4/18/22 The Next Step for Chinese Games?

4/18/22 The Next Step for Chinese Games?

View this email in your browser

Insider Digest 4/18/22: The Next Step for Chinese Games?

Housekeeping / Announcements / Fun:

You’ll notice that last week, no newsletter was sent out and there were no posts, even though I was on the Discord as much as I could be. Unfortunately, I fell ill with severe anemia and an infection. Still recovering at the moment, but it is also a good time to let you know that I will be taking maternity leave beginning June 15, and will be putting your subscription on pause at that time. We’ll play by ear how it goes, but I plan to keep open the Discord server and try to be active there, but you will not be charged for anything while I am on leave (3-4 months). We may have some guest posts here and there, but I will be pausing payment for that time period.

The newest TBC Syndicate deal with Huashan Capital is having our Zoom AMA with the founder this Friday at 7AM PST. Do definitely join us if you are interested in the deal!

What You Missed on the TBCI Discord

We should expect an announcement in the next few weeks (timing unsure) on the rectification progress of the 13 +1 platforms that met with the regulators last April. The ones that "pass" will be allowed to return to "normal" and conduct capital market transactions. The ones that don't pass will need to continue the rectification process and will be restricted.

Is Alibaba really losing market share because of crackdown?

Article is a fear combo of 1) last year's cyber security security mishap public cloud, 2) state cloud push, 3) slowing growth (not mutually exclusive), and 4) competitive market share grab (from Huawei ~doubled in 2021). Although the article is right in saying the TAM that Zhang stated earlier is probably a pipe dream, it also states the potential opportunity that cloud can still grow >2.5X in 4 years... Baba doesnt need to maintain its marketshare for it to be a significant part of it its SOP - similar dynamic to its ecommerce.

But how’s Huawei gaining market share?

See conversation here that is too long to summarize on sale of their x86 server business last year, how much they rely on server chips for their cloud business, public vs. private, and how much their chips have progressed (Kunpeng was an ARM v8 chip)

Sohu seeks delisting from NASDAQ

They are the only HFCAA affected company thus far to delist. Although notably, they have already privatized two subsidiaries, Changyou and Sogou

Continued discussion of PCAOB delisting worries …

Join us on Discord to discuss … this seems to be a largely geopolitical problem at this point

Most of us think Didi is an exception and should be treated as such

4/18/22 The Next Step for Chinese Games?

The below summary comes from synthesizing a handful of industry research reports on the Chinese gaming industry that I found to be interesting / helpful, as well as some thoughts I’ve gathered over time.

What Happened?

Well, after 263 days / 8 months of freezing the game approval process in China, the engine suddenly spluttered to life again and 45 domestic titles were granted permission to operate in China. (Interestingly, the long pause in 2018 was 265 days.) Of these, 40 were mobile, 4 were PC, and 1 was a Switch title. Notably, neither of the two industry juggernauts, NetEase or Tencent, received any approvals. No need to worry about them though. They have healthy balance sheets and large backlogs of titles, unlike smaller studios who often are working on just a few projects at a time. Apparently, 22,000 of these smaller companies went out of business during this 8 month freeze. Was it all attributable to the freeze? Probably not, but maybe they could have survived longer had spring come sooner.

The Govt and Gaming Will Always Have a Love-Hate Relationship

Here I’m really summarizing a lot of the points from our livecast with Greg Pilarowski, the former General Counsel at Shanda, and a veteran in China gaming.

Firstly, the emphasis is on remembering that gaming is just yet another type of internet content that the Party is looking to regulate. The rise of PC games in China starting in 2000 especially made it obvious that gaming = internet content. A big reason why foreign companies cannot operate them without domestic partners. Anyway, games have been regulated as such since then and we should expect it to be regulated as such going forward.

Secondly, while it’s unclear how exactly the censors and their consultants play through each game, which could get quite lengthy ... the entirety of the game is indeed submitted and videos and text extracts separately tendered for easy review. And while the junior staff could be very knowledgeable and indeed excited about gaming, it doesn’t seem as if the senior decisionmakers care. In any case, they are not measured by their gaming knowledge, but by their adherence to the country’s overall content framework, so I don’t think it really matters their individual affinity for gaming, though it couldn’t hurt to have advocates on board.

