3/16/22 Digest Liu He and the Rebound from the "Policy Bottom", Livestreaming ecommerce after Viya, China SaaS & the Long Way to Go

3/16/22 Digest Liu He and the Rebound from the "Policy Bottom", Livestreaming ecommerce after Viya, China SaaS & the Long Way to Go

View this email in your browser

Insider Digest 3/16/22: Liu He and the Rebound from the "Policy Bottom", Livestreaming ecommerce after Viya, China SaaS & the Long Way to Go

Housekeeping / Announcements / Fun:

Hope the volatility in the markets is treating you OK! After writing and erasing like 4 different posts because they would be outdated as soon as I wrote them, I finally just committed to sending this batch out! But you are missing out if you are not joining in the fun on our Discord server. Thank you for sharing your thoughts and resources so openly and that is the power of this community! I am learning 10x as much as I would on my own and I hope you are too. There really is no substitute for the Discord unfortunately … I wish there was an easy way to bring the content into email for those of you who tell me that the channels overwhelm you, but I hope you can give it a chance! If so, these weeks are definitely the best to get involved!

We still have a little bit of allocation left in the newest TBC Investment Syndicate deal, co-syndicated with Kevin Xu’s Interconnected.blog. If you are an accredited investor and applied to join the syndicate, you should have received an e-mail about the investment. If you don’t see it in your inbox because it went to spam (unfortunately happens often) you can always see the deal here. Please don’t share the link with anyone else!

3/16/22 Liu He’s Remarks and the Rebound from the “Policy Bottom”

3/13/22 Chinese SaaS is a Long Way from Having Its Own Salesforce

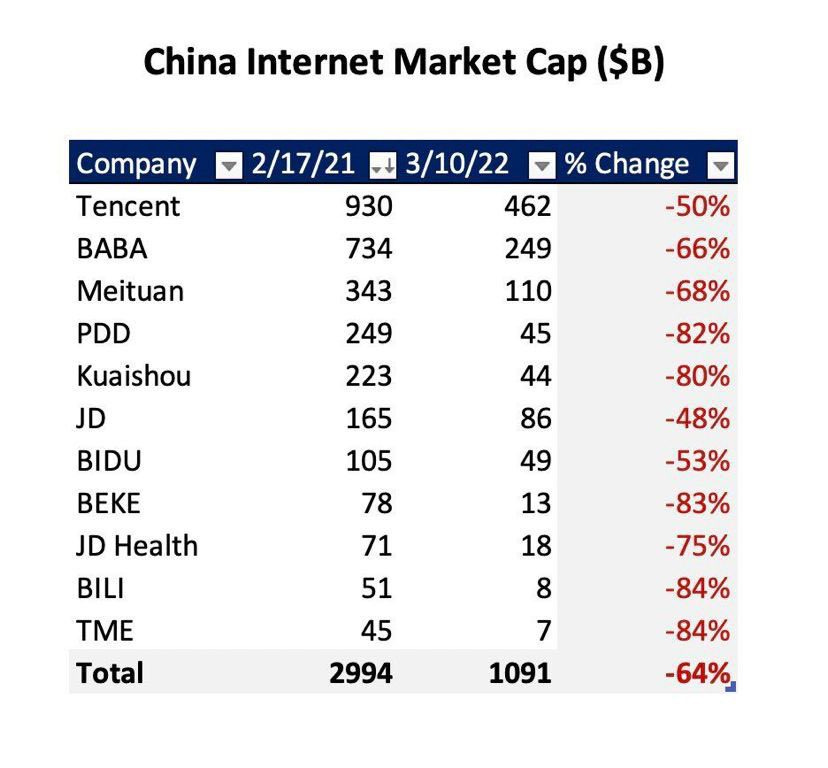

3/16/22 Liu He’s Remarks and the Rebound from the “Policy Bottom”

You can’t possibly have missed the crazy rally today Wednesday 3/16 for Chinese internet stocks in Hong Kong which also extended to US listings. The eye-popping numbers below from Hong Kong are accompanied by Zhihu +79%, Doyu 60%, Pinduoduo 56%, etc. Obviously, this doesn't do that much to counter the drops of the year before, but it is a start ...

Most are attributing the rebound to China’s “econ czar” Liu He’s remarks about the market, although there are many of us on the Discord who think it is also related to people covering their shorts. Here’s some context on Liu He’s remarks, which you can machine translate from the original here:

Many have written on the contents so I won’t really bother but he talked about near term plans for currency and lending, real estate, ADRs, platform regulations, and the Hong Kong Stock Exchange. Of course the first three are actually ultra important, but we care mostly about the last 3 things here at TBCI, so let me just say that he first rehashed some existing news, including:

US & Chinese regulators are working on the issue of ADRs and progress has been made; the Chinese government continues to support companies to go public abroad. This is clearly referring to the ADR delisting risk and the ongoing negotiations between CSRC and SEC.

Platform regulations seek to be standard, transparent, and predictable and reforms should be finished quickly, with red lights and green lights (punished and encouraged behaviors and sectors), increasing stability and international competitiveness. Really nothing new here!

