1/20/22 Tech Buzz China Insider Digest

View this email in your browser

Insider Digest 1/20/22: 2022 Tech Regulation Outlook, China Tech 2021 Investment Roundup, WeChat Developer Day, Bearish View on VIEs and More

Housekeeping / Announcements:

Oh my goodness, sorry for the very long delay. If you’re active on our Discord you know that I was out with COVID until this week (3 week illness, no joke, and a lingering cough, so stay safe!) and finally started feeling better enough on Monday to get back into the swing of things. Let’s see if we can make the weekly Discord gathering happen next week!

We’re still trying out different days to send out this newsletter, but it seems that some of you have a strong preference for the weekend. Let us know if you feel differently!

Here are our articles for the week! Due to the holidays and my illness, there is a bit more than usual. Again, a lot of these things are unfolding in real time, such as the Reuters rumor (later debunked) on internet platforms over 100mm users or $1.5Bn revenue in having to go through extra approvals for investments, so join us on Discord to discuss! Let’s get started —

1/18/22 The Final, Definitive Word on 2021 China Tech Investments

1/19/22 Comments on Chinese Regulations in 2022 from GR Veteran and 11-Year Ex-MOFCOM Employee

1/12/22 - US Lawmakers target Chinese Biotech

Yesterday, Republicans on the House Energy and Commerce (E&C) Committee issued a press release highlighting bills their members are leading to "combat and stop influence from the Chinese Communist Party in American medical research." E&C Republicans introduced seven bills that "increase transparency, improve oversight, and protect biomedical intellectual property" through the Department of Health and Human Services (HHS) and the National Institutes of Health (NIH).

The GOP is likely to take back the House and Senate in the November midterm elections, but it should not be assumed that there won't be any support from Democrats for these bills before that time. American biotech companies will undoubtedly strongly support most of these measures.

1/12/22: The Bearish View on VIEs

Ahhh, VIEs. You thought the last word had been uttered on these squishy, slippery things, but alas, that isn’t the case. I’m not one of those people who have been proclaiming the death of the VIE — but I’m also not as optimistic as the lawyers I’ve spoken to who make their living on VIEs and cling onto the status quo. “The government will never do anything about it,” they say, “deaths of the VIE come around every few years and it’s never been overturned.” It’s thus perfectly safe, they reason. But is it really? Let’s look at what the new rules actually say:

On December 24, 2021, CSRC and State Council came out with two documents:

CSRC: Administrative Measures for the Recordation of Overseas Issuance of Securities and Listing by Domestic Enterprises (in Chinese), a draft document out for comment that formalizes the process by which Chinese companies must seek parallel permission from the CSRC before listing overseas. Specifically, they are to hand in materials to the CSRC within 3 working days of publicly applying for an overseas IPO, including applicable opinions, filings or approvals by industry authorities. This doesn’t just include initial public offerings but other securities offerings, including issuances for purchasing other assets. Assuming materials are complete, CSRC is to give a response within 20 working days and publish the results thereof on its website.

Click through for more …. mainly why I don’t think you should rely too much on the CSRC’s words

1/18/22 A Lackluster WeChat Developer Day

Anyway, onto WeChat’s annual developer day 2022! It was a very quiet affair this year, in large part due to Allen Zhang’s absence. This was the first time he didn’t show up in any form at all — in 2020 he at least bothered to send a brief recorded video. In some of the other years he’s given hours of speeches, not just on his vision for WeChat but sometimes on his philosophy about product management and social networking in general. Real nuggets of wisdom that are mulled over and treasured by the tech community. I don’t know what exactly to read into this — Allen kind of does what he wants. Nonetheless, it significantly dampened the interest the audience had in what WeChat had to share, which I’m sorry to report, contained very little of note:

On Channels / Live:

Channels is actively trying to “operate”/ produce (versus relying on organic distribution, which is more of Allen’s “let the product speak for itself” style) content. The Westlife WeChat concert that got 28mm viewers is an example of this. However, while this was record breaking for Channels, the stats are pretty middling when you compare it with what other platforms have been able to achieve. So ... good job WeChat, but not sure how much applause that really deserves.

WeChat immediately tried two other concerts after this and announced that they plan to onboard more musicians in 2022, but I don’t know how this really differentiates the platform in any way, as Douyin and Kuaishou et al. have been doing this for years?