Thirdly, after the reorg in 2018 which saw a similar pause in game approvals, there was a significant drop (of 85%?!) versus the year before. The argument put forth and commonly accepted has been that the government wants more “high quality games” to be made. It kind of makes sense. “Quality” is a consistent complaint that the government has about content and tech development in China. In the case of the former, the judgment of what is “quality” is largely cultural and moralistic / political, but in the case of the latter, there is a real push for technical advancement. For gaming, both imperatives exist, and indeed, we can see from the newest list of approved games that they aren’t your brainless Candy Crush types but actually quite complex titles. But the censorship aspect will always take precedence, and it wouldn’t be wise to forget that. Either way though, we may see a drop just like the one post-2018 going forward. From 2018 to 2021, the number of games approved were 2064, 1507, and 1405. 2021 had just 768 due to it being a half year of approvals. But if we take the 45 approved this month ... that is 54% less than the average monthly approval (98) in the first half of 2021, immediately before the freeze. Ouch.

Opportunity 1: PC Games

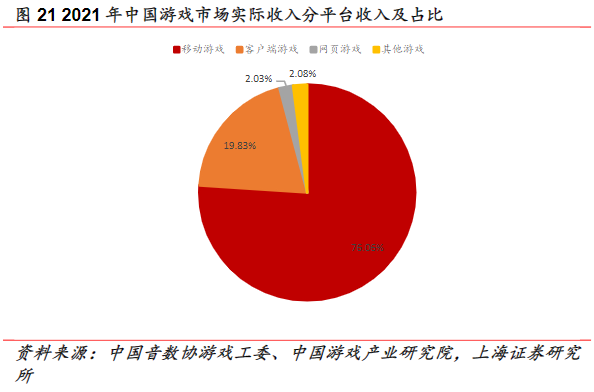

First off, there may be an opportunity in developing PC games. Chinese games development can be roughly divided into 2000-2007, when PC gaming was dominant, to 2008-now, when mobile gaming took over. 2015 was when increasingly hardcore (or at least midcore) mobile games began to seriously displace PC gaming development efforts, so that by 2021, you have 76% of gaming revenues domestically coming from mobile games (red), and just 19% from PC games (orange). (The remaining is composed of 2% from webpage games (gray) and 2% from other (yellow).) Basically, mobile game development still costs less than PC, with greater ROI. In fact, many mobile games got a huge boost from effectively being ports from popular PC gaming IP and gameplay. Chinese PC gaming development is also lacking compared to foreign capabilities. But ultimately, there are still a good number of PC gamers looking for new content — and the last major release was Netease’s Justice Online ... back in 2018.

Just how many players? Well, Steam, for example, estimates that Chinese players on international servers numbered 30mm MAU in 2018, and may reach 40-60mm by 2021 year end. That is a substantial number of the 120mm MAU in total on Steam in 2020. It’s entirely possible that the companies who choose to meet the unmet demand of PC gaming — and perhaps this extends to VR gaming when it does become mainstream — will be able to take advantage of this next “blue ocean opportunity.”

There is a risk here though. If we were to just look at the titles approved this month, it does seem that they veer towards the “lighter,” less hardcore gaming side of things. It could be that this is how the government wants to make sure its anti-addiction stance also succeeds. Not to say that all PC games are necessarily more immersive and hardcore than mobile games, but it is often the case. So I personally think this is a far less attractive opportunity than ...

