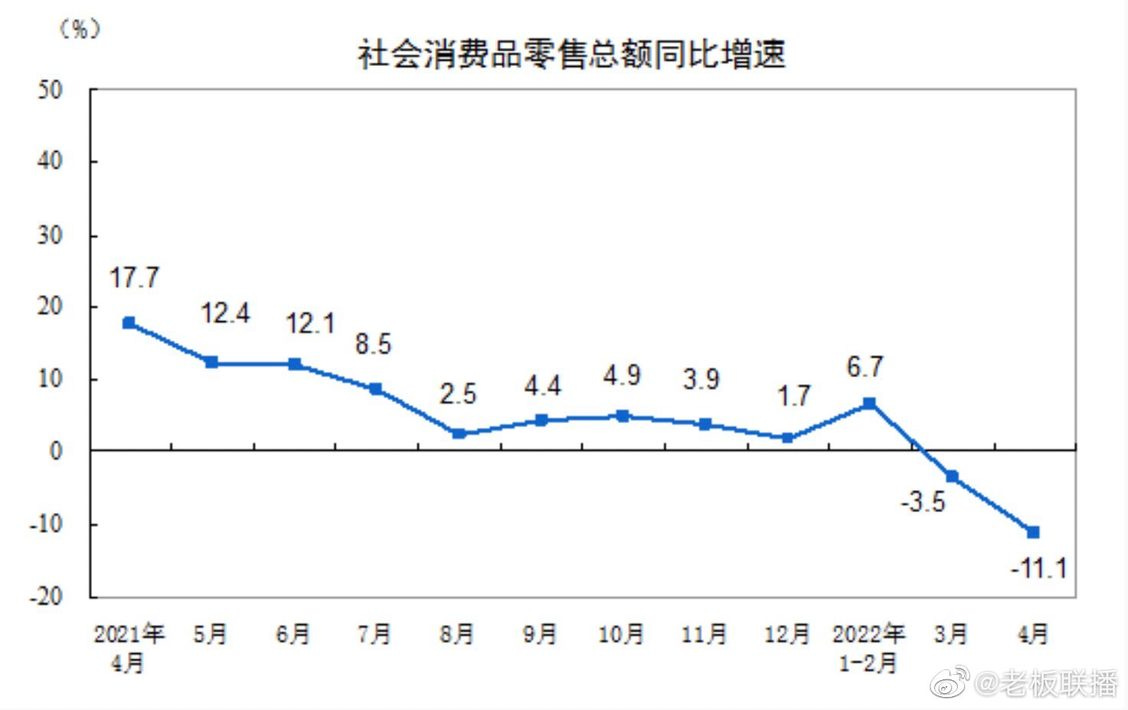

China consumer spending is down 11% in April YoY, Retail down 9.7%, F&B down 22.7%

It looked real enough, but the fact that another screenshot also supposedly from him came out to debunk it seems to suggest that there is a lot of validity to his points — the anti-capitalist crowd in China does seem to be a little out of control

Some interesting links that were shared:

China should move reserves out of US Treasuries, an oped based on speeches from a former PBoC official. Not by any means a mainstream opinion yet, but might perhaps get more attention after what US did to Russian assets. Could be big …

Didi passes delisting resolution

“like the Greenhill analyst said, if they dont delist, they will be stuck in a purgatory”

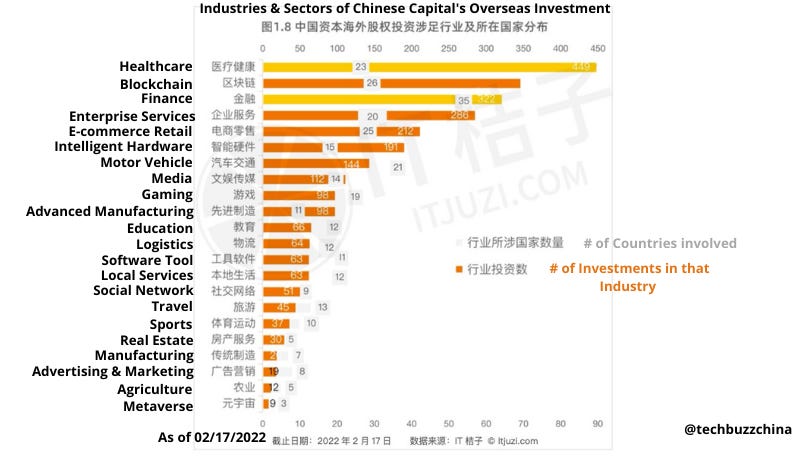

5/17/22 Chinese Tech Investments Overseas (As of Feb 2022)

This post is just a translation of ITJuzi's latest data on Chinese investments overseas. So far, it does not look like US-China tensions have done much to dent the enthusiasm of Chinese capital going abroad. However, I am concerned that things may turn for the worse at least for Chinese investment in the US in the near term as both COVID and geopolitical tensions continue to mount unabated.

First though, 2021 overseas investment actually matched the heights achieved in 2018, I think largely because last year was just an incredibly good year for private investing, period. It is unlikely we see those same numbers repeated for 2022.

Second, the US took the majority of investment dollars, with India a distant second, followed by Singapore in third place. Anecdotally, India is extremely tough for Chinese capital today, and can be basically considered to be entirely cut off. (These numbers encompass the last decade-plus, and do not reflect changes over time, so given the relatively few years China was active in India, you can see how quickly that ramped up ...). The US is much more lax in comparison, but again, things are in flux and can change at any time. We can see though, that Latin America / Australia / Africa don't even really register on this chart, and Europe is pretty small as well.

This bar chart easily shows how far the US outstrips other countries by deal count.

Similarly, USD accounts for about 90% of the investments.