Click through for more …. WeChat Pay, WeCom, Mini Programs

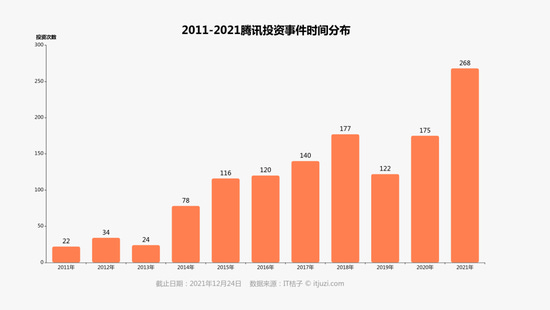

1/18/22 Brief Note on Tencent's Accelerating Investments

I've alluded to this specific article before, but in light of more commentary recently such as this SCMP piece about Tencent downsizing its tech empire, even the piece itself acknowledges that the company has, in fact been increasing its investment pace, and while its divestitures were larger than usual last year, it does regularly divest -- to the tune of ~$3Bn every year. JD and Sea were not its only divestitures last year -- there was also Zhihu, and a few other domestically listed Chinese companies.

So what did Tencent do exactly in 2021? This ultra detailed analysis from ITJuzi tells the complete story.

1/18/22 The Final, Definitive Word on 2021 China Tech Investments

I've posted so much on China VC investment already, so I promise this is the last time! But there are a few nuggets in here that's sufficiently different from what I've posted before that I feel compelled to share. Some of you have seen me post an abridged version of these notes on Twitter, but this post has much more detail. Here goes:

Note: this data is pulled from the 100-page ITJuzi 2021 China New Economy Unicorn Enterprises Research Report available here.

China has 295 unicorns or 37% of the world's unicorns, second behind the US at 316 or 39%.

Note that this is ITJuzi's total, which is less than the over 900 as combined by organizations like CBInsights, so I wouldn't try to match up data exactly. But by this measure, just China and the US account for 76% of the world's unicorns.

In addition, ITJuzi counts spinoffs such as Ant as unicorns. This is a common practice, but there are a lot more unicorn spinoffs in China than in the US,

Chinese unicorns are most numerous in enterprise software (46 or 16%), healthcare (39 or 13% ), automotive (35 or 12%), ecommerce (27 or 9%) and advanced manufacturing (22 or 7%). Just the top 5 categories is 57% of the total, showing heavy concentration.

1/19/22 Comments on Chinese Regulations in 2022 from GR Veteran and 11-Year Ex-MOFCOM Employee

1. On internet regulations in 2022:

The main theme of internet regulations is common prosperity, with two supporting lines: antitrust and network / data security.

On common prosperity, guidelines affecting the next 10-20 years are predicted to come out after Lianghui (late July to early August) or after the break in September.

Common prosperity means there will be 3 divisions: some industries will be expected to provide high quality growth & encouraged (advanced manufacturing, new energy vehicles, etc.), some will be rectified & given limits (e.g. internet) and some will become more of a public service (education, healthcare, senior care, real estate, etc.)

Local governments will give out policies after the national ones have been established, and may have overlap with existing regulations, but it is expected that the government will try to avoid the extreme measures applied to the after-school tutoring sector

Tax loopholes and subsidies will be fixed, and may include taking away the tax breaks currently afforded to internet companies

On antitrust: there is expected to be less movement as most of the core oversight organizations have been established and tools published, landmark cases prosecuted. New cases will happen but they should be less unexpected

The emphasis will be on anticompetitive behaviors instead and enforcement will spread from the top companies to more entities, but landmark cases have yet to emerge. This is much more nuanced than antitrust, and we will see if the Chinese regulators really have a coherent policy framework. I don't expect the markets to like this ...

There will be a push towards data opening up / sharing, and the regulators are especially interested in seeing the big players do more things for the ecosystem

Top platforms will be restricted in their investments. See below.

After Ant is separated into fintech, consumer tech, and internet microloan entities, can expect the same for WeChat Pay

Network / data / personal information security may have some cases this year, as CAC has strong political motivations to proactively investigate; overall the costs for compliance might be higher than antitrust. Results of the Didi case will be a landmark ruling in this category. It is quite incredible to me that there is still no resolution.

Have any comments or questions? See you on the Discord server!

Copyright (C) *|CURRENT_YEAR|* *|LIST:COMPANY|*. All rights reserved.

*|IFNOT:ARCHIVE_PAGE|**|LIST:DESCRIPTION|**|END:IF|*

*|IFNOT:ARCHIVE_PAGE|**|HTML:LIST_ADDRESS_HTML|**|END:IF|*

Update Preferences | Unsubscribe

*|IF:REWARDS|* *|HTML:REWARDS|* *|END:IF|*