Opportunity 2: Overseas Gaming

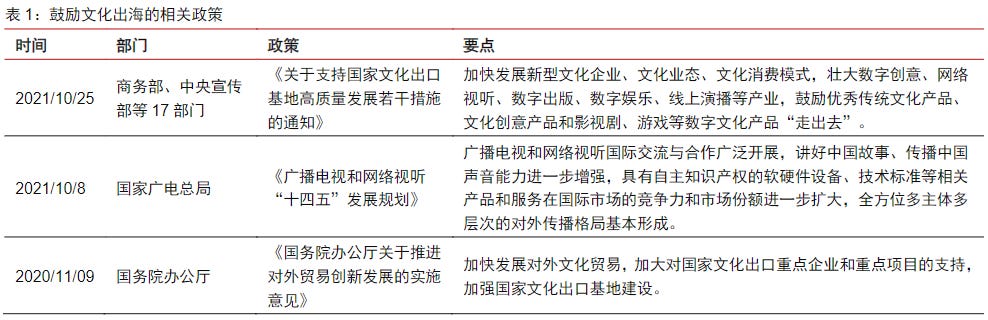

Believe it or not, despite the 8-month long hiatus in approving new games, China isn’t trying to kill its gaming industry ... and in fact encourages its export! The below table shows the latest batch of documents pertaining to that goal, with the latest being an announcement from 17 departments including the Ministry of Commerce and the Central Propaganda Department on “Several Measures to Support the High-quality Development of National Cultural Export Bases.” It’s not specific to gaming but all new media and cultural consumption products in general, and is mainly about the development of bases (e.g. office parks) to accelerate such businesses. That is just a very typical Chinese, infrastructure & supply-side focused solution for how to best capture an emerging market opportunity. I wouldn’t read too much into this — it certainly does not supersede concerns that the government has around gaming domestically, but I do think it is consistent with the ongoing strategy that as long as domestic content and addiction problems are properly addressed, the government was never trying to kill the gaming business wholesale. And most especially not the export side of things.

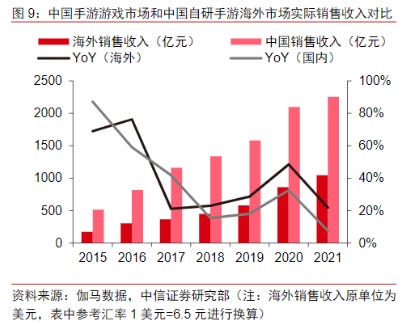

So how has the export business gone? For mobile games, CITIC Securities has kindly tabulated some industry data for us. The figure below shows how overseas sales (in dark red) compare with domestic sales (in pink) for Chinese self-developed mobile game titles. The lines show YoY growth rates, black for overseas and gray for domestic. While it’s not as if overseas sales will overtake domestic sales any time soon (it was just about $3Bn in 2021 and the 2025 estimate for overseas mobile gaming revenues is just $5Bn), the gap is narrowing over time. The goal for any Chinese company to call themselves truly globalized, remember, is to have over 50% of revenues come from overseas. If we apply the same logic to the entire industry, that’s still a ways away, since overseas revenues are less than half of domestic currently, but it is trending favorably in that direction, and with domestic regulatory headwinds, we may see that sooner rather than later.

The below figure shows the number of Chinese mobile games in the Top 2000 from 2018 to 1H 2021. There is a steady increase, although we don’t know how the revenue split looks. But hey, with pioneering titles like Genshin Impact lighting the way, it is probably an even sharper trend upwards.

Finally, it may have slipped your radar, but there is a lot of chatter about P2E or play-to-earn games such as Axie Infinity and other web3 titles. I’m not going to bother going into them here because I don’t think it is a real opportunity in China in the near term. Those who favor its rise argue that F2P (free-to-play AKA freemium) arose in China, and P2E is an even better deal than F2P for the average player, so with the Chinese gaming ecosystem being as massive as it is and with more “innovative dynamics” than the West, it could be the place where P2E breaks out in a big way. I disagree because I can’t see the government supporting this from a regulatory standpoint. Gaming as entertainment and cultural sustenance is OK ... but gaming as employment? And not by the way of e-sports, but as a sort of new blue collar work? Nope, can’t see it happening. And I dare say the newest wave of anti-speculative proposals issued by Chinese financial industry associations re-affirm that fact. Because, it’s about the real economy, remember?

What do you think?

Reply here on the Circle forum

Have any comments or questions? See you on the Discord server!

Copyright (C) *|CURRENT_YEAR|* *|LIST:COMPANY|*. All rights reserved.

*|IFNOT:ARCHIVE_PAGE|**|LIST:DESCRIPTION|**|END:IF|*

*|IFNOT:ARCHIVE_PAGE|**|HTML:LIST_ADDRESS_HTML|**|END:IF|*

Update Preferences | Unsubscribe

*|IF:REWARDS|* *|HTML:REWARDS|* *|END:IF|*