But he also then said a few helpful new things that I hadn’t caught before that seem to specifically address the volatility in the markets:

HKSE stability depends on strengthened communication between mainland and Hong Kong regulators

New policies positive to the market are encouraged, those with contracting effects should be carefully implemented, and departments should be responsive to the market. All policies with large impacts on the capital markets should be coordinated with the financial authorities to ensure stability and consistency. The Committee will increase coordination and conversation and accountability and seek to increase the participation of more long-term investors, blah blah. OK, not everything is new here, but the point about coordination with financial authorities before launching new policies seems promising. Imagine if they had done that before the edtech slaughter!

Note that these remarks were made at the State Council Finance Committee meeting, which actually takes place monthly. However, the meetings are rarely made public, and in any case, there are two different types of meetings, regular ones and themed ones, of which this meeting was a special “themed” one. This theme was “Studying the current economic situation and capital market issues” and it is only the third themed meeting ever publicly disclosed, so I guess you can think of it as a big deal. These meetings are so impactful that they are sometimes pointed to being the “policy bottom,” (haha, so not JPM bottom or Alex Yao bottom) since they often result in a rebound.

3/12/22 Life in Livestreaming Ecommerce After Viya

Austin Has Not Replaced Viya

As you should know by now, Austin was the undisputed #2 in Chinese ecommerce livestreaming, until Viya vacating the top spot due to tax fraud unexpectedly propped him up to #1. The day of Viya’s ban, he doubled his viewership to 38mm, and then to 49mm, but most were hecklers in it for the spectacle, and within a week, he had fallen to his 16mm average viewership. His fan count remains at 62mm, far short of Viya’s 80mm.

While he has tried to capture some of Viya’s fans by changing his inventory to absorb some of her brands, this hasn’t been as successful as some have anticipated. For those who’ve watched them in action, they really are quite different personality wise, and they’ve always had different product mixes. Changing too much would probably alienate his existing fanbase.

But He Did Well on 3/8

So let’s talk about 3/8 International Women’s Day, which has become a minor shopping holiday in China. Since it is so overtly female focused, however, it has become a major contest for certain brands — cosmetics in particular, of course. The timing is also in between Single’s Day and the other major shopping festival of the year, 6/18, which is why despite it being “minor,” marketers and brands watch it with great anticipation every year.

In fact, one of the biggest tip-offs to Perfect Diary / Yatsen’s impending decline was their less than stellar performance during the 2020 Women’s Day holiday. And that was not long after them taking the crown for Single’s Day, so many industry watchers concluded that they had overextended themselves in anticipation of the IPO and used up all their bullets ... and that furthermore, their customer retention was problematic ... all of which has turned out to be true. (See their latest disastrous filings here, although the steep decline started not long after the IPO.)

3/13/22 Chinese SaaS is a Long Way from Having Its Own Salesforce

This was a fairly popular article on Chinese SaaS when it came out about a year and a half ago. I saw it cited again and wanted to put it here as food for thought because I think while the industry has made some progress, the below still largely applies.

It’s probably best paired with another article I cited previously - Chinese vs. US Enterprise Software Opportunity.

On the Demand (Customer) Side ... (20% of the problem)

Lack of Standardization

One reason for this discrepancy is that the Chinese market is much more diverse than the US. Industries in China are also more complex and difficult to standardize.

Lack of Support

In China, it is also common that companies purchased a system but are not able to use it, since they don’t have a training system in place to support it.

Focus on Price

Immature customers can mean they use only the simplest use cases, reducing SaaS providers to the lowest common denominator of the most basic features competing on price.

On the Supply (SaaS Provider) Side ... (80% of the problem)

Lagging Development Abilities

SaaS “began” in China in 2015. Because so many enterprise software companies in China back then grew up delivering customized solutions instead of standardized products, this is how developers in the industry are used to working as well.

Killer Feature Thinking Doesn’t Work

While 2C software products can survive with one killer feature and a bunch of mediocre ones, 2B cannot. Everything needs to function to an acceptable level or else the customer will churn. China SaaS hasn’t developed this level of attention to detail yet.

Differentiation

Homogenization is probably the biggest problem for Chinese SaaS companies. Everyone goes after the same features and stops there. Deep, differentiated products/services usually result in shorter decision-making times as well as lower churn rates. It goes back to the point that the development talent is thin and the finished products are still subpar. For those customers who do have more sophisticated demands, the SaaS service providers aren’t able to provide the necessary customization (at the stated cost).

Making Reusable Modules

Again, thin development talent means that the level of structural planning that is needed rarely happens and modules are not often built in an efficient or sustainable way for future growth.

Have any comments or questions? See you on the Discord server!

Copyright (C) *|CURRENT_YEAR|* *|LIST:COMPANY|*. All rights reserved.

*|IFNOT:ARCHIVE_PAGE|**|LIST:DESCRIPTION|**|END:IF|*

*|IFNOT:ARCHIVE_PAGE|**|HTML:LIST_ADDRESS_HTML|**|END:IF|*

Update Preferences | Unsubscribe

*|IF:REWARDS|* *|HTML:REWARDS|* *|END:IF|*