Over half (56%) of the number of investments are in early stage (seed B). Note this is by deal number and not $ deployed.

Finally, the sectors of overseas investment differ somewhat from domestic hotspots. Healthcare is #1, but blockchain and fintech are #2 and #3 when they barely register domestically. Domestically, the three big sectors tend to be healthcare, enterprise and advanced manufacturing, but enterprise falls to #4 and manufacturing to #10 here, due to differences in ecosystem opportunities. Of course, this bar chart is tabulated by number of deals rather than dollars deployed, so that could account for some discrepancies, but this chart does diverge from the domestic landscape which I've written about here.

5/17/22 China VC/PE Q1 2022 Update

This report is from Zero2IPO, and is attached at the bottom of this post in full. We've taken some of the most important points and translated them here for you.

First, here is a summary of the government's stance towards venture capital over the last two years. As you can see, it's been fairly consistently focused on two things: the capital markets and manufacturing. And unlike the regulation-focused year of 2021, 2022 is much more growth focused. This is the same as every other policy statement from the central government with regards to tech in the last few years.

2022: Promote the development of venture capital; fully implement the stock issuance registration system; Enhance the core competency of manufacturing industry, digital economy, and carbon neutrality sectors

2021: Improve the venture capital supervision system; Steadily advance the registration system reform (for capital markets); Optimize and stabilize industrial and supply chains, and carbon neutrality as well

2020: Develop venture capital and equity investment; Pilot registration system (for domestic innovation stock listing boards); Promote manufacturing upgrade and the development of emerging industries

Second, on 2/18/22 a coalition of 12 ministries issued a document on what they think out to be goals for stable growth of the industrial economy. They are, to no one's surprise, mostly focused on infrastructure, advanced manufacturing, and climate tech.

Provide investment margin for infrastructure e.g. satellite navigation, 5G, and internet data centers;

Promote investment in advanced manufacturing and engineering;

Energy reform: Clean and efficient use of coal; New energy consumption; Wind, solar energy;

For Q1 2022, China early stage investment / VC / PE decreased significantly in all metrics while the US gained in everything except number of exits.

Funds raised:¥4,092.70 B -3.2% YoY

Number of investments: 2,155 -27.5% YoY

Investment Amount: ¥1,968.22 bln -47.1% YoY

Number of exits: 731, -31.7% YoY

However, fund registrations continue to increase. Across all types of funds, Q1 2022 saw new fund registrations of 2293, and increase of 26.3% YoY.

Early stage investment fundraising in China was poor. Funds are getting smaller (possibly sign of inability to hit fundraising targets).

Funds raised: 41.9Bn RMB, -20.1% YoY

New funds: 31, +3.3%

Per fund average: 135mm RMB, -25.3%

For VC (excluding early stage), the stats were nearly identical:

Funds raised: 88.9Bn RMB, -20.4%

New funds: 345, +8.8%

Per fund average: 263mm RMB, -25.6%

If we break it down by currency though, we see a big divergence. Across early stage / VC and PE, RMB funds raised over 370Bn, which is actually +11.6% YoY. But foreign currency (primarily USD) funds raised only 300Bn RMB equivalent, -62.6% YoY.

Where are the RMB funds coming from? Unsurprisingly, much of it involves state capital, as shown below. State capital GPs generally oversee state capital, and it can be from both governments and SOEs, and so that's why they're being used as a proxy for state capital involvement. Even for the smaller funds, state capital GPs account for 42%, which personally surprised me. Unfortunately I do not have a backwards looking to see how the makeup has changed over time, and so cannot say if state involvement is trending upwards or downwards.

What we can see is that the breakdown by sector is largely consistent with what I've shared in the past. Because the sources used are different, this categorization is somewhat different as well. (Previously I cited mostly ITJuzi data.) The top 3 sectors take up ~80% of the funds deployed as well as number of deals, and they are, in order: semis, healthcare, and manufacturing.

But what does the YoY change look like? I'll pick the top 3 sectors + IT + internet for comparison.

Here are the YoY changes for $ invested in early / VC / PE respectively:

Semis: +7% / +21% / -29%

Healthcare: -28% / -40% / -56%

Manufacturing: +75% / +21% / -65%

IT: -5% / -29% / -46%

Internet: - 66% / -88% / -93%

Pretty brutal. As you can see, even healthcare suffered a big decline, although I'd argue that was because of the exuberant excess of last year. Internet though, is probably reflective of a real shift in investment theses across the board. The other two sectors I didn't single out but which did well YoY were automotive and cleantech. Again, no surprises there.

Conclusion: Private investment in China is showing signs of strain, and will likely continue to do so for the rest of the year, at least. (It's mirroring what's happening in the US at the moment.) The few bright spots are "hard tech," such as semis and manufacturing, and RMB investments remain decent ... for now. But because RMB seems to be so heavily reliant on state capital, it's really hard to say what happens if the economy continues to tank. Is this capital here to stay? Or will it need to be re-directed to other, more urgent needs?

I do want to note that while Zero2IPO is one of the earliest organizations to track China VC/PE, I tend to like ITJuzi's product much better, because they sell not just summary data but the underlying detailed database. So don't take this to be gospel, merely a directional indicator.

Have any comments or questions? See you on the Discord server!

Copyright (C) *|CURRENT_YEAR|* *|LIST:COMPANY|*. All rights reserved.

*|IFNOT:ARCHIVE_PAGE|**|LIST:DESCRIPTION|**|END:IF|*

*|IFNOT:ARCHIVE_PAGE|**|HTML:LIST_ADDRESS_HTML|**|END:IF|*

Update Preferences | Unsubscribe

*|IF:REWARDS|* *|HTML:REWARDS|* *|END:IF|*